# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import pandas as pd # 导入pandas库,用于数据处理和分析

# Import pandas for data processing and analysis

import numpy as np # 导入numpy库,用于数值计算

# Import numpy for numerical computation

from sklearn.cluster import KMeans # 导入K-Means聚类算法

# Import K-Means clustering algorithm

from sklearn.preprocessing import StandardScaler # 导入标准化工具,消除量纲影响

# Import standardization tool to eliminate scale effects

from sklearn.metrics import silhouette_score # 导入轮廓系数,评估聚类质量

# Import silhouette score to evaluate clustering quality

import matplotlib.pyplot as plt # 导入matplotlib绘图库

# Import matplotlib plotting library

import platform # 导入platform模块,用于检测操作系统

# Import platform module for OS detection

# ========== 中文字体设置 ==========

# ========== Chinese font settings ==========

if platform.system() == 'Linux': # 如果是Linux操作系统

# If running on Linux OS

plt.rcParams['font.sans-serif'] = ['Source Han Serif SC', 'SimHei', 'DejaVu Sans'] # 设置思源宋体等中文字体

# Set Source Han Serif SC and other Chinese fonts

else: # 如果是Windows操作系统

# If running on Windows OS

plt.rcParams['font.sans-serif'] = ['SimHei', 'Microsoft YaHei'] # 设置黑体和微软雅黑

# Set SimHei and Microsoft YaHei fonts

plt.rcParams['axes.unicode_minus'] = False # 解决坐标轴负号显示问题

# Fix the minus sign display issue on axes

# ========== 第1步:加载本地财务数据 ==========

# ========== Step 1: Load local financial data ==========

if platform.system() == 'Linux': # Linux平台数据路径

# Data path for Linux platform

data_path = '/home/ubuntu/r2_data_mount/qiufei/data/stock' # Linux下的数据挂载路径

# Mounted data path on Linux

else: # Windows平台数据路径

# Data path for Windows platform

data_path = 'C:/qiufei/data/stock' # Windows下的本地数据路径

# Local data path on Windows

financial_statement_dataframe = pd.read_hdf(f'{data_path}/financial_statement.h5') # 读取上市公司财务报表数据

# Read listed company financial statement data

stock_basic_info_dataframe = pd.read_hdf(f'{data_path}/stock_basic_data.h5') # 读取股票基本信息数据

# Read stock basic information data

# ========== 第2步:筛选2023年报数据 ==========

# ========== Step 2: Filter 2023 annual report data ==========

annual_report_dataframe_2023 = financial_statement_dataframe[ # 按条件筛选2023年报数据

# Filter 2023 annual report data by conditions

(financial_statement_dataframe['quarter'].str.endswith('q4')) & # 筛选第四季度(年报)

# Select Q4 (annual reports)

(financial_statement_dataframe['quarter'].str.startswith('2023')) # 筛选2023年

# Select year 2023

].copy() # 复制以避免链式赋值警告

# Copy to avoid chained assignment warning13 无监督学习方法 (Unsupervised Learning Methods)

无监督学习(Unsupervised Learning)处理没有标签的数据,目标是发现数据中的内在结构和模式。与监督学习不同,无监督学习没有”正确答案”作为指导,需要算法自行发现数据的规律。本章首先讨论无监督学习的理论基础( 小节 13.2 ),然后介绍K-均值聚类(小节 13.3 )和层次聚类(小节 13.4 ),接着讲解主成分分析(小节 13.5 )及非线性降维方法(小节 13.6 ),最后介绍聚类评估( 小节 13.7 )。

Unsupervised Learning deals with unlabeled data, aiming to discover the inherent structure and patterns within it. Unlike supervised learning, unsupervised learning has no “correct answers” for guidance—algorithms must discover regularities in the data on their own. This chapter first discusses the theoretical foundations of unsupervised learning ( 小节 13.2 ), then introduces K-means clustering ( 小节 13.3 ) and hierarchical clustering ( 小节 13.4 ), followed by principal component analysis ( 小节 13.5 ) and nonlinear dimensionality reduction methods ( 小节 13.6 ), and finally covers clustering evaluation ( 小节 13.7 ).

13.1 无监督学习在金融市场分析中的典型应用 (Typical Applications of Unsupervised Learning in Financial Market Analysis)

在金融市场中,大量数据是无标签的——我们不知道哪些股票”应该”被归为一类,也不知道市场的”真实”结构是什么。无监督学习方法为发现金融数据中隐藏的模式和结构提供了强大工具。

In financial markets, a large volume of data is unlabeled—we do not know which stocks “should” be grouped together, nor do we know what the “true” structure of the market is. Unsupervised learning methods provide powerful tools for discovering hidden patterns and structures in financial data.

