import pandas as pd # 导入数据分析库 pandas

# Import the pandas library for data analysis

import numpy as np # 导入数值计算库 numpy

# Import the numpy library for numerical computation

import matplotlib.pyplot as plt # 导入绘图库 matplotlib

# Import the matplotlib library for plotting

import seaborn as sns # 导入统计可视化库 seaborn

# Import the seaborn library for statistical visualization

import platform # 导入平台检测库,用于自动适配数据路径

# Import the platform library for OS detection and auto-adapting data paths

# 设置中文字体,确保图表中中文正常显示

# Set Chinese fonts to ensure proper display of Chinese characters in charts

plt.rcParams['font.sans-serif'] = ['SimHei', 'Microsoft YaHei'] # 设置中文字体优先级列表

# Set the priority list of Chinese fonts

# 解决负号显示问题

# Fix the minus sign display issue

plt.rcParams['axes.unicode_minus'] = False # 修复负号显示为方块的问题

# Fix the issue where minus signs are displayed as squares

# 根据操作系统自动设置本地数据路径

# Automatically set local data paths based on the operating system

if platform.system() == 'Windows': # 判断当前操作系统类型

# Check the current operating system type

data_path = 'C:/qiufei/data/stock' # Windows 数据路径

# Data path for Windows

else: # Linux 系统下使用服务器数据路径

# Use server data path on Linux

data_path = '/home/ubuntu/r2_data_mount/qiufei/data/stock' # Linux 数据路径

# Data path for Linux

# 读取上市公司基本信息

# Load basic information of listed companies

stock_basic_dataframe = pd.read_hdf(f'{data_path}/stock_basic_data.h5') # 加载上市公司基本信息数据

# Load the basic information dataset of listed companies

# 读取前复权日度行情数据

# Load pre-adjusted daily price data

stock_price_dataframe = pd.read_hdf(f'{data_path}/stock_price_pre_adjusted.h5') # 加载前复权日度股价行情

# Load pre-adjusted daily stock price data

# 重置索引,使 order_book_id 和 date 从索引变为普通列

# Reset the index so that order_book_id and date become regular columns

stock_price_dataframe = stock_price_dataframe.reset_index() # 将多级索引转为普通列便于筛选操作

# Convert multi-level index to regular columns for easier filtering1 统计学导论 (Introduction to Statistics)

统计学是一门关于数据的科学,它系统地研究数据的收集、整理、分析和解释,从而从数据中提取有价值的信息和知识。在当今这个大数据时代,统计学已经渗透到商业、经济、医学、工程、社会科学等几乎所有领域,成为决策者和研究者不可或缺的工具。对于商学院的学生而言,掌握统计学思维和方法,不仅意味着能够分析数据,更意味着能够在不确定的商业环境中做出理性的、基于证据的决策。

Statistics is the science of data. It systematically studies the collection, organization, analysis, and interpretation of data to extract valuable information and knowledge. In today’s era of big data, statistics has permeated virtually every field—business, economics, medicine, engineering, and the social sciences—making it an indispensable tool for decision-makers and researchers. For business school students, mastering statistical thinking and methods means not only being able to analyze data, but also being able to make rational, evidence-based decisions in an uncertain business environment.

1.0.1 统计学在经济金融领域的典型应用 (Typical Applications of Statistics in Economics and Finance)

统计学是现代金融和经济学研究的基石。对于商学院的学生来说,最重要的不是统计学的历史沿革,而是它今天如何被实际地用于解决真实的商业和金融问题。以下几个典型应用场景,涵盖了本书后续章节将要系统介绍的核心方法,旨在激发学生的学习动力。

Statistics is the cornerstone of modern finance and economics research. For business school students, the most important thing is not the historical evolution of statistics, but rather how it is actually used today to solve real business and financial problems. The following typical application scenarios cover the core methods that will be systematically introduced in subsequent chapters of this book, aiming to inspire students’ motivation to learn.

1.0.1.1 应用一:投资组合风险管理 (Application 1: Portfolio Risk Management)

投资组合管理是金融学的核心议题之一。Harry Markowitz 于 1952 年提出的均值-方差 (Mean-Variance) 框架,其核心思想是:投资者应该在给定的风险水平下最大化预期收益,或在给定的收益水平下最小化风险。这个理论的全部技术工具——均值、方差、协方差、相关系数——正是本书 章节 2 和 章节 8 的核心内容。

Portfolio management is one of the core topics in finance. The Mean-Variance framework proposed by Harry Markowitz in 1952 is based on the idea that investors should maximize expected return for a given level of risk, or minimize risk for a given level of return. All the technical tools of this theory—mean, variance, covariance, and correlation coefficient—are precisely the core content of 章节 2 and 章节 8 in this book.

一位量化基金经理的日常工作流程大致如下:

The daily workflow of a quantitative fund manager roughly involves the following:

计算收益率的描述统计量(第二章): 均值代表预期收益,标准差代表风险

构建相关系数矩阵(第八章): 理解资产之间的联动关系,这是分散化投资的关键

进行回归分析(第八章、第十章): 估计资产的 Beta 系数,量化系统性风险敞口

假设检验(第五章、第七章): 评估投资策略的 Alpha 是否统计显著,即超额收益是能力还是运气

Computing descriptive statistics of returns (Chapter 2): The mean represents expected return; the standard deviation represents risk

Constructing a correlation matrix (Chapter 8): Understanding the co-movement between assets, which is key to diversification

Performing regression analysis (Chapters 8 and 10): Estimating the Beta coefficient of assets to quantify systematic risk exposure

Hypothesis testing (Chapters 5 and 7): Evaluating whether the Alpha of an investment strategy is statistically significant—i.e., whether excess returns are due to skill or luck

我们来用中国A股市场的真实数据,快速预览一下统计学在投资分析中的应用:

Let us use real data from China’s A-share market to quickly preview the application of statistics in investment analysis:

本地股票基本信息和行情数据加载完毕。下面选取5家长三角代表性上市公司2023年数据,并计算日对数收益率。

Local stock basic information and price data have been loaded. Next, we select 5 representative listed companies from the Yangtze River Delta region for 2023 data and calculate daily log returns.

# 选取5家长三角代表性上市公司

# Select 5 representative listed companies from the Yangtze River Delta

# 海康威视(杭州)、宁波银行(宁波)、恒瑞医药(连云港)、科大讯飞(合肥)、上汽集团(上海)

# Hikvision (Hangzhou), Bank of Ningbo (Ningbo), Hengrui Medicine (Lianyungang), iFlytek (Hefei), SAIC Motor (Shanghai)

selected_stock_id_list = [ # 初始化长三角代表性公司股票代码列表

# Initialize the stock code list of representative YRD companies

'002415.XSHE', # 海康威视 - 安防科技龙头

# Hikvision - Leading security technology company

'002142.XSHE', # 宁波银行 - 城商行标杆

# Bank of Ningbo - Benchmark city commercial bank

'600276.XSHG', # 恒瑞医药 - 创新药龙头

# Hengrui Medicine - Leading innovative pharmaceutical company

'002230.XSHE', # 科大讯飞 - AI语音龙头

# iFlytek - Leading AI voice technology company

'600104.XSHG', # 上汽集团 - 汽车制造龙头

# SAIC Motor - Leading automobile manufacturer

] # 完成长三角地区5家代表性上市公司的股票代码列表定义

# Completed the definition of the stock code list for 5 representative YRD companies

# 筛选这5家公司2023年全年的行情数据,并复制以避免 SettingWithCopyWarning

# Filter the 2023 full-year price data for these 5 companies, copying to avoid SettingWithCopyWarning

filtered_price_2023 = stock_price_dataframe[ # 基于布尔索引筛选目标股票和日期范围

# Filter target stocks and date range using boolean indexing

(stock_price_dataframe['order_book_id'].isin(selected_stock_id_list)) & # 股票代码在选定列表中

# Stock code is in the selected list

(stock_price_dataframe['date'] >= '2023-01-01') & # 日期不早于2023年1月1日

# Date is no earlier than January 1, 2023

(stock_price_dataframe['date'] <= '2023-12-31') # 日期不晚于2023年12月31日

# Date is no later than December 31, 2023

].copy() # 复制数据避免 SettingWithCopyWarning

# Copy data to avoid SettingWithCopyWarning

# 将数据从长格式 (long format) 转换为宽格式 (wide format)

# Convert data from long format to wide format

# 每一列代表一只股票的收盘价,每一行代表一个交易日

# Each column represents a stock's closing price; each row represents a trading day

pivoted_close_price = filtered_price_2023.pivot( # 将长格式数据透视为宽格式(每列一只股票)

# Pivot long-format data into wide format (one stock per column)

index='date', # 以日期为行索引

# Use date as the row index

columns='order_book_id', # 以股票代码为列名

# Use stock code as column names

values='close' # 提取收盘价

# Extract closing prices

) # 完成数据透视,得到以日期为行、股票为列的收盘价宽格式矩阵

# Completed the pivot, obtaining a wide-format matrix of closing prices with dates as rows and stocks as columns

# 计算日对数收益率: ln(P_t / P_{t-1})

# Calculate daily log returns: ln(P_t / P_{t-1})

# 对数收益率具有时间可加性,是金融学中的标准做法

# Log returns have the property of time additivity, which is standard practice in finance

daily_log_returns = np.log(pivoted_close_price / pivoted_close_price.shift(1)).dropna() # 计算日对数收益率并删除首行缺失值

# Calculate daily log returns and drop the first row with missing values上述代码完成了数据加载、筛选和对数收益率计算。下面将列名替换为公司简称,并绘制相关性热力图。

The above code completes data loading, filtering, and log return calculation. Next, we replace column names with company abbreviations and plot the correlation heatmap.

# 将列名从股票代码替换为更易读的公司简称

# Replace column names from stock codes to more readable company abbreviations

stock_name_mapping = { # 构建股票代码到公司简称的映射字典

# Build a mapping dictionary from stock codes to company abbreviations

'002415.XSHE': '海康威视', # 杭州,安防科技龙头

# Hangzhou, leading security technology company

'002142.XSHE': '宁波银行', # 宁波,城商行标杆

# Ningbo, benchmark city commercial bank

'600276.XSHG': '恒瑞医药', # 连云港,创新药龙头

# Lianyungang, leading innovative pharmaceutical company

'002230.XSHE': '科大讯飞', # 合肥,AI语音龙头

# Hefei, leading AI voice technology company

'600104.XSHG': '上汽集团', # 上海,汽车制造龙头

# Shanghai, leading automobile manufacturer

} # 完成股票代码到公司简称的映射字典定义

# Completed the definition of the mapping dictionary from stock codes to company abbreviations

daily_log_returns.columns = [stock_name_mapping[col] for col in daily_log_returns.columns] # 将列名从股票代码替换为公司简称

# Replace column names from stock codes to company abbreviations

# 计算相关系数矩阵: 衡量任意两只股票收益率的线性关联程度

# Calculate the correlation matrix: measure the degree of linear association between any two stocks' returns

correlation_matrix = daily_log_returns.corr() # 计算Pearson相关系数矩阵

# Compute the Pearson correlation coefficient matrix

# 绘制热力图: 直观展示资产间的相关性结构

# Plot a heatmap: visually display the correlation structure among assets

fig, axis = plt.subplots(figsize=(8, 6)) # 创建8x6英寸的画布

# Create an 8x6-inch canvas

sns.heatmap( # 绘制相关系数热力图

# Plot the correlation coefficient heatmap

correlation_matrix, # 传入相关系数矩阵

# Pass in the correlation matrix

annot=True, # 在每个格子中显示数值

# Display values in each cell

fmt='.2f', # 保留两位小数

# Keep two decimal places

cmap='RdBu_r', # 使用红蓝配色方案(红色=正相关,蓝色=负相关)

# Use the red-blue color scheme (red = positive correlation, blue = negative correlation)

center=0, # 将颜色中心设为0

# Set the color center to 0

vmin=-1, vmax=1, # 相关系数的取值范围为[-1, 1]

# The range of correlation coefficients is [-1, 1]

square=True, # 让每个格子为正方形

# Make each cell square

ax=axis # 指定绑图坐标轴

# Specify the plotting axis

) # 完成相关性热力图的绑制参数配置

# Completed the configuration of heatmap plotting parameters

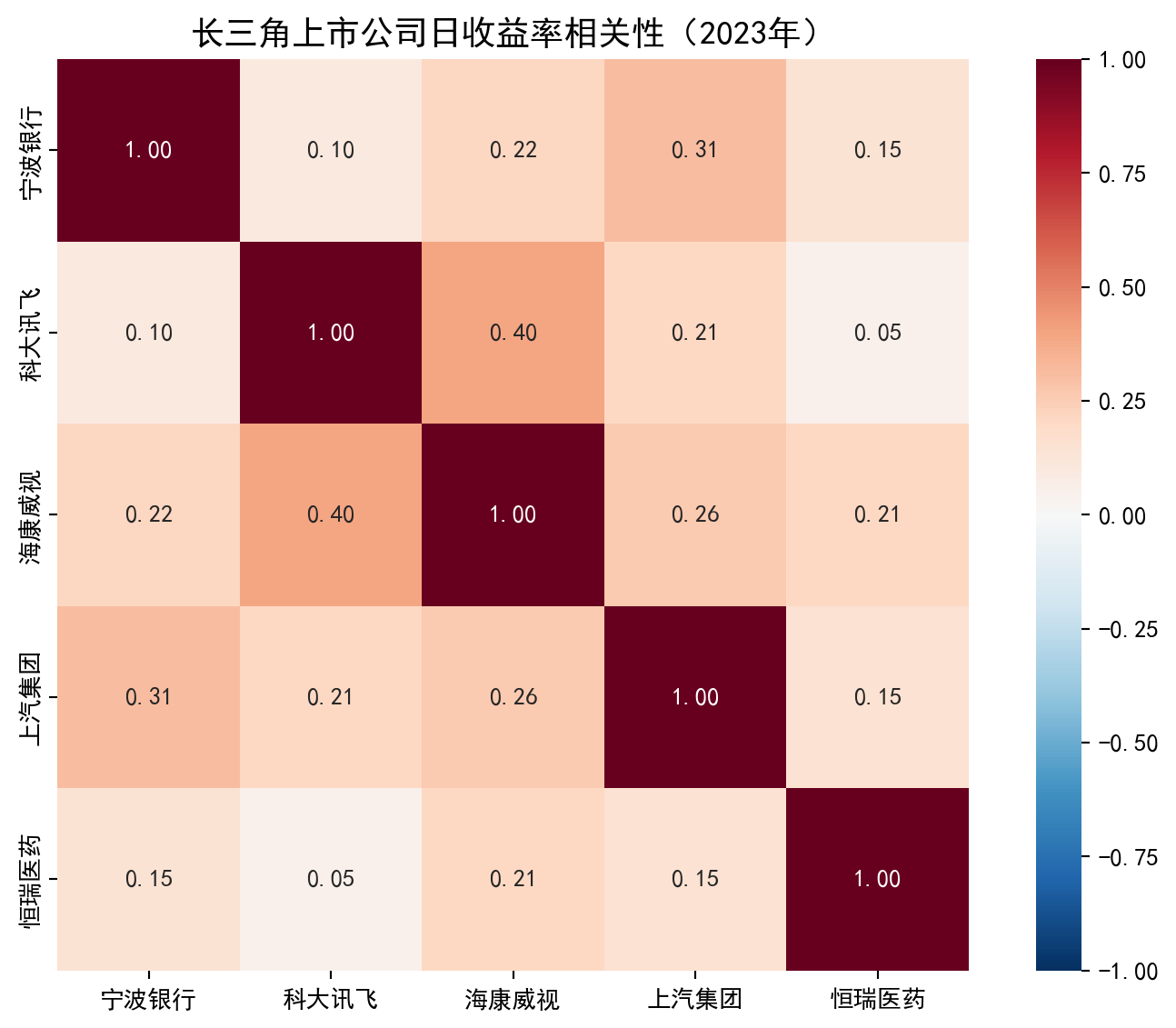

axis.set_title('长三角上市公司日收益率相关性(2023年)', fontsize=14) # 设置热力图标题

# Set the heatmap title

plt.tight_layout() # 自动调整布局,防止标签被截断

# Automatically adjust layout to prevent label clipping

plt.show() # 渲染并展示图形

# Render and display the figure

上图展示的相关系数矩阵揭示了一个重要信息:不同行业的股票之间相关性较低,这意味着将它们组合在一起可以有效分散风险——这正是 Markowitz 投资组合理论的核心洞察。我们将在 章节 8 中系统学习相关系数的计算与检验方法。

The correlation matrix shown above reveals an important insight: stocks from different industries have relatively low correlations, meaning that combining them can effectively diversify risk—this is precisely the core insight of Markowitz’s portfolio theory. We will systematically study the calculation and testing of correlation coefficients in 章节 8.

1.0.1.2 应用二:上市公司财务质量的统计评估 (Application 2: Statistical Assessment of Listed Company Financial Quality)

在基本面分析中,投资者需要从数以千计的上市公司中筛选出财务质量优良的标的。这一过程大量使用描述统计( 章节 2 )和推断统计( 章节 5 )的方法:

In fundamental analysis, investors need to screen thousands of listed companies to identify those with excellent financial quality. This process extensively uses methods of descriptive statistics ( 章节 2 ) and inferential statistics ( 章节 5 ):

描述统计:计算全市场公司的营收增长率、净资产收益率 (ROE)、资产负债率等指标的均值、中位数、标准差,从而建立”行业基准” (benchmark)

概率分布:财务指标的分布形态(是否正态、是否存在偏态和厚尾)直接影响我们选择哪种统计方法进行分析( 章节 4 )

假设检验:例如,检验长三角地区上市公司的 ROE 是否显著高于全国平均水平( 章节 7 )

回归分析:探究影响公司盈利能力的关键因素,如研发投入、资产规模、财务杠杆等( 章节 10 )

Descriptive statistics: Calculate the mean, median, and standard deviation of metrics such as revenue growth rate, return on equity (ROE), and debt-to-asset ratio for all listed companies, thereby establishing “industry benchmarks”

Probability distributions: The distributional shape of financial indicators (whether normal, skewed, or heavy-tailed) directly affects which statistical methods we choose for analysis ( 章节 4 )

Hypothesis testing: For example, testing whether the ROE of companies in the Yangtze River Delta region is significantly higher than the national average ( 章节 7 )

Regression analysis: Investigating key factors affecting corporate profitability, such as R&D investment, asset size, and financial leverage ( 章节 10 )

1.0.1.3 应用三:量化因子投资 (Application 3: Quantitative Factor Investing)

在中国资本市场,量化投资已经成为一种主流的投资策略。其核心思想是:构建一系列能够预测股票未来收益的”因子”(factor),如市盈率 (PE)、市净率 (PB)、市值 (Market Cap)、动量 (Momentum) 等,然后通过多元回归模型( 章节 10 )和机器学习方法( 章节 12 、 章节 13 )来构建选股模型。

In the Chinese capital market, quantitative investing has become a mainstream investment strategy. Its core idea is to construct a set of “factors” that can predict future stock returns—such as price-to-earnings ratio (PE), price-to-book ratio (PB), market capitalization, and momentum—and then use multiple regression models ( 章节 10 ) and machine learning methods ( 章节 12, 章节 13 ) to build stock selection models.

一个完整的因子投资研究流程涉及本书几乎所有的统计方法:

A complete factor investing research process involves almost all the statistical methods in this book:

探索性数据分析( 章节 2 ):理解因子的分布特征和截面差异

相关性分析( 章节 8 ):检验因子之间的多重共线性

回归分析( 章节 10 ):估计因子对收益率的边际贡献

方差分析( 章节 9 ):比较不同因子组合的策略表现是否有显著差异

非线性模型( 章节 11 ):当因子与收益率之间的关系不是简单线性时,需要使用逻辑回归等非线性方法

树模型和集成学习( 章节 12 ):处理高维因子的非线性交互效应

聚类分析( 章节 13 ):将股票根据因子特征进行无监督分类,发现市场的内在结构

Exploratory data analysis ( 章节 2 ): Understanding the distributional characteristics and cross-sectional differences of factors

Correlation analysis ( 章节 8 ): Testing multicollinearity among factors

Regression analysis ( 章节 10 ): Estimating the marginal contribution of each factor to returns

Analysis of variance ( 章节 9 ): Comparing whether the performance of different factor combinations differs significantly

Nonlinear models ( 章节 11 ): When the relationship between factors and returns is not simply linear, nonlinear methods such as logistic regression are needed

Tree models and ensemble learning ( 章节 12 ): Handling nonlinear interaction effects of high-dimensional factors

Cluster analysis ( 章节 13 ): Unsupervised classification of stocks based on factor characteristics to discover the intrinsic structure of the market

1.0.1.4 应用四:宏观经济与货币政策分析 (Application 4: Macroeconomic and Monetary Policy Analysis)

宏观经济数据(GDP增长率、CPI、PMI、M2增速等)是影响资本市场走势的关键因素。经济学家和分析师大量使用时间序列分析方法来研究宏观经济变量之间的动态关系。虽然本书侧重于截面数据和面板数据的方法,但其中许多核心概念——如回归分析、自变量选择、模型诊断——在时间序列分析中同样适用。

Macroeconomic data (GDP growth rate, CPI, PMI, M2 growth rate, etc.) are key factors influencing the trends of capital markets. Economists and analysts extensively use time series analysis methods to study the dynamic relationships among macroeconomic variables. Although this book focuses on cross-sectional and panel data methods, many of its core concepts—such as regression analysis, variable selection, and model diagnostics—are equally applicable in time series analysis.

例如,中国央行在制定货币政策时,会使用统计模型来评估利率调整对经济增长和物价稳定的影响。投资者也会利用回归模型来分析宏观经济指标对股票市场的传导机制。

For example, when formulating monetary policy, the People’s Bank of China uses statistical models to assess the impact of interest rate adjustments on economic growth and price stability. Investors also use regression models to analyze the transmission mechanism of macroeconomic indicators to the stock market.

小结:统计学是金融决策的语言

Summary: Statistics is the Language of Financial Decision-Making

从以上四个应用场景可以看出,统计学不是一门抽象的数学理论,而是金融从业者每天都在使用的实用工具。无论是投资组合管理、公司财务分析、量化策略开发,还是宏观经济研究,统计方法无处不在。本书的目标,就是帮助商学院的学生系统地掌握这些方法,并能够将其应用于中国资本市场的真实数据分析之中。

From the above four application scenarios, we can see that statistics is not an abstract mathematical theory, but a practical tool used daily by finance professionals. Whether it is portfolio management, corporate financial analysis, quantitative strategy development, or macroeconomic research, statistical methods are ubiquitous. The goal of this book is to help business school students systematically master these methods and apply them to real data analysis in China’s capital markets.

1.1 统计学在商业决策中的核心作用 (The Core Role of Statistics in Business Decision-Making)

1.1.1 案例研究:A/B测试在券商量化策略中的应用 (Case Study: A/B Testing in Securities Firm Quantitative Strategies)

让我们通过一个中国证券行业的真实案例来理解统计学的核心价值。

Let us understand the core value of statistics through a real case from China’s securities industry.

1.1.1.1 背景:券商量化选股策略优化 (Background: Optimization of Securities Firm Quantitative Stock Selection Strategy)

某头部券商的量化投研团队管理着超过200亿元的资产。为了提升组合的超额收益(Alpha),团队开发了一种新的多因子选股模型,声称可以提高策略的月度胜率(Win Rate)。

A leading securities firm’s quantitative investment research team manages over 20 billion yuan in assets. To improve the portfolio’s excess return (Alpha), the team developed a new multi-factor stock selection model, claiming it could improve the strategy’s monthly win rate.

1.1.1.2 实验设计 (Experimental Design)

为了验证这个新模型是否真的有效,他们设计了如下随机对照实验:

To verify whether this new model is truly effective, they designed the following randomized controlled experiment:

实验参数:

Experimental Parameters:

实验周期:12个月回测

样本规模:20,000次模拟交易信号

随机分配:10,000次信号使用新模型,10,000次使用旧模型

Experimental period: 12-month backtest

Sample size: 20,000 simulated trading signals

Random assignment: 10,000 signals use the new model, 10,000 use the old model

分组方案:

Group Assignment:

处理组(Treatment Group):使用新多因子选股模型

对照组(Control Group):使用原选股模型

Treatment Group: Uses the new multi-factor stock selection model

Control Group: Uses the original stock selection model

1.1.1.3 实验结果 (Experimental Results)

如 表 1.1 所示,实验结果显示处理组的月度胜率(25%)比对照组(22%)高出3个百分点。

As shown in 表 1.1, the experimental results show that the treatment group’s monthly win rate (25%) is 3 percentage points higher than the control group (22%).

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import pandas as pd # 导入数据分析库 pandas

# Import the pandas data analysis library

# ========== 构建A/B测试结果数据 ==========

# ========== Build A/B test result data ==========

# 演示用模拟数据 (Mock data for demonstration)

# Mock data for demonstration

# 场景:某头部券商量化团队对比新旧选股模型的效果

# Scenario: A leading securities firm's quant team compares new vs. old stock selection models

ab_test_data_dict = { # 构建A/B测试结果的数据字典

# Build the data dictionary for A/B test results

'组别': ['处理组(新因子模型)', '对照组(旧因子模型)'], # 实验分组名称

# Experimental group names

'模拟交易信号数': [10000, 10000], # 每组产生的模拟交易信号数量

# Number of simulated trading signals per group

'月度胜出信号数': [2500, 2200], # 信号产生正收益的次数

# Number of signals that generated positive returns

'月度胜率': ['25%', '22%'] # 胜出信号数 / 总信号数

# Win rate = winning signals / total signals

} # 完成A/B测试结果数据字典的构建

# Completed the construction of the A/B test result data dictionary

# ========== 创建并展示结果表格 ==========

# ========== Create and display the results table ==========

ab_test_results_dataframe = pd.DataFrame(ab_test_data_dict) # 将字典转为 DataFrame

# Convert the dictionary to a DataFrame

ab_test_results_dataframe # 输出表格

# Output the table| 组别 | 模拟交易信号数 | 月度胜出信号数 | 月度胜率 | |

|---|---|---|---|---|

| 0 | 处理组(新因子模型) | 10000 | 2500 | 25% |

| 1 | 对照组(旧因子模型) | 10000 | 2200 | 22% |

1.1.1.4 统计学的核心问题 (The Core Question of Statistics)

这3个百分点的差异是真实的、由新因子模型带来的效果,还是仅仅由于随机波动造成的偶然结果?