13.1.1 应用一:A股市场风格聚类 (Application 1: A-Share Market Style Clustering)

利用 valuation_factors_quarterly_15_years.h5 中的多维估值因子数据,对A股上市公司进行K-means聚类分析,可以发现市场中天然存在的”风格群组”:如大盘价值股、小盘成长股、高股息蓝筹股等。这种数据驱动的分类方式不依赖于人工设定的规则(如简单的市值大小分组),能够揭示出更细微的市场结构。

Using the multidimensional valuation factor data from valuation_factors_quarterly_15_years.h5, K-means clustering analysis on A-share listed companies can reveal naturally occurring “style groups” in the market: such as large-cap value stocks, small-cap growth stocks, and high-dividend blue chips. This data-driven classification approach does not depend on manually set rules (such as simple market-cap grouping) and can uncover more nuanced market structures.

13.1.2 应用二:财务报表异常检测 (Application 2: Financial Statement Anomaly Detection)

主成分分析(PCA)可以将 financial_statement.h5 中数十个财务指标降维到少数几个主成分,捕捉财务数据的主要变异方向。那些在低维空间中远离主体分布的公司,可能存在财务异常或财务造假嫌疑。这一方法已被广泛应用于审计风险评估和监管预警系统中。

Principal Component Analysis (PCA) can reduce dozens of financial indicators in financial_statement.h5 down to a few principal components, capturing the main directions of variation in financial data. Companies that lie far from the main distribution in this low-dimensional space may exhibit financial anomalies or suspected financial fraud. This method has been widely applied in audit risk assessment and regulatory early-warning systems.

13.1.3 应用三:投资组合构建中的降维应用 (Application 3: Dimensionality Reduction in Portfolio Construction)

在构建投资组合时,高维资产之间的相关性矩阵既难以估计又难以解释。PCA可以从大量个股收益率中提取出少数几个”统计因子”,这些因子往往对应市场因子、行业因子、风格因子等经济含义明确的驱动力。基于 stock_price_pre_adjusted.h5 中的日度收益率数据进行PCA分析,可以识别A股市场的主要收益率驱动因子,为风险分解和组合优化提供依据。

When constructing portfolios, the correlation matrix among high-dimensional assets is both difficult to estimate and difficult to interpret. PCA can extract a small number of “statistical factors” from a large set of individual stock returns; these factors often correspond to economically meaningful drivers such as market factors, industry factors, and style factors. Performing PCA on daily return data from stock_price_pre_adjusted.h5 can identify the main return drivers of the A-share market, providing a basis for risk decomposition and portfolio optimization.

13.1.4 聚类与降维的关系 (Relationship Between Clustering and Dimensionality Reduction)

| 类型 | 目标 | 典型方法 | 输出 |

|---|---|---|---|

| 聚类 | 发现相似组 | K-means, 层次聚类, DBSCAN | 类别标签 |

| 降维 | 简化数据 | PCA, t-SNE, UMAP | 低维表示 |

| Type | Objective | Typical Methods | Output |

|---|---|---|---|

| Clustering | Discover similar groups | K-means, Hierarchical, DBSCAN | Category labels |

| Dim. Reduction | Simplify data | PCA, t-SNE, UMAP | Low-dim. representation |

实际中两者常结合使用:先降维再聚类,或用聚类结果验证降维效果。

In practice, the two are often combined: first reduce dimensionality then cluster, or use clustering results to validate the dimensionality reduction outcome.

13.2 从理论到实践:苦活累活 (From Theory to Practice: The “Dirty Work”)

无监督学习因为没有”标准答案”(Ground Truth),是数据分析中最容易造假和自欺欺人的领域。

Because unsupervised learning has no “ground truth,” it is the area in data analysis most susceptible to fabrication and self-deception.

13.2.1 墨迹测试 (The Rorschach Test)

聚类分析就像心理学上的”墨迹测试”:你希望看到什么,你就能在数据里看到什么。

Cluster analysis is like the psychological “Rorschach test”: you see in the data whatever you want to see.

现象:即使你把完全随机的噪声数据扔进 K-means,只要你设定 \(K=3\),它一定会给你吐出 3 个”泾渭分明”的簇。

教训:不要迷信算法输出的标签。必须通过业务逻辑验证(比如:这个簇的用户行为真的有商业意义吗?)和稳定性测试(数据换一半,簇还在吗?)。

Phenomenon: Even if you feed completely random noise into K-means, as long as you set \(K=3\), it will always produce 3 “clearly separated” clusters.

Lesson: Do not blindly trust the labels produced by algorithms. You must validate through business logic (e.g., does the user behavior of this cluster truly have commercial meaning?) and stability tests (if you replace half the data, do the clusters still hold?).

13.2.2 尺度的诅咒 (Scaling Effects)

K-means 极其依赖欧几里得距离。

K-means is extremely dependent on Euclidean distance.

陷阱:如果你的数据包含”年收入”(单位:元,范围 0-100万)和”年龄”(单位:岁,范围 0-100)。

后果:年收入的 1 元差异和年龄的 1 岁差异被赋予了同样的权重!实际上,算法会完全忽略年龄,只根据收入聚类。

规则:做聚类前,必须标准化 (Standardization)(均值0,方差1)。没有例外。

Trap: If your data contains “annual income” (unit: yuan, range 0–1,000,000) and “age” (unit: years, range 0–100).

Consequence: A 1-yuan difference in income and a 1-year difference in age are given equal weight! In practice, the algorithm will completely ignore age and cluster solely based on income.

Rule: Before clustering, you must standardize (mean 0, variance 1). No exceptions.

13.3 K-均值聚类 (K-Means Clustering)

13.3.1 算法原理 (Algorithm Principles)

K-means是最经典的聚类算法,由MacQueen于1967年正式命名。其目标是将\(n\)个数据点划分为\(K\)个簇,使各簇内部的方差(平方距离和)最小,如 式 13.1 所示:

K-means is the most classic clustering algorithm, formally named by MacQueen in 1967. Its goal is to partition \(n\) data points into \(K\) clusters such that the within-cluster variance (sum of squared distances) is minimized, as shown in 式 13.1:

\[ \min_{C_1,...,C_K} \sum_{k=1}^K \sum_{x_i \in C_k} \|x_i - \mu_k\|^2 \tag{13.1}\]

其中\(\mu_k = \frac{1}{|C_k|}\sum_{x_i \in C_k} x_i\)是簇\(C_k\)的质心。

where \(\mu_k = \frac{1}{|C_k|}\sum_{x_i \in C_k} x_i\) is the centroid of cluster \(C_k\).

Lloyd算法(标准K-means):

Lloyd’s Algorithm (Standard K-means):

初始化: 随机选择\(K\)个点作为初始质心\(\mu_1^{(0)}, ..., \mu_K^{(0)}\)

分配步骤: 将每个点分配到最近的质心 \[ C_k^{(t)} = \{x_i : \|x_i - \mu_k^{(t)}\| \leq \|x_i - \mu_j^{(t)}\|, \forall j\} \]

更新步骤: 重新计算每个簇的质心 \[ \mu_k^{(t+1)} = \frac{1}{|C_k^{(t)}|}\sum_{x_i \in C_k^{(t)}} x_i \]

重复步骤2-3直到收敛(簇分配不再变化)

Initialization: Randomly select \(K\) points as initial centroids \(\mu_1^{(0)}, ..., \mu_K^{(0)}\)

Assignment step: Assign each point to the nearest centroid \[ C_k^{(t)} = \{x_i : \|x_i - \mu_k^{(t)}\| \leq \|x_i - \mu_j^{(t)}\|, \forall j\} \]

Update step: Recompute the centroid of each cluster \[ \mu_k^{(t+1)} = \frac{1}{|C_k^{(t)}|}\sum_{x_i \in C_k^{(t)}} x_i \]

Repeat steps 2–3 until convergence (cluster assignments no longer change)

K-means收敛性定理

K-means Convergence Theorem

定理: Lloyd算法必定在有限步内收敛。

Theorem: Lloyd’s algorithm is guaranteed to converge in a finite number of steps.

证明思路:

Proof sketch:

每次分配步骤,目标函数不会增加(每点分配到最近质心)

每次更新步骤,目标函数不会增加(质心是簇内均值)

目标函数有下界(≥0)且严格单调不增

簇分配的可能组合有限(\(K^n\)种)

因此算法必定在有限步内收敛

At each assignment step, the objective function does not increase (each point is assigned to the nearest centroid)

At each update step, the objective function does not increase (the centroid is the within-cluster mean)

The objective function has a lower bound (≥0) and is strictly non-increasing

The number of possible cluster assignments is finite (\(K^n\) combinations)

Therefore, the algorithm must converge in a finite number of steps

注意: 收敛点可能是局部最优而非全局最优,因此实际中常多次随机初始化取最优结果。

Note: The convergence point may be a local optimum rather than a global optimum; therefore, in practice, multiple random initializations are used and the best result is selected.

13.3.2 K值选择方法 (Methods for Choosing K)

1. 肘部法则(Elbow Method)

1. Elbow Method

绘制K与簇内平方和(Within-Cluster Sum of Squares, WCSS)的关系图,寻找”肘部”——WCSS下降速度明显放缓的点。

Plot the relationship between K and the Within-Cluster Sum of Squares (WCSS), and look for the “elbow”—the point where the rate of WCSS decrease noticeably slows down.

2. 轮廓系数(Silhouette Score)

2. Silhouette Score

对于每个样本\(i\),轮廓系数的计算如 式 13.2 所示:

For each sample \(i\), the silhouette coefficient is calculated as shown in 式 13.2:

\[ s(i) = \frac{b(i) - a(i)}{\max\{a(i), b(i)\}} \tag{13.2}\]

其中:

where:

\(a(i)\): 样本\(i\)到同簇其他样本的平均距离

\(b(i)\): 样本\(i\)到最近其他簇样本的平均距离

\(a(i)\): the average distance from sample \(i\) to other samples in the same cluster

\(b(i)\): the average distance from sample \(i\) to samples in the nearest other cluster

\(s(i) \in [-1, 1]\),值越大表示聚类效果越好。

\(s(i) \in [-1, 1]\); larger values indicate better clustering quality.