Is this 3-percentage-point difference a real effect brought by the new factor model, or merely a chance result caused by random fluctuation?

这就是统计学的核心问题。现实世界中,数据总是包含着自然变异(natural variation)。即使新旧模型完全相同,处理组和对照组的月度胜率也会因为随机性而略有差异。

This is the core question of statistics. In the real world, data always contains natural variation. Even if the new and old models were exactly the same, the monthly win rates of the treatment and control groups would still differ slightly due to randomness.

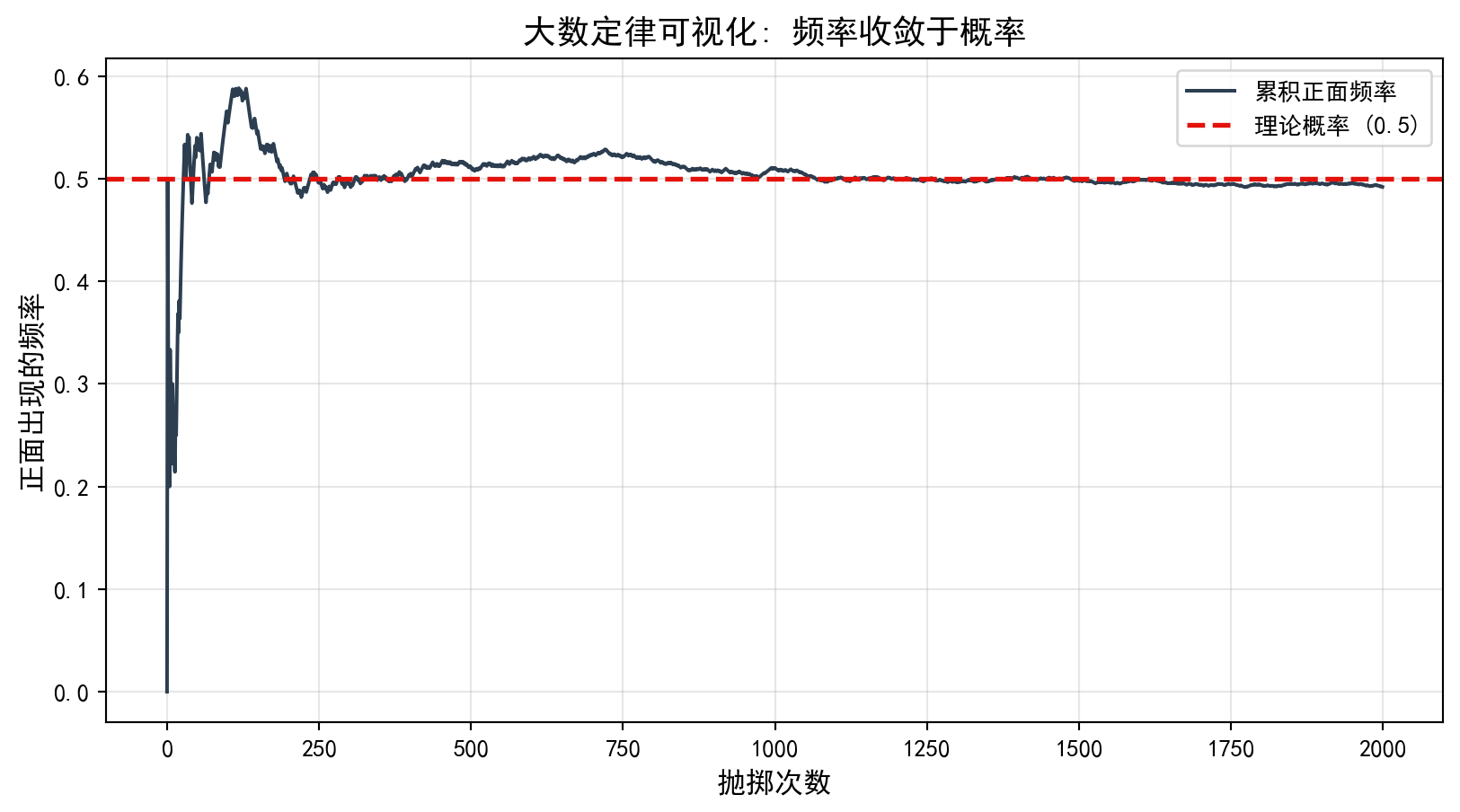

直觉可视化:大数定律 (Law of Large Numbers)

Intuitive Visualization: The Law of Large Numbers

为什么我们相信样本能代表总体?核心基石是大数定律。 它告诉我们:随着样本量 \(n\) 的增加,样本均值 \(\bar{X}\) 会以概率 1 收敛到总体均值 \(\mu\)。

Why do we believe that a sample can represent a population? The cornerstone is the Law of Large Numbers. It tells us that as the sample size \(n\) increases, the sample mean \(\bar{X}\) converges to the population mean \(\mu\) with probability 1.

我们可以通过一个简单的 Python 模拟来”看见”这个定律。

We can “see” this law through a simple Python simulation.

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import numpy as np # 导入数值计算库

# Import the numerical computation library

import matplotlib.pyplot as plt # 导入绑图库

# Import the plotting library

# ========== 模拟抛硬币实验 ==========

# ========== Simulate coin-flipping experiment ==========

np.random.seed(42) # 设定随机数种子,确保结果可复现

# Set random seed for reproducibility

num_coin_flip_trials = 2000 # 总抛掷次数设为2000次

# Set total number of flips to 2000

coin_flip_results = np.random.randint(0, 2, num_coin_flip_trials) # 生成2000个0或1的随机数(0=反面, 1=正面)

# Generate 2000 random integers of 0 or 1 (0 = tails, 1 = heads)

# 计算累积正面频率: 前 n 次中正面出现的比例

# Calculate cumulative heads frequency: proportion of heads in the first n flips

cumulative_mean_frequencies = np.cumsum(coin_flip_results) / (np.arange(num_coin_flip_trials) + 1) # 计算前n次抛掷中正面出现的累积频率

# Calculate the cumulative frequency of heads in the first n flips

# ========== 绘制大数定律可视化图 ==========

# ========== Plot the Law of Large Numbers visualization ==========

plt.figure(figsize=(10, 5)) # 创建10x5英寸的画布

# Create a 10x5-inch canvas

plt.plot(cumulative_mean_frequencies, color='#2C3E50', linewidth=1.5, label='累积正面频率') # 绘制频率曲线

# Plot the frequency curve

plt.axhline(0.5, color='#E3120B', linestyle='--', linewidth=2, label='理论概率 (0.5)') # 绘制理论值参考线

# Plot the theoretical value reference line

plt.xlabel('抛掷次数', fontsize=12) # X轴标签

# X-axis label

plt.ylabel('正面出现的频率', fontsize=12) # Y轴标签

# Y-axis label

plt.title('大数定律可视化: 频率收敛于概率', fontsize=14) # 图标题

# Chart title

plt.legend() # 显示图例

# Display legend

plt.grid(True, alpha=0.3) # 显示网格线,透明度为0.3

# Display grid lines with 0.3 transparency

plt.show() # 展示图形

# Display the figure

注意看图的前半部分:当次数很少时,频率波动巨大(可能连续几次正面,频率100%)。但随着次数增加,这条线就像被一种引力吸住一样,稳定在 0.5 附近。这就是统计推断的信心来源——数据越多,真相越清晰。

Pay attention to the first half of the chart: when the number of flips is small, the frequency fluctuates wildly (there might be several consecutive heads, bringing the frequency to 100%). But as the number of flips increases, the line is pulled as if by gravity, stabilizing around 0.5. This is the source of confidence in statistical inference—the more data, the clearer the truth.

1.2 数据基础与变量类型 (Data Fundamentals and Variable Types)

1.2.1 数据框结构 (Data Frame Structure)

在Python中,pandas库提供的DataFrame是处理统计数据的核心数据结构。数据框(data frame)是一个二维表格,其中:

In Python, the DataFrame provided by the pandas library is the core data structure for handling statistical data. A data frame is a two-dimensional table in which:

每一行(row):代表一个观测单元(observation)或案例(case)

每一列(column):代表一个变量(variable)

Each row: represents an observation unit or case

Each column: represents a variable

让我们通过一个真实的A股市场数据示例来理解数据框结构。如 表 1.2 所示,我们展示了2023年中国长三角地区部分上市公司的基本信息。

Let us understand the data frame structure through a real example from the A-share market. As shown in 表 1.2, we display the basic information of some listed companies in China’s Yangtze River Delta region.

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import pandas as pd # 导入数据分析库 pandas

# Import the pandas data analysis library

import platform # 导入平台检测库,用于自动适配数据路径

# Import the platform detection library for auto-adapting data paths

# ========== 设置本地数据路径 ==========

# ========== Set local data paths ==========

if platform.system() == 'Windows': # 判断当前操作系统类型

# Check the current operating system type

data_path = 'C:/qiufei/data/stock' # Windows 数据路径

# Data path for Windows

else: # Linux 系统下使用服务器数据路径

# Use server data path on Linux

data_path = '/home/ubuntu/r2_data_mount/qiufei/data/stock' # Linux 数据路径

# Data path for Linux

# ========== 读取并筛选数据 ==========

# ========== Load and filter data ==========

stock_basic_dataframe = pd.read_hdf(f'{data_path}/stock_basic_data.h5') # 读取上市公司基本信息

# Load basic information of listed companies

# 定义长三角地区包含的省份列表

# Define the list of provinces in the Yangtze River Delta region

yangtze_delta_city_list = ['上海市', '浙江省', '江苏省', '安徽省'] # 长三角四省市对应的行政区划名称

# Administrative division names for the four YRD provinces/municipalities

# 筛选注册地在长三角地区的公司,取前10条做示例展示

# Filter companies registered in the YRD region, take the first 10 for demonstration

sampled_stock_dataframe = stock_basic_dataframe[stock_basic_dataframe['province'].isin(yangtze_delta_city_list)].head(10) # 筛选长三角公司并取前10条

# Filter YRD companies and take the first 10

# ========== 输出结果 ==========

# ========== Output results ==========

print(f'数据框维度: {sampled_stock_dataframe.shape[0]}行 {sampled_stock_dataframe.shape[1]}列') # 打印数据框的行数和列数

# Print the number of rows and columns of the data frame

# 选取关键字段展示: 股票代码、简称、省份、行业、上市日期

# Select key fields for display: stock code, abbreviation, province, industry, listing date

sampled_stock_dataframe[['order_book_id', 'abbrev_symbol', 'province', 'industry_name', 'listed_date']] # 输出选定字段的数据表

# Output the data table with selected fields数据框维度: 10行 24列| order_book_id | abbrev_symbol | province | industry_name | listed_date | |

|---|---|---|---|---|---|

| 34 | 000035.XSHE | ZGTY | 江苏省 | 生态保护和环境治理业 | 1994-04-08 |

| 70 | 000153.XSHE | FYYY | 安徽省 | 医药制造业 | 2000-09-20 |

| 72 | 000156.XSHE | HSCM | 浙江省 | 广播、电视、电影和影视录音制作业 | 2000-09-06 |

| 77 | 000301.XSHE | DFSH | 江苏省 | 化学纤维制造业 | 2000-05-29 |

| 91 | 000411.XSHE | YTJT | 浙江省 | 批发业 | 1996-07-16 |

| 96 | 000417.XSHE | HBJT | 安徽省 | 零售业 | 1996-08-12 |

| 97 | 000418.XSHE | XTEA | 江苏省 | 未知 | 1997-03-28 |

| 100 | 000421.XSHE | NJGY | 江苏省 | 燃气生产和供应业 | 1996-08-06 |

| 103 | 000425.XSHE | XGJX | 江苏省 | 专用设备制造业 | 1996-08-28 |

| 125 | 000517.XSHE | RADC | 浙江省 | 房地产业 | 1993-08-06 |

上面的代码从本地数据文件中读取了中国A股上市公司的基本信息,并筛选出长三角地区(上海、浙江、江苏、安徽)的公司样本。表 1.2 的输出结果是一个典型的数据框:表中每一行对应一家上市公司(即一个观测单元),各列则代表不同的变量,如 order_book_id(股票代码)、abbrev_symbol(股票简称)、province(注册省份)、industry_name(所属行业)和 listed_date(上市日期)。这种”行=观测、列=变量”的二维表格结构,就是贯穿整本教材的核心数据组织形式。

The above code reads the basic information of Chinese A-share listed companies from local data files, filtering for companies in the Yangtze River Delta region (Shanghai, Zhejiang, Jiangsu, and Anhui). The output of 表 1.2 is a typical data frame: each row corresponds to a listed company (i.e., an observation unit), and each column represents a different variable, such as order_book_id (stock code), abbrev_symbol (stock abbreviation), province (registered province), industry_name (industry classification), and listed_date (listing date). This “row = observation, column = variable” two-dimensional table structure is the core data organization form used throughout this textbook.

1.2.2 变量的类型体系 (The Variable Type System)

理解变量类型是统计分析的基础。如 图 1.3 所示,变量可以分为两大类:数值变量和分类变量。

Understanding variable types is the foundation of statistical analysis. As shown in 图 1.3, variables can be divided into two broad categories: numerical variables and categorical variables.