3. Gap统计量

3. Gap Statistic

比较实际数据的WCSS与随机数据的期望WCSS之差。

Compare the difference between the WCSS of the actual data and the expected WCSS of random reference data.

13.3.3 案例:上市公司财务特征聚类 (Case Study: Clustering Listed Companies by Financial Characteristics)

什么是企业画像与客户分群?

What Are Corporate Profiling and Customer Segmentation?

在投资分析和企业管理中,面对数千家上市公司,如何快速识别出财务特征相似的企业群体?传统的行业分类(如证监会行业代码)虽然提供了基本框架,但同一行业内的企业在盈利能力、负债水平、资产规模等方面可能存在巨大差异。K-Means聚类分析提供了一种数据驱动的”企业画像”方法:它根据多维财务指标的相似性,自动将公司划分为若干具有内在一致性的群组。

In investment analysis and corporate management, when facing thousands of listed companies, how can one quickly identify groups of companies with similar financial characteristics? Traditional industry classifications (such as CSRC industry codes) provide a basic framework, but companies within the same industry may exhibit vast differences in profitability, leverage, and asset size. K-Means clustering analysis offers a data-driven “corporate profiling” approach: it automatically divides companies into several internally consistent groups based on the similarity of multidimensional financial indicators.

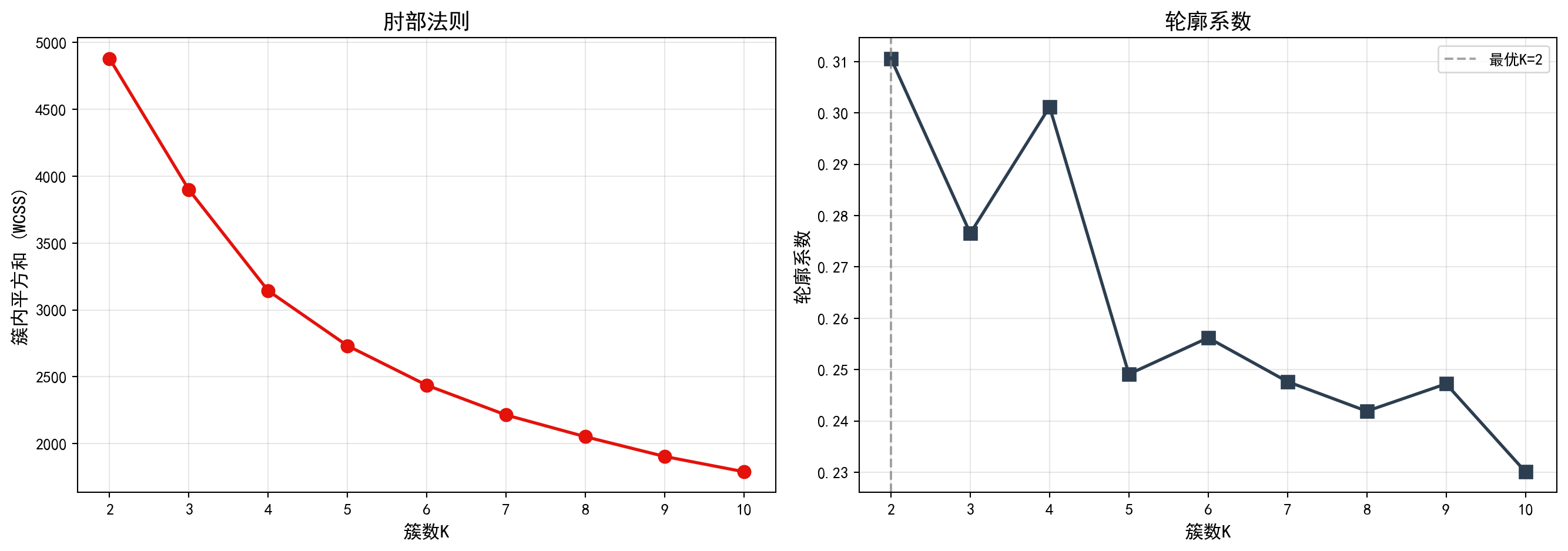

这种无监督学习方法在金融实践中有广泛应用:基金经理可以据此构建同质化的股票池、银行可以识别不同风险等级的客户群体、咨询公司可以对标杆企业进行分类对标分析。下面我们使用长三角地区上市公司的财务数据,进行K-Means聚类分析。图 13.1 展示了肘部法则和轮廓系数对最优K值的评估结果。

This unsupervised learning method has broad applications in financial practice: fund managers can use it to construct homogeneous stock pools, banks can identify customer groups at different risk levels, and consulting firms can perform benchmarking analysis on peer companies. Below, we use financial data from listed companies in the Yangtze River Delta region to perform K-Means clustering analysis. 图 13.1 presents the evaluation results of the elbow method and silhouette score for determining the optimal K.

2023年报数据筛选完成。下面合并公司基本信息,筛选长三角非金融企业并计算关键财务指标。

Filtering of 2023 annual report data is complete. Next, we merge company basic information, filter for non-financial enterprises in the Yangtze River Delta, and compute key financial indicators.

# ========== 第3步:合并基本信息并筛选长三角非金融企业 ==========

# ========== Step 3: Merge basic info and filter YRD non-financial firms ==========

annual_report_dataframe_2023 = annual_report_dataframe_2023.merge( # 左连接合并股票基本信息

# Left join to merge stock basic information

stock_basic_info_dataframe[['order_book_id', 'abbrev_symbol', 'industry_name', 'province']], # 合并公司简称、行业、省份

# Merge company abbreviation, industry, and province

on='order_book_id', how='left' # 以股票代码为键进行左连接

# Left join on stock code

) # 完成基本信息合并操作

# Complete basic information merge

yangtze_river_delta_areas_list = ['上海市', '江苏省', '浙江省', '安徽省'] # 长三角地区省市列表

# List of YRD provinces/municipalities

financial_industries_list = ['货币金融服务', '保险业', '其他金融业'] # 需排除的金融行业列表

# List of financial industries to exclude

clustering_analysis_dataframe = annual_report_dataframe_2023[ # 多条件筛选目标企业样本

# Filter target company samples by multiple conditions

(annual_report_dataframe_2023['province'].isin(yangtze_river_delta_areas_list)) & # 仅保留长三角地区企业

# Keep only YRD region companies

(~annual_report_dataframe_2023['industry_name'].isin(financial_industries_list)) & # 排除金融行业企业

# Exclude financial industry companies

(annual_report_dataframe_2023['total_assets'] > 0) & # 总资产需大于0

# Total assets must be positive

(annual_report_dataframe_2023['total_equity'] > 0) # 所有者权益需大于0

# Total equity must be positive

].copy() # 复制筛选结果

# Copy filtered results

# ========== 第4步:计算关键财务指标 ==========

# ========== Step 4: Compute key financial indicators ==========

clustering_analysis_dataframe['roa'] = clustering_analysis_dataframe['net_profit'] / clustering_analysis_dataframe['total_assets'] * 100 # 计算总资产收益率(ROA),百分比

# Calculate Return on Assets (ROA), in percentage

clustering_analysis_dataframe['debt_ratio'] = clustering_analysis_dataframe['total_liabilities'] / clustering_analysis_dataframe['total_assets'] * 100 # 计算资产负债率,百分比

# Calculate debt-to-asset ratio, in percentage

clustering_analysis_dataframe['current_ratio'] = np.where( # 条件计算流动比率

# Conditionally calculate current ratio

clustering_analysis_dataframe['current_liabilities'] > 0, # 如果流动负债大于0

# If current liabilities are positive

clustering_analysis_dataframe['current_assets'] / clustering_analysis_dataframe['current_liabilities'], # 计算流动比率 = 流动资产/流动负债

# Calculate current ratio = current assets / current liabilities

np.nan # 否则设为缺失值

# Otherwise set to NaN

) # 完成流动比率的条件计算

# Complete conditional calculation of current ratio

clustering_analysis_dataframe['log_assets'] = np.log(clustering_analysis_dataframe['total_assets'] / 1e8) # 对总资产取对数(以亿元为单位),消除规模差异

# Log-transform total assets (in 100-million yuan) to eliminate scale differences关键财务指标计算完毕。下面选择聚类分析特征并过滤极端异常值。

Key financial indicator computation is complete. Next, we select clustering features and filter extreme outliers.

# ========== 第5步:选择聚类特征并过滤异常值 ==========

# ========== Step 5: Select clustering features and filter outliers ==========

selected_clustering_features_list = ['roa', 'debt_ratio', 'current_ratio', 'log_assets'] # 定义用于聚类的四个财务特征

# Define four financial features for clustering

features_for_clustering_dataframe = clustering_analysis_dataframe[selected_clustering_features_list].dropna() # 删除含缺失值的样本

# Drop samples with missing values

features_for_clustering_dataframe = features_for_clustering_dataframe[ # 过滤各指标的极端异常值

# Filter extreme outliers for each indicator

(features_for_clustering_dataframe['roa'] > -50) & (features_for_clustering_dataframe['roa'] < 30) & # 过滤ROA极端值

# Filter extreme ROA values

(features_for_clustering_dataframe['debt_ratio'] > 0) & (features_for_clustering_dataframe['debt_ratio'] < 100) & # 过滤资产负债率极端值

# Filter extreme debt ratio values

(features_for_clustering_dataframe['current_ratio'] > 0) & (features_for_clustering_dataframe['current_ratio'] < 10) # 过滤流动比率极端值

# Filter extreme current ratio values

] # 完成异常值过滤,保留合理范围内的样本

# Complete outlier filtering, keeping samples within reasonable range

print(f'聚类样本量: {len(features_for_clustering_dataframe)}') # 输出有效样本数量

# Print the number of valid samples聚类样本量: 1856经过上述数据预处理流程——剔除金融行业公司、排除总资产或所有者权益为非正值的异常记录、过滤ROA、资产负债率和流动比率的极端异常值后,最终保留了1856家长三角地区非金融上市公司作为本次聚类分析的有效样本。该样本量充分覆盖了长三角地区主要上市企业,能够为聚类分析提供稳健的统计基础。

After the above data preprocessing pipeline—removing financial industry companies, excluding records with non-positive total assets or equity, and filtering extreme outliers in ROA, debt ratio, and current ratio—1,856 non-financial listed companies in the Yangtze River Delta region were retained as valid samples for this clustering analysis. This sample size sufficiently covers the major listed enterprises in the YRD region and provides a robust statistical foundation for clustering analysis.