1.2.2.1 1. 数值变量 (Numerical/Quantitative Variables)

数值变量可以取具体的数值,可以进行算术运算。

Numerical variables take specific numeric values and can be subjected to arithmetic operations.

离散变量(Discrete Variables):只能取离散的、分离的值,通常是整数计数。

Discrete Variables: Can only take discrete, separated values, usually integer counts.

- 特征:可能取值是可数的(0, 1, 2, 3…)

- 中国商业案例:

- 阿里巴巴的年度活跃用户数:10.39亿(2024财年)

- 上汽集团的年销量:约500万辆

- 每日A股成交订单数:数千万笔

- Characteristics: Possible values are countable (0, 1, 2, 3…)

- Chinese business examples:

- Alibaba’s annual active users: 1.039 billion (FY2024)

- SAIC Motor’s annual sales: approximately 5 million vehicles

- Daily A-share trading orders: tens of millions

连续变量(Continuous Variables):可以在一个范围内取任何值,理论上可以无限细分。

Continuous Variables: Can take any value within a range, theoretically infinitely divisible.

- 特征:可能取值是无限可分的

- 中国商业案例:

- 海康威视股价:30-40元/股(可精确到0.01元)

- 海康威视年营收:891.6亿元(2023年)

- 上汽集团汽车产量:502万辆(可精确到辆)

- Characteristics: Possible values are infinitely divisible

- Chinese business examples:

- Hikvision stock price: 30–40 yuan/share (precise to 0.01 yuan)

- Hikvision annual revenue: 89.16 billion yuan (2023)

- SAIC Motor vehicle production: 5.02 million units (precise to the individual unit)

离散 vs 连续的判断准则 (Criteria for Distinguishing Discrete vs. Continuous)

判断一个变量是离散还是连续,关键看可能取值之间是否有”间隙”:

The key to determining whether a variable is discrete or continuous is whether there are “gaps” between possible values:

问题:公司的年收入是离散还是连续?

Question: Is a company’s annual revenue discrete or continuous?

分析:

Analysis:

理论上,收入可以取任何正值,是连续的

但实践中,我们记录到万元或亿元单位

判断标准:这个变量能否取更精细的值?如果能,则是连续的

In theory, revenue can take any positive value and is continuous

In practice, we record it in units of ten thousand or hundred million yuan

Criterion: Can this variable take more precise values? If yes, it is continuous

结论:年收入是连续变量,因为理论上可以精确到分。

Conclusion: Annual revenue is a continuous variable because, in theory, it can be precise to the cent.

1.2.2.2 2. 分类变量 (Categorical/Qualitative Variables)

分类变量代表类别或标签,不能进行算术运算。

Categorical variables represent categories or labels and cannot be subjected to arithmetic operations.

名义变量(Nominal Variables):代表类别或标签,没有内在顺序。

Nominal Variables: Represent categories or labels with no inherent order.

- 特征:类别之间没有优先级或顺序

- 中国商业案例:

- 证券交易所:上交所(SH) vs 深交所(SZ) vs 北交所(BJ)

- 行业分类:金融、科技、制造、消费、医药

- 支付方式:微信支付、支付宝、银联卡、现金

- 公司总部所在地:上海、北京、深圳、杭州

- Characteristics: No priority or ordering among categories

- Chinese business examples:

- Stock exchanges: SSE (SH) vs. SZSE (SZ) vs. BSE (BJ)

- Industry classification: Finance, Technology, Manufacturing, Consumer, Pharmaceuticals

- Payment methods: WeChat Pay, Alipay, UnionPay card, Cash

- Company headquarters: Shanghai, Beijing, Shenzhen, Hangzhou

名义变量的不同取值称为水平(levels)或类别。

The different values of a nominal variable are called levels or categories.

有序变量(Ordinal Variables):具有顺序或排名,但水平之间的间隔不一定均匀。

Ordinal Variables: Have order or ranking, but the intervals between levels are not necessarily uniform.

- 特征:有顺序关系,但间隔不确定

- 中国商业案例:

- 信用评级:AAA > AA > A > BBB(相邻级别之间的风险差异不等)

- 股票分析师评级:强烈买入 > 买入 > 持有 > 卖出 > 强烈卖出

- 客户满意度:非常满意 > 满意 > 一般 > 不满意 > 非常不满意

- 教育程度:博士 > 硕士 > 本科 > 大专 > 高中

- Characteristics: Have ordering relationships, but intervals are uncertain

- Chinese business examples:

- Credit ratings: AAA > AA > A > BBB (risk differences between adjacent levels are not equal)

- Stock analyst ratings: Strong Buy > Buy > Hold > Sell > Strong Sell

- Customer satisfaction: Very Satisfied > Satisfied > Neutral > Dissatisfied > Very Dissatisfied

- Education level: Doctorate > Master’s > Bachelor’s > Associate > High School

重要警示:数字不等于数值变量 (Important Warning: Numbers Do Not Equal Numerical Variables)

这是一个常见的陷阱!有些变量用数字表示但其实是分类变量。

This is a common trap! Some variables are represented by numbers but are actually categorical variables.

典型案例:

Typical examples:

- 邮政编码:上海200000,北京100000

- 计算”平均邮政编码”没有意义

- 这是名义变量

- Postal codes: Shanghai 200000, Beijing 100000

- Calculating an “average postal code” is meaningless

- This is a nominal variable

- 身份证号:虽然全是数字,但完全不能进行算术运算

- 这是名义变量

- National ID numbers: Although entirely composed of digits, arithmetic operations are completely meaningless

- This is a nominal variable

- 股票代码:600000(浦发银行),002142(宁波银行)

- 只是标识符,不能加减乘除

- 这是名义变量

- Stock codes: 600000 (SPD Bank), 002142 (Bank of Ningbo)

- These are merely identifiers; arithmetic operations are meaningless

- This is a nominal variable

- Likert量表:1=非常不同意,2=不同意,3=中立,4=同意,5=非常同意

- 可以计算均值(有争议),但要注意间隔不一定相等

- 通常作为有序变量处理

- Likert scale: 1 = Strongly Disagree, 2 = Disagree, 3 = Neutral, 4 = Agree, 5 = Strongly Agree

- One can compute the mean (controversial), but note that intervals are not necessarily equal

- Usually treated as an ordinal variable

判断标准:对这个变量进行算术运算(加、减、乘、除)是否有实际意义?

Criterion: Do arithmetic operations (addition, subtraction, multiplication, division) on this variable have practical meaning?

1.2.3 变量类型与统计方法的关系 (The Relationship Between Variable Types and Statistical Methods)

不同的变量类型适合不同的统计方法,这在后续章节会详细讨论。

Different variable types are suitable for different statistical methods, which will be discussed in detail in subsequent chapters.

对于数值变量(无论是离散还是连续):

For numerical variables (whether discrete or continuous):

可以计算:均值、中位数、方差、标准差

可以进行:加减乘除、对数变换、标准化

适合使用:t检验、方差分析、回归分析、相关分析

Can compute: mean, median, variance, standard deviation

Can perform: arithmetic, logarithmic transformation, standardization

Suitable methods: t-test, ANOVA, regression analysis, correlation analysis

对于分类变量(无论是名义还是有序):

For categorical variables (whether nominal or ordinal):

只能计算:频数、频率、百分比

适合使用:卡方检验、列联表分析、逻辑回归

Can only compute: frequency, relative frequency, percentage

Suitable methods: chi-square test, contingency table analysis, logistic regression

实践中的处理方式 (Practical Handling)

在实际数据分析中,有时会将分类变量转换为数值变量:

In practice, categorical variables are sometimes converted to numerical variables:

示例:将性别(男/女)转换为虚拟变量(0/1)

Example: Converting gender (male/female) to a dummy variable (0/1)

男 = 0, 女 = 1

这样就可以在回归分析中使用

但要注意:0和1只是编码,不是真正的数值

Male = 0, Female = 1

This allows use in regression analysis

But note: 0 and 1 are just codes, not real numerical values

示例:将教育程度转换为数值

Example: Converting education level to numerical values

高中=12,本科=16,硕士=18,博士=21

使用受教育年限代表教育程度

这样就变成了数值变量

High school = 12, Bachelor’s = 16, Master’s = 18, Doctorate = 21

Using years of education to represent education level

This transforms it into a numerical variable

1.3 变量之间的关系 (Relationships Between Variables)

在实际商业分析中,我们不仅关注单个变量,更关注变量之间的关系。以下通过三个中国金融市场案例来展示不同类型的变量关系。

In real business analysis, we are interested not only in individual variables but also in the relationships between variables. The following three cases from the Chinese financial market illustrate different types of variable relationships.

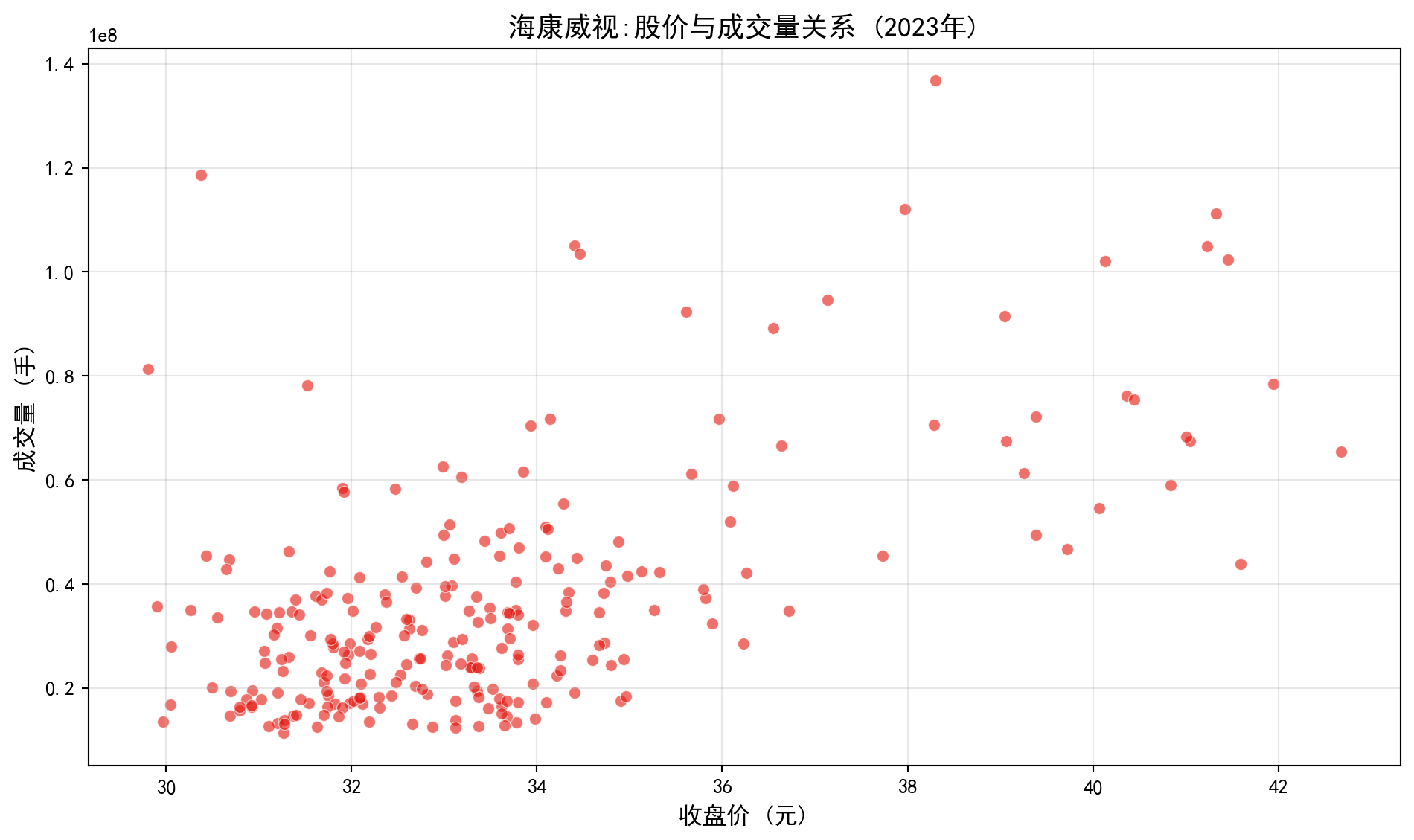

1.3.0.1 案例1:负相关关系 - 海康威视股价与成交量 (Case 1: Negative Association — Hikvision Stock Price vs. Trading Volume)

公司股价与成交量之间存在着怎样的关系?这是投资分析中的经典议题。我们将以海康威视(002415.XSHE)——中国安防行业龙头、长三角代表性上市公司——为研究对象,利用其2023年全年的真实交易数据进行分析。

What is the relationship between a company’s stock price and its trading volume? This is a classic topic in investment analysis. We will study Hikvision (002415.XSHE) — the leading company in China’s security industry and a representative listed company in the Yangtze River Delta — using its real trading data for the entire year of 2023.