下面对标准化后的财务指标进行K-Means聚类分析。通过肘部法则和轮廓系数两种方法确定最优簇数K,并以可视化方式展示评估结果。

Next, we perform K-Means clustering analysis on the standardized financial indicators. We determine the optimal number of clusters K using both the elbow method and the silhouette score, and display the evaluation results visually.

# ========== 第6步:特征标准化 ==========

# ========== Step 6: Feature standardization ==========

features_standard_scaler = StandardScaler() # 创建标准化器(均值0、标准差1)

# Create a standardizer (mean=0, std=1)

scaled_features_matrix = features_standard_scaler.fit_transform(features_for_clustering_dataframe) # 对特征矩阵进行标准化变换

# Standardize the feature matrix

# ========== 第7步:使用肘部法则和轮廓系数确定最优K值 ==========

# ========== Step 7: Determine optimal K using elbow method and silhouette score ==========

candidate_k_values_range = range(2, 11) # 候选簇数K从2到10

# Candidate cluster numbers K from 2 to 10

within_cluster_sum_of_squares_list = [] # 存储各K值对应的簇内平方和(WCSS)

# Store WCSS for each K value

calculated_silhouette_scores_list = [] # 存储各K值对应的轮廓系数

# Store silhouette scores for each K value

for k in candidate_k_values_range: # 遍历每个候选K值

# Iterate over each candidate K value

kmeans_clustering_model = KMeans(n_clusters=k, random_state=42, n_init=10) # 创建K-Means模型

# Create a K-Means model

kmeans_clustering_model.fit(scaled_features_matrix) # 在标准化数据上拟合模型

# Fit the model on standardized data

within_cluster_sum_of_squares_list.append(kmeans_clustering_model.inertia_) # 记录簇内平方和

# Record within-cluster sum of squares

calculated_silhouette_scores_list.append(silhouette_score(scaled_features_matrix, kmeans_clustering_model.labels_)) # 记录轮廓系数

# Record silhouette score特征标准化和肘部法则/轮廓系数计算完毕。下面绘制K值选择评估图。

Feature standardization and elbow method / silhouette score computation are complete. Next, we plot the K-value selection evaluation chart.

# ========== 第8步:可视化K值选择结果(双图) ==========

# ========== Step 8: Visualize K-value selection results (dual panel) ==========

evaluation_metrics_figure, evaluation_metrics_axes = plt.subplots(1, 2, figsize=(14, 5)) # 创建1行2列子图

# Create a 1-row, 2-column subplot layout

# --- 左图:肘部法则 ---

# --- Left panel: Elbow Method ---

elbow_method_axes = evaluation_metrics_axes[0] # 获取左侧子图

# Get the left subplot

elbow_method_axes.plot(candidate_k_values_range, within_cluster_sum_of_squares_list, 'o-', color='#E3120B', linewidth=2, markersize=8) # 绘制WCSS随K变化曲线

# Plot WCSS vs. K curve

elbow_method_axes.set_xlabel('簇数K', fontsize=12) # 设置x轴标签

# Set x-axis label

elbow_method_axes.set_ylabel('簇内平方和 (WCSS)', fontsize=12) # 设置y轴标签

# Set y-axis label

elbow_method_axes.set_title('肘部法则', fontsize=14) # 设置子图标题

# Set subplot title

elbow_method_axes.grid(True, alpha=0.3) # 添加半透明网格线

# Add semi-transparent grid lines

# --- 右图:轮廓系数 ---

# --- Right panel: Silhouette Score ---

silhouette_score_axes = evaluation_metrics_axes[1] # 获取右侧子图

# Get the right subplot

silhouette_score_axes.plot(candidate_k_values_range, calculated_silhouette_scores_list, 's-', color='#2C3E50', linewidth=2, markersize=8) # 绘制轮廓系数随K变化曲线

# Plot silhouette score vs. K curve

silhouette_score_axes.set_xlabel('簇数K', fontsize=12) # 设置x轴标签

# Set x-axis label

silhouette_score_axes.set_ylabel('轮廓系数', fontsize=12) # 设置y轴标签

# Set y-axis label

silhouette_score_axes.set_title('轮廓系数', fontsize=14) # 设置子图标题

# Set subplot title

silhouette_score_axes.grid(True, alpha=0.3) # 添加半透明网格线

# Add semi-transparent grid lines

optimal_number_of_clusters = candidate_k_values_range[np.argmax(calculated_silhouette_scores_list)] # 找到轮廓系数最大的K值

# Find the K value with the highest silhouette score

silhouette_score_axes.axvline(x=optimal_number_of_clusters, color='gray', linestyle='--', alpha=0.7, # 绘制最优K值的垂直虚线

# Draw a vertical dashed line at the optimal K value

label=f'最优K={optimal_number_of_clusters}') # 在图上标注最优K的垂直参考线

# Label the optimal K reference line on the chart

silhouette_score_axes.legend() # 添加图例

# Add legend

plt.tight_layout() # 自动调整子图间距

# Automatically adjust subplot spacing

plt.show() # 显示图表

# Display the chart

图 13.1 的左图(肘部法则)显示,随着簇数K从2增加到10,簇内平方和(WCSS)持续下降,但下降速率在K=3至K=4附近出现明显放缓——形成了所谓的”肘部”拐点,表明K=3或K=4是较合理的簇数选择。右图(轮廓系数)则显示,K=2时轮廓系数达到最高值,随后随着K增大而逐步下降,说明从纯粹的统计指标角度,数据最自然地被分为两组。下面输出最优K值结论。

The left panel (elbow method) of 图 13.1 shows that as K increases from 2 to 10, the WCSS continuously decreases, but the rate of decrease noticeably slows around K=3 to K=4—forming the so-called “elbow” point, indicating that K=3 or K=4 is a reasonable choice for the number of clusters. The right panel (silhouette score) shows that the silhouette score reaches its highest value at K=2 and then gradually decreases as K grows, suggesting that from a purely statistical perspective, the data is most naturally divided into two groups. Below we output the optimal K conclusion.

print(f'根据轮廓系数,最优K = {optimal_number_of_clusters}') # 输出最优K值结论

# Print the optimal K conclusion based on silhouette score根据轮廓系数,最优K = 2运行结果显示,根据轮廓系数准则,统计意义上的最优簇数K=2。然而,在实际业务分析中,将所有上市公司仅分为两组过于粗糙,难以从中挖掘出具有实际管理价值的差异化特征。因此,我们综合考虑肘部法则中K=4附近的拐点信号和产业研究的实际需求,选择K=4进行后续分析——这一选择能够更好地区分出不同财务健康状况的企业群体,为投资决策和产业研究提供更细粒度的洞察。

The results show that, according to the silhouette score criterion, the statistically optimal number of clusters is K=2. However, in practical business analysis, dividing all listed companies into only two groups is too coarse to extract differentiated characteristics with real managerial value. Therefore, considering both the elbow signal around K=4 and the practical needs of industry research, we choose K=4 for subsequent analysis—this choice better distinguishes enterprise groups with different financial health profiles and provides finer-grained insights for investment decisions and industry research.