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import pandas as pd # 数据分析库

# Data analysis library

import numpy as np # 数值计算库

# Numerical computation library

import matplotlib.pyplot as plt # 绘图库

# Plotting library

import seaborn as sns # 统计可视化库

# Statistical visualization library

import platform # 平台检测库

# Platform detection library

# ========== 中文字体配置 ==========

# ========== Chinese font configuration ==========

plt.rcParams['font.sans-serif'] = ['SimHei', 'Microsoft YaHei'] # 设置中文字体

# Set Chinese fonts

plt.rcParams['axes.unicode_minus'] = False # 解决负号显示问题

# Fix the minus sign display issue

# ========== 设置本地数据路径 ==========

# ========== Set local data paths ==========

if platform.system() == 'Windows': # 判断当前操作系统类型

# Check the current operating system type

data_path = 'C:/qiufei/data/stock' # Windows 数据路径

# Data path for Windows

else: # Linux 系统下使用服务器数据路径

# Use server data path on Linux

data_path = '/home/ubuntu/r2_data_mount/qiufei/data/stock' # Linux 数据路径

# Data path for Linux

# ========== 读取并筛选数据 ==========

# ========== Load and filter data ==========

stock_price_dataframe = pd.read_hdf(f'{data_path}/stock_price_pre_adjusted.h5') # 读取前复权股价数据

# Load pre-adjusted stock price data

stock_price_dataframe = stock_price_dataframe.reset_index() # 将多级索引转为普通列

# Convert multi-level index to regular columns

# 筛选海康威视(002415.XSHE)2023年全年的交易数据

# Filter Hikvision (002415.XSHE) trading data for the full year 2023

hikvision_prices_dataframe = stock_price_dataframe[ # 基于布尔条件筛选海康威视全年行情

# Filter Hikvision full-year data using boolean conditions

(stock_price_dataframe['order_book_id'] == '002415.XSHE') & # 匹配海康威视股票代码

# Match the Hikvision stock code

(stock_price_dataframe['date'] >= '2023-01-01') & # 起始日期为2023年1月1日

# Start date: January 1, 2023

(stock_price_dataframe['date'] <= '2023-12-31') # 截止日期为2023年12月31日

# End date: December 31, 2023

].copy() # 使用 .copy() 避免 SettingWithCopyWarning

# Use .copy() to avoid SettingWithCopyWarning

hikvision_prices_dataframe = hikvision_prices_dataframe.sort_values('date') # 按日期升序排列

# Sort by date in ascending order上述代码完成了数据读取和筛选:首先加载本地存储的前复权日度行情数据,然后使用布尔索引筛选出海康威视2023年全年的交易数据(共约244个交易日)。.copy() 方法用于创建独立副本,避免后续操作中出现 SettingWithCopyWarning 警告。.sort_values('date') 确保数据按日期从早到晚排列。

The above code completes data loading and filtering: first it loads locally stored pre-adjusted daily trading data, then uses boolean indexing to filter Hikvision’s trading data for the full year of 2023 (approximately 244 trading days). The .copy() method creates an independent copy to avoid SettingWithCopyWarning in subsequent operations. .sort_values('date') ensures the data is sorted chronologically.

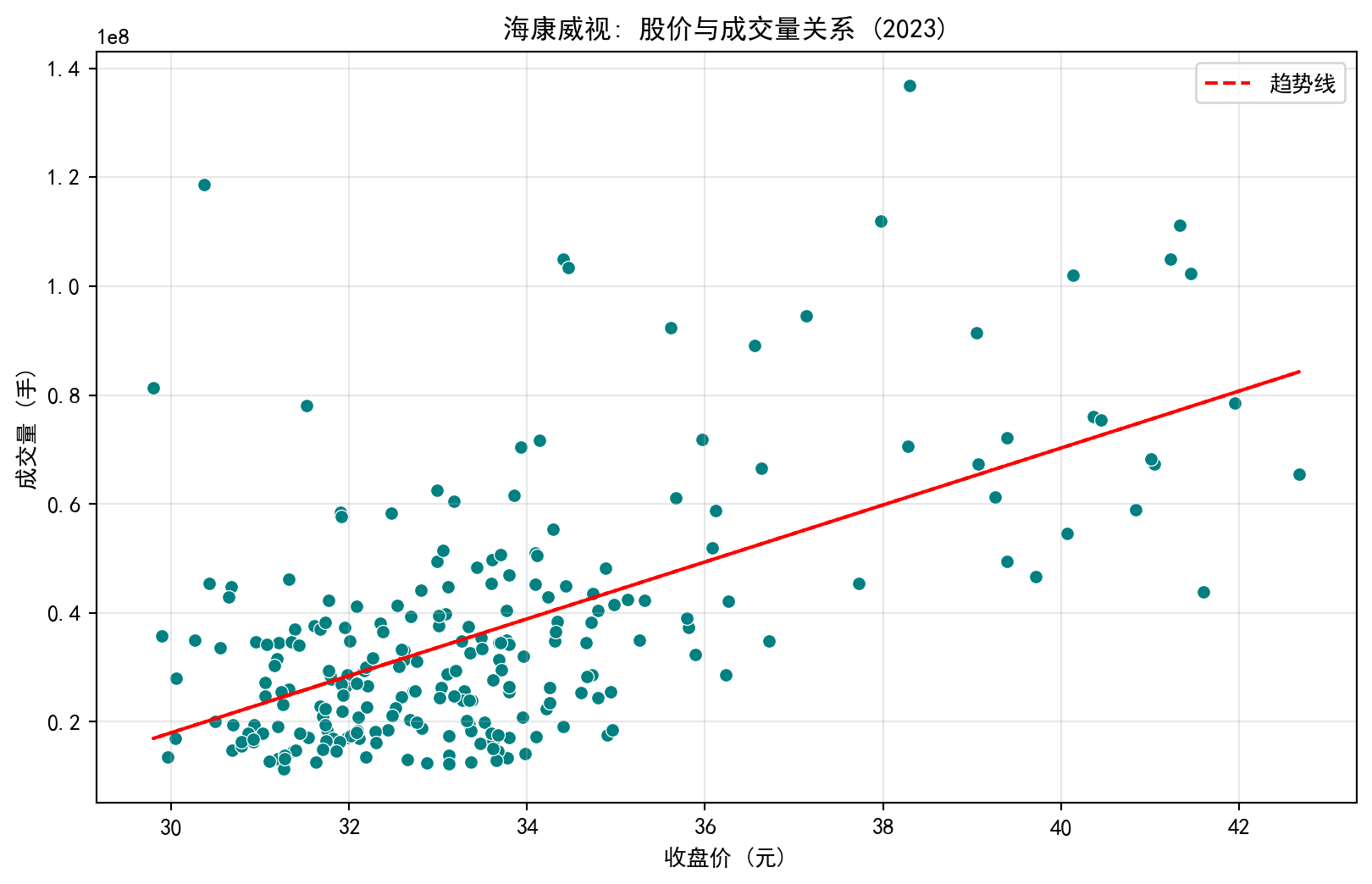

下面使用 seaborn 库的 scatterplot 函数绘制散点图(scatter plot),其中X轴为每日收盘价,Y轴为每日成交量。散点图是观察两个数值变量之间关系最直接的可视化工具。

Below we use the scatterplot function from the seaborn library to draw a scatter plot, where the X-axis is the daily closing price and the Y-axis is the daily trading volume. The scatter plot is the most direct visualization tool for observing the relationship between two numerical variables.

# ========== 绘制散点图 ==========

# ========== Draw scatter plot ==========

plt.figure(figsize=(10, 6)) # 创建10x6英寸的画布

# Create a 10x6-inch canvas

sns.scatterplot(data=hikvision_prices_dataframe, x='close', y='volume', alpha=0.6, color='#E3120B') # 绘制散点图

# Draw scatter plot

plt.xlabel('收盘价 (元)', fontsize=12) # X轴: 收盘价

# X-axis: closing price

plt.ylabel('成交量 (手)', fontsize=12) # Y轴: 成交量

# Y-axis: trading volume

plt.title('海康威视:股价与成交量关系 (2023年)', fontsize=14, fontweight='bold') # 图标题

# Chart title

plt.grid(True, alpha=0.3) # 显示网格线

# Display grid lines

plt.tight_layout() # 自动调整布局避免截断

# Automatically adjust layout to avoid clipping

plt.show() # 展示图形

# Display the figure

图 1.4 展示了股价与成交量的关系。从图中可以看出:

图 1.4 shows the relationship between stock price and trading volume. From the chart we can see:

当股价上涨时,成交量往往下降

这是一种负相关关系

可能的解释:股价高时,投资者观望情绪浓厚,交易减少

When the stock price rises, trading volume tends to decrease

This is a negative association

Possible explanation: When stock prices are high, investor sentiment turns cautious, and trading decreases

1.3.0.2 案例2:正相关关系 - 营业收入与净利润 (Case 2: Positive Association — Revenue vs. Net Profit)

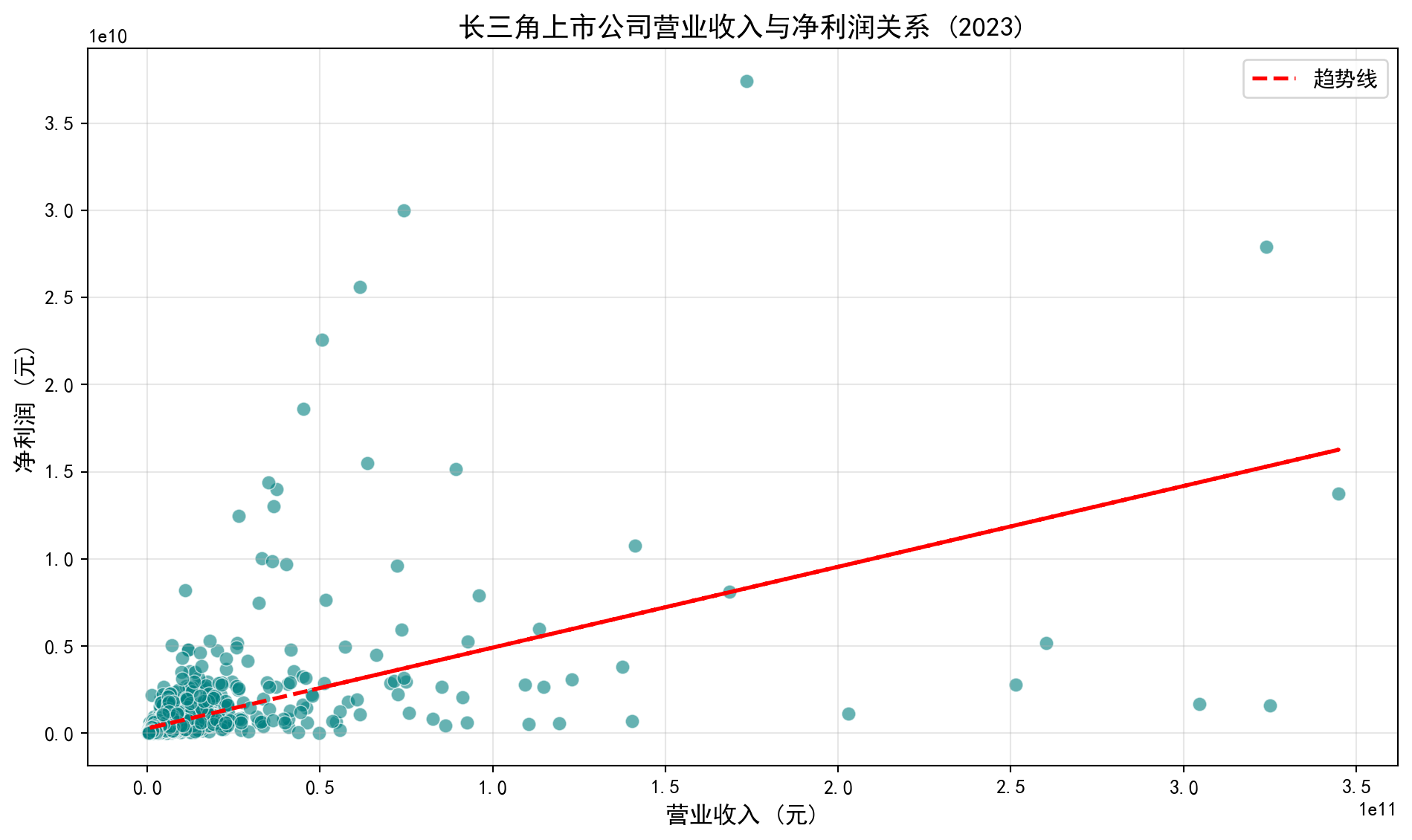

企业的营业收入与净利润之间通常存在正相关关系:收入越高的企业,利润往往也越高(假设利润率保持相对稳定)。我们将使用中国A股上市公司的真实财务报表数据来验证这一关系。具体做法是:从本地财务数据中筛选长三角地区(上海、浙江、江苏、安徽)上市公司2023年年报数据,然后绘制营业收入与净利润的散点图。

There is usually a positive correlation between a company’s revenue and net profit: companies with higher revenue tend to have higher profits (assuming profit margins remain relatively stable). We will use real financial statement data from Chinese A-share listed companies to verify this relationship. Specifically, we will filter 2023 annual report data for YRD-region listed companies from local financial data, and then draw a scatter plot of revenue versus net profit.

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import pandas as pd # 数据分析库

# Data analysis library

import numpy as np # 数值计算库

# Numerical computation library

import matplotlib.pyplot as plt # 绘图库

# Plotting library

import seaborn as sns # 统计可视化库

# Statistical visualization library

import platform # 平台检测库

# Platform detection library

# ========== 中文字体配置 ==========

# ========== Chinese font configuration ==========

plt.rcParams['font.sans-serif'] = ['SimHei', 'Microsoft YaHei'] # 设置中文字体

# Set Chinese fonts

plt.rcParams['axes.unicode_minus'] = False # 解决负号显示问题

# Fix the minus sign display issue

# ========== 设置本地数据路径 ==========

# ========== Set local data paths ==========

if platform.system() == 'Windows': # 判断当前操作系统类型

# Check the current operating system type

data_path = 'C:/qiufei/data/stock' # Windows 数据路径

# Data path for Windows

else: # Linux 系统下使用服务器数据路径

# Use server data path on Linux

data_path = '/home/ubuntu/r2_data_mount/qiufei/data/stock' # Linux 数据路径

# Data path for Linux

# ========== 读取数据 ==========

# ========== Load data ==========

financial_statement_dataframe = pd.read_hdf(f'{data_path}/financial_statement.h5') # 读取上市公司财务报表数据

# Load listed company financial statement data

stock_basic_dataframe = pd.read_hdf(f'{data_path}/stock_basic_data.h5') # 读取上市公司基本信息

# Load listed company basic information上述代码从本地加载了两个核心数据集:financial_statement.h5 包含所有A股上市公司2005-2025年的季度财务报表数据(包括营业收入、净利润等指标);stock_basic_data.h5 包含上市公司的基本信息(股票代码、公司名称、所在省份、行业分类等)。

The above code loads two core datasets from local storage: financial_statement.h5 contains quarterly financial statement data for all A-share listed companies from 2005 to 2025 (including revenue, net profit, etc.); stock_basic_data.h5 contains basic information about listed companies (stock code, company name, province, industry classification, etc.).

下面对数据进行筛选和清洗:首先筛选2023年第四季度报告(即年报),然后限定为长三角地区的公司,最后去除营收或利润为负数或极端值的异常记录,以确保散点图的可读性。

Below we filter and clean the data: first selecting Q4 2023 reports (i.e., annual reports), then restricting to YRD-region companies, and finally removing abnormal records with negative or extreme values for revenue or profit to ensure the scatter plot’s readability.

# ========== 筛选长三角地区2023年年报数据 ==========

# ========== Filter YRD region 2023 annual report data ==========

financial_data_2023 = financial_statement_dataframe[financial_statement_dataframe['quarter'] == '2023q4'].copy() # 筛选四季度报(年报)

# Filter Q4 reports (annual reports)

yangtze_delta_city_list = ['上海市', '浙江省', '江苏省', '安徽省'] # 长三角地区省份列表

# List of YRD provinces

target_stocks_dataframe = stock_basic_dataframe[stock_basic_dataframe['province'].isin(yangtze_delta_city_list)] # 筛选长三角公司

# Filter YRD companies

# 合并财务数据与公司基本信息

# Merge financial data with company basic information

merged_financial_dataframe = pd.merge(financial_data_2023, target_stocks_dataframe, on='order_book_id') # 按股票代码合并财务数据与公司信息

# Merge financial data and company info by stock code

# 筛选出收入和利润在合理范围内的非极端异常值公司进行展示,避免图像失真(营收在0到5000亿,净利润0到500亿)

# Filter companies with revenue and profit within reasonable ranges to avoid chart distortion

cleaned_financial_dataframe = merged_financial_dataframe[ # 基于营收和净利润的合理范围进行筛选

# Filter based on reasonable ranges for revenue and net profit

(merged_financial_dataframe['revenue'] > 0) & # 营收大于零(排除异常值)

# Revenue greater than zero (exclude anomalies)

(merged_financial_dataframe['revenue'] < 5e11) & # 营收小于5000亿元(排除极端值)

# Revenue less than 500 billion yuan (exclude extreme values)

(merged_financial_dataframe['net_profit'] > 0) & # 净利润大于零(排除亏损企业)

# Net profit greater than zero (exclude loss-making companies)

(merged_financial_dataframe['net_profit'] < 5e10) # 净利润小于500亿元(排除极端值)

# Net profit less than 50 billion yuan (exclude extreme values)

].copy() # 复制筛选结果避免链式赋值警告

# Copy filtered result to avoid chained assignment warning

cleaned_financial_dataframe = cleaned_financial_dataframe.dropna(subset=['revenue', 'net_profit']) # 剔除存在NaN的记录

# Remove records containing NaN数据筛选与清洗完成。上述代码通过多个条件(营收大于0且小于5000亿、净利润大于0且小于500亿)过滤掉了亏损企业和极端值公司。pd.merge() 函数将财务数据与公司基本信息按股票代码(order_book_id)进行合并,使我们能够同时获取每家公司的财务指标和地区信息。

Data filtering and cleaning are complete. The above code filters out loss-making companies and extreme-value companies using multiple conditions (revenue > 0 and < 500 billion, net profit > 0 and < 50 billion). The pd.merge() function merges financial data with company basic information by stock code (order_book_id), enabling us to access both financial metrics and regional information for each company.

下面使用散点图和趋势线(trend line)来可视化营业收入与净利润的关系。趋势线通过最小二乘法拟合一元线性回归得到,直观展示两个变量的线性关系方向和强度。

Below we use a scatter plot and trend line to visualize the relationship between revenue and net profit. The trend line is obtained by fitting a simple linear regression using ordinary least squares, intuitively showing the direction and strength of the linear relationship between the two variables.

# ========== 绘制散点图与趋势线 ==========

# ========== Draw scatter plot and trend line ==========

plt.figure(figsize=(10, 6)) # 创建10x6英寸画布

# Create a 10x6-inch canvas

sns.scatterplot(data=cleaned_financial_dataframe, x='revenue', y='net_profit', s=50, color='#008080', alpha=0.6) # 绘制散点图

# Draw scatter plot

# 添加一次线性趋势线: 利用最小二乘法拟合一元线性回归

# Add a linear trend line: fit simple linear regression using least squares

trend_line_coefficients = np.polyfit(cleaned_financial_dataframe['revenue'], cleaned_financial_dataframe['net_profit'], 1) # 拟合一次多项式系数

# Fit first-degree polynomial coefficients

trend_line_polynomial = np.poly1d(trend_line_coefficients) # 构建多项式函数

# Build polynomial function

plt.plot(cleaned_financial_dataframe['revenue'], trend_line_polynomial(cleaned_financial_dataframe['revenue']), 'r--', linewidth=2, label='趋势线') # 绘制红色虚线趋势线

# Draw red dashed trend line

plt.xlabel('营业收入 (元)', fontsize=12) # X轴: 营业收入

# X-axis: Revenue

plt.ylabel('净利润 (元)', fontsize=12) # Y轴: 净利润

# Y-axis: Net profit

plt.title('长三角上市公司营业收入与净利润关系 (2023)', fontsize=14, fontweight='bold') # 图标题

# Chart title

plt.legend(fontsize=11) # 显示图例

# Display legend

plt.grid(True, alpha=0.3) # 显示网格线

# Display grid lines

plt.tight_layout() # 自动调整布局

# Automatically adjust layout

plt.show() # 展示图形

# Display the figure

图 1.5 展示了营业收入与净利润的强正相关关系:

图 1.5 shows the strong positive correlation between revenue and net profit:

营业收入增长,净利润也随之增长

这是一种正相关关系

商业原理:在利润率保持相对稳定的情况下,企业规模的扩张往往带来绝对利润的增长

As revenue grows, net profit grows accordingly

This is a positive association

Business rationale: When profit margins remain relatively stable, expansion of firm scale generally leads to growth in absolute profit

1.3.0.3 案例3:无关联关系 - 公司注册地与ROE (Case 3: No Association — Company Location vs. ROE)

前两个案例展示了变量之间存在明确关系(正相关和负相关)的情况。然而,并非所有变量之间都存在有意义的统计关系。本案例将检验一个直觉假设:公司的注册地(分类变量)是否与其盈利能力ROE(数值变量)有关。ROE(Return on Equity,净资产收益率)是衡量企业盈利能力的核心财务指标,计算公式为:净利润 ÷ 归属母公司股东权益 × 100%。我们将从长三角四省市各取若干上市公司,比较它们的ROE分布。

The previous two cases demonstrated clear relationships (positive and negative correlations) between variables. However, not all variables have meaningful statistical relationships. This case examines an intuitive hypothesis: is a company’s registered location (categorical variable) related to its profitability ROE (numerical variable)? ROE (Return on Equity) is a core financial metric measuring corporate profitability, calculated as: Net Profit ÷ Equity Attributable to Parent Company Shareholders × 100%. We will take several listed companies from each of the four YRD provinces/municipalities and compare their ROE distributions.

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import pandas as pd # 数据分析库

# Data analysis library

import numpy as np # 数值计算库

# Numerical computation library

import matplotlib.pyplot as plt # 绘图库

# Plotting library

import seaborn as sns # 统计可视化库

# Statistical visualization library

import platform # 平台检测库

# Platform detection library

# ========== 设置本地数据路径 ==========

# ========== Set local data paths ==========

if platform.system() == 'Windows': # 判断当前操作系统类型

# Check the current operating system type

data_path = 'C:/qiufei/data/stock' # Windows 数据路径

# Data path for Windows

else: # Linux 系统下使用服务器数据路径

# Use server data path on Linux

data_path = '/home/ubuntu/r2_data_mount/qiufei/data/stock' # Linux 数据路径

# Data path for Linux

# ========== 读取数据 ==========

# ========== Load data ==========

stock_basic_dataframe = pd.read_hdf(f'{data_path}/stock_basic_data.h5') # 读取上市公司基本信息

# Load listed company basic information

financial_statement_dataframe = pd.read_hdf(f'{data_path}/financial_statement.h5') # 读取财务报表数据

# Load financial statement data

# ========== 筛选长三角地区公司 ==========

# ========== Filter YRD region companies ==========

target_city_list = ['上海市', '浙江省', '江苏省', '安徽省'] # 长三角地区省份列表

# List of YRD provinces

target_stocks_dataframe = stock_basic_dataframe[stock_basic_dataframe['province'].isin(target_city_list)].head(50).copy() # 取前50家公司

# Take the first 50 companies上述代码筛选了注册地在长三角四省市(上海、浙江、江苏、安徽)的上市公司,并取前50家作为样本。.head(50) 限制样本量是为了让散点图更清晰易读。

The above code filters listed companies registered in the four YRD provinces/municipalities (Shanghai, Zhejiang, Jiangsu, and Anhui), taking the first 50 as the sample. .head(50) limits the sample size to make the scatter plot clearer and more readable.

下面的代码从财务报表中获取每家公司最新一期的财务数据,然后计算ROE(净资产收益率)。ROE = 净利润 ÷ 归属母公司股东权益 × 100%,数值越高表示公司每投入1元股东资本能产生越多的利润。

The code below retrieves the most recent financial data for each company from financial statements, then calculates ROE (Return on Equity). ROE = Net Profit ÷ Equity Attributable to Parent Company Shareholders × 100%; a higher value indicates the company generates more profit per yuan of shareholder capital invested.

# ========== 计算ROE (净资产收益率) ==========

# ========== Calculate ROE (Return on Equity) ==========

# 获取每只股票最新季度的财务数据(按季度降序排列后去重)

# Get the most recent quarterly financial data for each stock (sort by quarter descending, then deduplicate)

latest_financial_dataframe = financial_statement_dataframe.sort_values('quarter', ascending=False).drop_duplicates('order_book_id') # 按季度降序取每只股票最新一期数据

# Sort by quarter descending and keep only the latest record for each stock

# 计算ROE: 净利润 / 归属母公司股东权益 × 100 (转换为百分比)

# Calculate ROE: Net Profit / Equity Attributable to Parent × 100 (convert to percentage)

latest_financial_dataframe['roe'] = ( # 新增ROE列并赋值

# Add ROE column and assign values

latest_financial_dataframe['net_profit'] / latest_financial_dataframe['equity_parent_company'] * 100 # 净利润除以归母权益再乘100转百分比

# Net profit divided by parent equity times 100 to convert to percentage

) # 完成ROE指标的计算赋值

# Complete the ROE calculation

# 将ROE数据合并到公司基本信息表中

# Merge ROE data into the company basic information table

merged_stock_dataframe = target_stocks_dataframe.merge(latest_financial_dataframe[['order_book_id', 'roe']], on='order_book_id', how='left') # 左连接合并ROE数据到公司信息表

# Left join to merge ROE data into company info table

merged_stock_dataframe = merged_stock_dataframe.dropna(subset=['roe']) # 剔除ROE为空的记录

# Remove records where ROE is nullROE计算完成。上述代码中 .sort_values('quarter', ascending=False).drop_duplicates('order_book_id') 的作用是:对每只股票,按季度降序排列后保留第一条记录,从而获得最新一期的财务数据。.merge() 函数将ROE数据与公司基本信息合并。

ROE calculation is complete. In the above code, .sort_values('quarter', ascending=False).drop_duplicates('order_book_id') sorts each stock’s records by quarter in descending order and keeps only the first record, thereby obtaining the most recent financial data. The .merge() function combines ROE data with company basic information.

下面为各省份分配数字编码,将分类变量(省份名称)转换为数值,以便在散点图的X轴上展示。需要注意的是,这里的数字编码(0,1,2,3)仅用于绘图定位,不具有数学意义——这正是我们前面讲到的「分类变量不能进行数学运算」的例子。

Below we assign numeric codes to each province, converting the categorical variable (province name) to numerical values for display on the X-axis of the scatter plot. Note that these numeric codes (0, 1, 2, 3) are used solely for plotting positioning and carry no mathematical meaning — this is exactly the example of “categorical variables cannot be subjected to arithmetic operations” we discussed earlier.

# ========== 为城市分配数字编码(用于X轴) ==========

# ========== Assign numeric codes to cities (for X-axis) ==========

city_to_code_mapping = {city: i for i, city in enumerate(target_city_list)} # 构建城市→数字编码映射字典

# Build city-to-numeric-code mapping dictionary

merged_stock_dataframe['city_code'] = merged_stock_dataframe['province'].map(city_to_code_mapping) # 将省份映射为数字编码

# Map province to numeric code

# ========== 中文字体配置 ==========

# ========== Chinese font configuration ==========

plt.rcParams['font.sans-serif'] = ['SimHei', 'Microsoft YaHei'] # 设置中文字体

# Set Chinese fonts

plt.rcParams['axes.unicode_minus'] = False # 解决负号显示问题

# Fix the minus sign display issue

# ========== 绘制散点图 ==========

# ========== Draw scatter plot ==========

plt.figure(figsize=(10, 6)) # 创建10x6英寸画布

# Create a 10x6-inch canvas

sns.scatterplot(data=merged_stock_dataframe, x='city_code', y='roe', alpha=0.6, color='#F0A700') # 绘制散点图

# Draw scatter plot

plt.xlabel('城市编码', fontsize=12) # X轴: 城市编码

# X-axis: City code

plt.ylabel('ROE (%)', fontsize=12) # Y轴: 净资产收益率

# Y-axis: Return on Equity

plt.title('长三角城市与上市公司ROE关系', fontsize=14, fontweight='bold') # 图标题

# Chart title

plt.xticks(range(len(target_city_list)), target_city_list, rotation=45) # 将X轴刻度替换为城市名称

# Replace X-axis tick labels with city names

plt.grid(True, alpha=0.3, axis='y') # 仅显示Y轴方向网格线

# Display only Y-axis grid lines

plt.tight_layout() # 自动调整布局

# Automatically adjust layout

plt.show() # 展示图形

# Display the figure

图 1.6 展示了城市与ROE之间没有明显的系统关系:

图 1.6 shows that there is no clear systematic relationship between city and ROE:

不同城市的公司ROE分布相似

这是一种无关联关系

公司的盈利能力更多取决于自身经营,而非注册地

Companies in different cities have similar ROE distributions

This is a case of no association

A company’s profitability depends more on its own operations than on its registered location

1.3.1 关联不等于因果 (Association Does Not Imply Causation)

这是统计学中最重要的原则之一,也是最容易误解的概念。

This is one of the most important principles in statistics and also one of the most easily misunderstood concepts.

1.3.1.1 经典案例:空调销量与啤酒销量 (Classic Example: Air Conditioner Sales vs. Beer Sales)

在夏季,某零售平台发现空调销量和啤酒销量同时上升。两者高度相关,但显然:

In summer, a retail platform finds that air conditioner sales and beer sales both rise simultaneously. The two are highly correlated, but obviously:

购买空调不会导致购买更多啤酒

两者的真实关系:都与夏季高温相关

高温 → 空调需求上升

高温 → 啤酒需求上升

Buying air conditioners does not cause people to buy more beer

The real relationship: both are related to summer heat

High temperature → Increased demand for air conditioners

High temperature → Increased demand for beer

这种情况下,夏季温度是一个混淆变量(confounding variable)。

In this situation, summer temperature is a confounding variable.

1.3.1.2 中国商业案例 (Chinese Business Cases)

案例1:上海房价与深圳房价 (Case 1: Shanghai Housing Prices vs. Shenzhen Housing Prices)

观察:上海房价上涨,深圳房价也上涨

相关性强,但不是因果关系

真实原因:都受宏观经济政策、流动性宽松等因素影响

Observation: When Shanghai housing prices rise, Shenzhen housing prices also rise

The correlation is strong, but it is not a causal relationship

Real reason: Both are affected by macroeconomic policies, monetary easing, and other factors

案例2:高管学历与公司绩效 (Case 2: Executive Education vs. Company Performance)

- 观察:高学历CEO的公司往往绩效更好

- 但不能简单推断:高学历 → 公司绩效好

- 可能的混淆变量:

- 高学历CEO通常在更大、更成熟的公司

- 这些公司有更好的资源和品牌

- 公司规模和成熟度才是真正的影响因素

- Observation: Companies with highly educated CEOs tend to perform better

- But one cannot simply infer: High education → Good company performance

- Possible confounding variables:

- Highly educated CEOs are typically at larger, more mature companies

- These companies have better resources and brand recognition

- Company size and maturity are the real influencing factors

建立因果关系的条件 (Conditions for Establishing Causation)

要从关联推断因果,需要满足三个条件:

To infer causation from association, three conditions must be met:

时间顺序:原因必须在结果之前

强关联:两者之间有稳定的统计关联

排除混淆:控制其他可能的解释

Temporal order: The cause must precede the effect

Strong association: There is a stable statistical association between the two

Elimination of confounding: Other possible explanations are controlled

只有通过精心设计的随机对照实验,才能可靠地建立因果关系。观察性研究无论数据多大,只能展示关联,不能证明因果。

Only through carefully designed randomized controlled experiments can causation be reliably established. Observational studies, no matter how large the data, can only show association and cannot prove causation.

1.3.2 混淆变量 (Confounding Variables)

混淆变量是与解释变量和响应变量都相关,但未被研究考虑的变量。

A confounding variable is a variable that is related to both the explanatory variable and the response variable but is not accounted for in the study.

1.3.2.1 金融案例:低市盈率与高收益 (Financial Case: Low P/E Ratio and High Returns)

观察:研究发现购买低市盈率(PE)股票的投资者往往获得更高收益。

Observation: Research finds that investors who buy low P/E ratio stocks tend to earn higher returns.

错误结论:低市盈率直接导致高收益。

Incorrect conclusion: Low P/E ratio directly causes high returns.

真实原因:低市盈率往往出现在行业景气度处于底部的公司。当行业周期反转时,盈利快速恢复推动了股价上涨。行业周期反转才是真正的因果因素,低市盈率只是行业低谷期的一种表征。

Real reason: Low P/E ratios often appear in companies whose industries are at the bottom of the business cycle. When the industry cycle reverses, rapid earnings recovery drives stock price increases. Industry cycle reversal is the true causal factor; low P/E is merely a symptom of the industry trough.

1.3.2.2 商业案例:周末购物与消费金额 (Business Case: Weekend Shopping vs. Spending Amount)

观察:周末购物的人均消费比工作日高20%。

Observation: Per capita spending on weekends is 20% higher than on weekdays.

错误结论:周末导致消费增加。

Incorrect conclusion: Weekends cause increased spending.

真实原因:周末购物者更多是全职工作者(收入更高),而工作日购物者更多是退休人员或学生。就业状态和收入是混淆变量。

Real reason: Weekend shoppers are more likely to be full-time workers (higher income), while weekday shoppers are more likely to be retirees or students. Employment status and income are confounding variables.

解决方法 (Solutions):

分层分析:分别比较全职工作者的周末vs工作日消费

多元回归:控制收入、就业状态等变量

Stratified analysis: Compare full-time workers’ weekend vs. weekday spending separately

Multiple regression: Control for income, employment status, and other variables

1.4 数据收集方法 (Data Collection Methods)

数据收集是统计分析的第一步。数据的质量直接决定了分析结果的可靠性。如果数据收集过程有偏差,再精妙的统计方法也无法得出正确结论。

Data collection is the first step of statistical analysis. The quality of data directly determines the reliability of analytical results. If the data collection process is biased, even the most sophisticated statistical methods cannot yield correct conclusions.

1.4.1 观察性研究与实验研究 (Observational Studies vs. Experimental Studies)

观察性研究(Observational Study)只是观察和记录对象的特征,不对研究对象进行干预。

An Observational Study merely observes and records the characteristics of subjects without intervening.

常见类型:

Common types:

横截面研究(Cross-sectional):在一个时间点上观察(如2023年A股上市公司的财务快照)

回顾性研究(Retrospective):回溯过去的数据(如分析2008-2023年金融危机的影响)

前瞻性研究(Prospective):跟踪一段时间(如跟踪新上市公司3年)

Cross-sectional study: Observing at a single point in time (e.g., a financial snapshot of A-share listed companies in 2023)

Retrospective study: Looking back at historical data (e.g., analyzing the impact of financial crises from 2008-2023)

Prospective study: Tracking over a period of time (e.g., following newly listed companies for 3 years)

实验研究(Experimental Study)通过主动干预来研究因果关系。

An Experimental Study investigates causal relationships through active intervention.

关键要素:

Key elements:

处理/干预(Treatment):对实验组施加的条件

对照/控制(Control):对照组不施加处理

随机化(Randomization):随机分配对象到实验组和对照组

Treatment/Intervention: The condition applied to the experimental group

Control: The control group does not receive the treatment

Randomization: Randomly assigning subjects to experimental and control groups

1.4.1.1 量化投资实验设计 (Quantitative Investment Experiment Design)

假设某基金公司想验证新开发的量化投资因子是否真的有效:

Suppose a fund company wants to verify whether a newly developed quantitative investment factor is truly effective:

研究问题:新因子模型能否提高投资组合的超额收益?

Research question: Can the new factor model improve portfolio excess returns?

实验设计:

Experiment design:

样本量:随机选取3000只A股股票

随机分配:

- 处理组:1500只股票按新因子信号构建组合

- 对照组:1500只股票按传统因子信号构建组合

双盲设计:基金经理和分析师在评估期内不知道哪组使用了新因子

主要终点:比较两组的超额收益率、夏普比率

Sample size: Randomly select 3,000 A-share stocks

Random assignment:

- Treatment group: 1,500 stocks form a portfolio based on the new factor signals

- Control group: 1,500 stocks form a portfolio based on traditional factor signals

Double-blind design: Fund managers and analysts do not know which group uses the new factor during evaluation

Primary endpoint: Compare excess returns and Sharpe ratios between the two groups

为什么需要随机化?

Why is randomization necessary?

如果不随机分配,可能出现系统偏差:

Without random assignment, systematic bias may occur:

研究人员倾向于将新因子应用于历史表现好的股票

这些股票本身就有更高的收益

无法判断是新因子有效,还是选股池本身的差异

Researchers tend to apply the new factor to stocks with good historical performance

These stocks inherently have higher returns

It becomes impossible to determine whether the new factor is effective or whether the stock pool itself differs

随机化的作用:平衡两组的已知和未知因素,确保只有”是否使用新因子”这一变量不同。

The role of randomization: Balance known and unknown factors between the two groups, ensuring that the only difference is “whether the new factor is used.”

1.4.1.2 随机区组设计 (Randomized Block Design)

当存在已知的影响因素但不是研究重点时,可以使用随机区组设计。

When there are known influencing factors that are not the focus of the study, a Randomized Block Design can be used.

中国金融案例:交易员培训方案实验

Chinese financial case: Trader training program experiment

研究问题:比较两种新的交易员培训方案(A方案:实盘模拟训练;B方案:理论案例教学)对交易绩效的影响

Research question: Compare the effects of two new trader training programs (Plan A: Live simulation training; Plan B: Theoretical case teaching) on trading performance

挑战:交易员的初始经验水平差异很大,会影响结果

Challenge: Traders’ initial experience levels vary significantly, which affects the results

解决方案:

Solution:

将交易员按从业年限分为三个区组(blocks):

- 资深交易员区组(10年以上)

- 中级交易员区组(3-10年)

- 初级交易员区组(3年以下)

在每个区组内随机分配交易员到方案A和方案B

确保每个培训方案组都有相同数量的各经验层级交易员

Divide traders into three blocks by years of experience:

- Senior trader block (10+ years)

- Intermediate trader block (3-10 years)

- Junior trader block (under 3 years)

Randomly assign traders within each block to Plan A and Plan B

Ensure each training program group has equal numbers of traders from each experience level

优势:

Advantages:

控制了初始经验水平的影响

提高了实验的统计功效(statistical power)

可以检验培训方案是否对不同经验层级的交易员有不同效果(交互效应)

Controls the effect of initial experience level

Improves the statistical power of the experiment

Can test whether the training program has different effects on traders at different experience levels (interaction effect)

1.5 抽样方法 (Sampling Methods)

1.5.1 总体、样本与统计推断 (Population, Sample, and Statistical Inference)

在统计学中:

In statistics:

总体(Population):研究对象的全体

样本(Sample):从总体中抽取的、用于研究的较小子集

参数(Parameter):总体特征,用希腊字母表示(如总体均值\(\mu\))

统计量(Statistic):样本特征,用普通字母表示(如样本均值\(\bar{x}\))

Population: The entire group of subjects under study

Sample: A smaller subset drawn from the population for study

Parameter: A population characteristic, denoted by Greek letters (e.g., population mean \(\mu\))

Statistic: A sample characteristic, denoted by ordinary letters (e.g., sample mean \(\bar{x}\))

案例:

Example:

总体:所有中国A股上市公司(约5000家)

样本:被抽取研究的100家公司

参数:所有公司的平均市盈率(P/E ratio)

统计量:这100家公司的平均市盈率

Population: All Chinese A-share listed companies (approximately 5,000)

Sample: 100 companies selected for study

Parameter: The average P/E ratio of all companies

Statistic: The average P/E ratio of these 100 companies

1.5.1.1 为什么需要抽样? (Why Is Sampling Necessary?)

进行全面调查(普查)往往不现实:

Conducting a complete census is often impractical:

- 成本太高:调查全部5000家上市公司需要巨大人力物力

- 时间太长:等到调查完成,情况可能已经变化

- 破坏性测试:某些测试是破坏性的,不能对全部对象进行

- 案例:测试灯泡寿命,必须用到灯泡烧毁

- 不能测试所有灯泡,否则就没有产品可卖了

- Too costly: Surveying all 5,000 listed companies requires enormous human and material resources

- Too time-consuming: By the time the survey is complete, conditions may have changed

- Destructive testing: Some tests are destructive and cannot be performed on all subjects

- Example: Testing light bulb lifespan requires burning them out

- You cannot test all light bulbs, otherwise there would be none left to sell

1.5.1.2 统计推断的核心思想 (The Core Idea of Statistical Inference)

关键问题:如何从100家样本公司的市盈率,推断全部5000家公司的市盈率?

Key question: How can we infer the P/E ratio of all 5,000 companies from the P/E ratio of 100 sample companies?

统计推断的答案:

The answer from statistical inference:

样本是总体的代表(如果抽样得当)

样本统计量是总体参数的估计

通过置信区间(confidence interval)量化估计的不确定性

通过假设检验(hypothesis testing)判断结论的可靠性

The sample represents the population (if properly sampled)

Sample statistics are estimates of population parameters

Confidence intervals quantify the uncertainty of estimates

Hypothesis testing assesses the reliability of conclusions

我们将在第5章详细学习这些方法。

We will study these methods in detail in Chapter 5.

1.5.2 简单随机抽样 (Simple Random Sampling)

定义:每个个体被抽中的概率相等,且每个可能的样本被抽中的概率也相等。

Definition: Every individual has an equal probability of being selected, and every possible sample has an equal probability of being selected.

案例:中国消费者信心调查

Example: Chinese Consumer Confidence Survey

假设要从上海2000万成年人中抽取1500人进行消费者信心调查:

Suppose we want to sample 1,500 people from Shanghai’s 20 million adults for a consumer confidence survey:

实施方法:

Implementation method:

获得上海所有成年人的抽样框

使用计算机随机数生成器

随机抽取1500人

确保每个人被抽中的概率相等

Obtain a sampling frame of all adults in Shanghai

Use a computer random number generator

Randomly select 1,500 people

Ensure each person has an equal probability of being selected

挑战:

Challenges:

抽样框不完整:某些人群可能不在抽样框中(如无固定电话者)

无响应偏差:被抽中的人可能拒绝参与调查

Incomplete sampling frame: Some groups may not be in the sampling frame (e.g., those without landline phones)

Nonresponse bias: Selected individuals may refuse to participate

1.5.3 抽样偏差 (Sampling Bias)

抽样偏差是系统性误差,不同于数据的自然变异,无法通过统计技术修正。

Sampling bias is a systematic error, different from natural data variability, and cannot be corrected by statistical techniques.

1.5.3.1 常见类型 (Common Types)

选择偏差(Selection Bias)

案例:在写字楼里进行的消费调查

Example: Consumer survey conducted in office buildings

问题:会高估收入水平(白领集中)

被抽取的样本不能代表整个人群

Problem: Overestimates income level (concentration of white-collar workers)

The sample drawn cannot represent the entire population

自愿响应偏差(Voluntary Response Bias)

案例:网络投票、微博热搜调查

Example: Online polls, Weibo trending-topic surveys

- 问题:只能吸引持有强烈观点的人参与

- 历史教训:

- 1948年美国总统大选,电话民意测验预测杜威获胜

- 但实际杜鲁门获胜

- 原因:当时只有富裕家庭(支持杜威)有电话

- Problem: Attracts only those with strong opinions

- Historical lesson:

- In the 1948 U.S. presidential election, telephone polls predicted Dewey would win

- But Truman actually won

- Reason: At the time, only wealthy families (who supported Dewey) had telephones

无响应偏差(Nonresponse Bias)

案例:邮寄问卷回收率低

Example: Low return rate for mailed questionnaires

问题:响应者可能与不响应者有系统性差异

比如年轻人更不愿意回复纸质问卷

Problem: Responders may systematically differ from non-responders

For example, young people are less willing to reply to paper questionnaires

幸存者偏差 (Survivorship Bias):二战飞机的启示

(Survivorship Bias: Lessons from World War II Aircraft)

这是统计学历史上最著名的反例之一,由统计学家亚伯拉罕·沃德 (Abraham Wald) 在二战期间提出。

This is one of the most famous counterexamples in the history of statistics, proposed by statistician Abraham Wald during World War II.

现象:返航的战机上,机翼被打得千疮百孔,而驾驶舱和引擎完好无损。

军方直觉:应该加强机翼的装甲,因为那里弹孔最多。

统计学家直觉:错!应该加强驾驶舱和引擎。

Observation: Returning aircraft had wings riddled with bullet holes, while cockpits and engines were intact.

Military intuition: Reinforce the wing armor, because that’s where most bullet holes are.

Statistician’s intuition: Wrong! Reinforce the cockpit and engine.

逻辑:

Logic:

我们只能看到返航的飞机(幸存者)。

那些驾驶舱和引擎中弹的飞机,根本就没能飞回来(被样本剔除了)。

机翼上的弹孔反而证明了:即使机翼中弹,飞机依然能活下来。

We can only see the aircraft that returned (survivors).

Those aircraft hit in the cockpit and engine never made it back (they were excluded from the sample).

Bullet holes in the wings actually prove that: even if the wings are hit, the plane can still survive.

主要启示:数据分析最危险的不是数据里有什么,而是数据里缺了什么。在商业中,我们分析成功的公司(幸存者),试图总结”成功经验”,却往往忽略了那些做了同样事情但破产了的公司。

Key takeaway: The most dangerous thing in data analysis is not what is in the data, but what is missing from the data. In business, we analyze successful companies (survivors) and try to summarize “success factors,” but often overlook companies that did the same things but went bankrupt.

1.5.4 中国民意调查的挑战 (Challenges of Public Opinion Polling in China)

2016年美国总统大选的预测失败是统计学界的经典案例。许多民调机构错误预测希拉里获胜,原因是:

The failure to predict the 2016 U.S. presidential election is a classic case in the statistics community. Many polling organizations incorrectly predicted Hillary Clinton would win, because:

错过了新增的”特朗普选民”

抽样框未能充分覆盖农村地区

响应率低,且特朗普支持者更不愿意参与调查

They missed the new “Trump voters”

The sampling frame failed to adequately cover rural areas

Response rates were low, and Trump supporters were less willing to participate in surveys

中国类似的挑战:

Similar challenges in China:

城乡差异

(Urban-rural divide)

一线城市调查结果不能代表全国

农村地区的消费习惯、价值观与城市差异很大

First-tier city survey results cannot represent the entire country

Rural areas’ consumption habits and values differ greatly from cities

数字鸿沟

(Digital divide)

网络调查会漏掉不使用互联网的群体

老年人、农村居民、低收入者被低估

Online surveys miss groups that do not use the internet

The elderly, rural residents, and low-income individuals are underrepresented

地域文化差异

(Regional cultural differences)

长三角的消费习惯可能与西北地区完全不同

全国性调查需要确保地域代表性

Consumption habits in the Yangtze River Delta may be completely different from the Northwest

National surveys need to ensure regional representativeness

政治敏感性

(Political sensitivity)

某些敏感话题的调查可能得到不真实的回答

社会期望偏差(Social Desirability Bias):受访者按照”社会期望”而非真实想法回答

Surveys on certain sensitive topics may receive untruthful responses

Social Desirability Bias: Respondents answer according to “social expectations” rather than their true thoughts

1.5.5 其他抽样方法 (Other Sampling Methods)

虽然本教材主要使用简单随机抽样,但实践中还有其他专门方法:

Although this textbook primarily uses simple random sampling, there are other specialized methods used in practice:

分层抽样(Stratified Sampling)

先将总体分成若干层(strata)

再从每层随机抽样

案例:按省份分层,确保每个省份都有足够样本

First divide the population into several strata

Then randomly sample from each stratum

Example: Stratify by province to ensure each province has an adequate sample

整群抽样(Cluster Sampling)

将总体分成若干群

随机抽取部分群

调查群内所有个体

案例:随机抽取若干个学校,调查这些学校的所有学生

优势:节省成本,不需要跑遍全国

Divide the population into several clusters

Randomly select some clusters

Survey all individuals within the selected clusters

Example: Randomly select several schools and survey all students in those schools

Advantage: Saves cost, no need to travel nationwide

1.5.6 3. 系统抽样 (Systematic Sampling)

按固定间隔抽取

案例:从生产线上每隔100件产品抽取1件检验

实施简单,但要注意周期性模式

Select at fixed intervals

Example: Inspect 1 product for every 100 on the production line

Simple to implement, but watch out for periodic patterns

1.6 从理论到实践:苦活累活 (From Theory to Practice: The “Dirty Work”)

每一本统计学教科书在介绍方法时,通常都假设数据是完美的:没有缺失值,没有录入错误,样本完美代表总体。然而,现实世界的数据是”脏乱”的。在应用任何统计模型之前,数据科学家往往要花80%的时间进行数据清洗和预处理。

Every statistics textbook, when introducing methods, typically assumes that the data is perfect: no missing values, no entry errors, and samples perfectly represent the population. However, real-world data is “messy.” Before applying any statistical model, data scientists often spend 80% of their time on data cleaning and preprocessing.

1.6.1 数据质量陷阱 (Data Quality Traps)

即使是像上市公司财务报表这样经过审计的数据,也并非完美无缺。

Even audited data such as listed company financial statements is not flawless.

缺失值 (Missing Values): 公司可能因为停牌、推迟披露年报等原因导致数据缺失。

异常值 (Outliers): 录入错误或极端事件(如巨额亏损)会导致某些指标偏离正常范围几个数量级。

幸存者偏差 (Survivorship Bias): 这是金融数据分析中最危险的陷阱。

Missing Values: Companies may have missing data due to trading suspensions, delayed annual reports, etc.

Outliers: Entry errors or extreme events (such as massive losses) can cause certain metrics to deviate several orders of magnitude from normal ranges.

Survivorship Bias: This is the most dangerous trap in financial data analysis.

让我们通过一个实际的 Python 案例来演示什么是幸存者偏差。

Let us demonstrate survivorship bias through a practical Python example.

1.6.2 案例研究:幸存者偏差的验证 (Case Study: Verifying Survivorship Bias)

很多关于”长期投资”的研究会告诉你:如果你在10年前买入A股所有股票并持有至今,平均收益率是多少。但这些研究往往犯了一个致命错误:它们只统计了现在还活着的公司。

Many studies on “long-term investing” will tell you: what would the average return be if you had bought all A-share stocks 10 years ago and held them until now. But these studies often make a fatal error: they only count companies that are still alive today.

事实上,有很多公司在过去10年里因为业绩不佳而退市了。如果我们只分析现在的上市公司,就人为地剔除了那些”失败者”,从而高估了市场的平均表现。

In fact, many companies were delisted over the past 10 years due to poor performance. If we only analyze currently listed companies, we artificially exclude those “losers,” thereby overestimating the market’s average performance.

让我们用本地的 stock_basic 数据来看看,到底有多少公司”消失”了。

Let us use local stock_basic data to see how many companies have “disappeared.”

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import pandas as pd # 数据分析库

# Data analysis library

import platform # 平台检测库

# Platform detection library

# ========== 设置本地数据路径 ==========

# ========== Set local data paths ==========

if platform.system() == 'Windows': # 判断当前操作系统类型

# Check the current operating system type

data_path = 'C:/qiufei/data/stock' # Windows 数据路径

# Data path for Windows

else: # Linux 系统下使用服务器数据路径

# Use server data path on Linux

data_path = '/home/ubuntu/r2_data_mount/qiufei/data/stock' # Linux 数据路径

# Data path for Linux

# ========== 读取并分析数据 ==========

# ========== Load and analyze data ==========

stock_basic_dataframe = pd.read_hdf(f'{data_path}/stock_basic_data.h5') # 读取上市公司基本信息

# Load listed company basic information

# 统计各上市状态的公司数量: Active(上市)、Delisted(退市)、Unknown(暂停上市)

# Count companies by listing status: Active (Listed), Delisted, Unknown (Paused)

listing_status_counts = stock_basic_dataframe['status'].value_counts() # 按上市状态分组计数

# Group and count by listing status

# 将英文状态名替换为中英文对照的标签

# Replace English status names with bilingual labels

status_name_mapping = {'Active': '上市 (Listed)', 'Delisted': '退市 (Delisted)', 'Unknown': '暂停上市 (Paused)'} # 定义英文到中英文对照的映射

# Define mapping from English to bilingual labels

listing_status_counts.index = listing_status_counts.index.map(status_name_mapping) # 应用映射替换索引标签

# Apply mapping to replace index labels