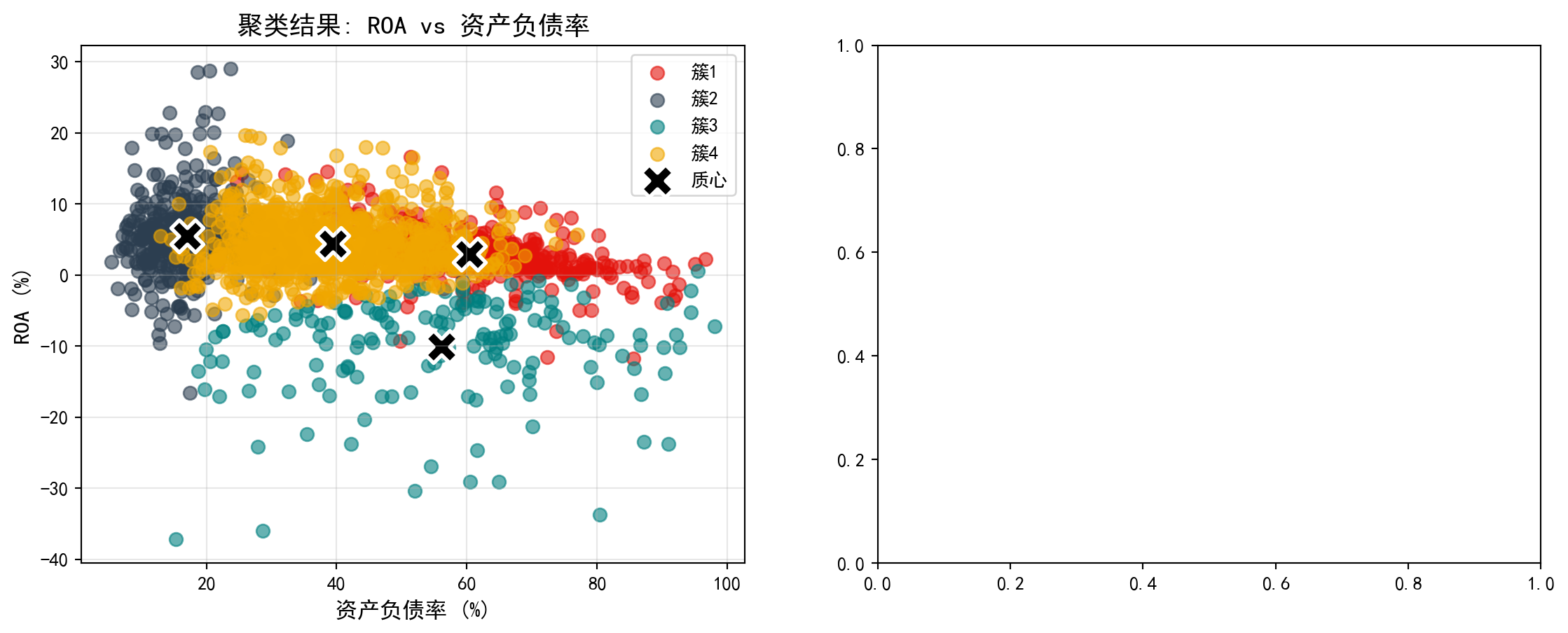

确定K=4后,我们对聚类结果进行详细分析。图 13.2 展示了各簇的财务特征概况,图 13.3 则通过散点图和雷达图直观展示聚类差异。

After determining K=4, we conduct a detailed analysis of the clustering results. 图 13.2 presents an overview of the financial characteristics of each cluster, while 图 13.3 intuitively displays clustering differences through scatter plots and radar charts.

# ========== 第1步:使用指定簇数进行K-Means聚类 ==========

# ========== Step 1: Perform K-Means clustering with the chosen number of clusters ==========

chosen_number_of_clusters = 4 # 根据业务理解选择4簇(对应不同财务特征的企业群体)

# Choose 4 clusters based on business understanding (corresponding to different financial profile groups)

final_kmeans_clustering_model = KMeans(n_clusters=chosen_number_of_clusters, random_state=42, n_init=10) # 创建K-Means模型

# Create the K-Means model

features_for_clustering_dataframe['cluster'] = final_kmeans_clustering_model.fit_predict(scaled_features_matrix) # 拟合并预测簇标签

# Fit the model and predict cluster labels

# ========== 第2步:统计各簇财务特征概况 ==========

# ========== Step 2: Compute summary statistics for each cluster ==========

print(f'=== 使用K={chosen_number_of_clusters}的聚类结果 ===\n') # 输出标题

# Print the header

cluster_characteristics_summary_dataframe = features_for_clustering_dataframe.groupby('cluster').agg({ # 按簇分组聚合

# Group by cluster and aggregate

'roa': ['mean', 'std', 'count'], # 计算ROA的均值、标准差、样本数

# Compute mean, std, and count for ROA

'debt_ratio': 'mean', # 计算资产负债率均值

# Compute mean debt ratio

'current_ratio': 'mean', # 计算流动比率均值

# Compute mean current ratio

'log_assets': 'mean' # 计算对数资产规模均值

# Compute mean log assets

}).round(3) # 四舍五入保留三位小数

# Round to 3 decimal places

print(cluster_characteristics_summary_dataframe) # 输出聚合统计表

# Print the aggregated summary table

# ========== 第3步:解读各簇的财务特征含义 ==========

# ========== Step 3: Interpret the financial characteristics of each cluster ==========

print('\n=== 聚类特征解释 ===') # 输出解释标题

# Print the interpretation header

for cluster_index in range(chosen_number_of_clusters): # 遍历每个簇

# Iterate over each cluster

current_cluster_mean_series = features_for_clustering_dataframe[features_for_clustering_dataframe['cluster'] == cluster_index][selected_clustering_features_list].mean() # 计算当前簇的特征均值

# Compute the feature means for the current cluster

print(f'\n簇{cluster_index+1} (n={sum(features_for_clustering_dataframe["cluster"]==cluster_index)}):') # 输出簇编号和样本量

# Print cluster number and sample size

print(f' ROA: {current_cluster_mean_series["roa"]:.2f}%') # 输出平均总资产收益率

# Print average ROA

print(f' 资产负债率: {current_cluster_mean_series["debt_ratio"]:.1f}%') # 输出平均资产负债率

# Print average debt-to-asset ratio

print(f' 流动比率: {current_cluster_mean_series["current_ratio"]:.2f}') # 输出平均流动比率

# Print average current ratio

print(f' 资产规模(log): {current_cluster_mean_series["log_assets"]:.2f}') # 输出平均对数资产规模

# Print average log asset size=== 使用K=4的聚类结果 ===

roa debt_ratio current_ratio log_assets

mean std count mean mean mean

cluster

0 2.959 3.579 397 60.400 1.302 5.486

1 5.487 5.456 409 17.036 5.235 3.065

2 -10.042 7.054 161 56.084 1.524 3.174

3 4.364 3.957 889 39.408 1.956 3.458

=== 聚类特征解释 ===

簇1 (n=397):

ROA: 2.96%

资产负债率: 60.4%

流动比率: 1.30

资产规模(log): 5.49

簇2 (n=409):

ROA: 5.49%

资产负债率: 17.0%

流动比率: 5.23

资产规模(log): 3.06

簇3 (n=161):

ROA: -10.04%

资产负债率: 56.1%

流动比率: 1.52

资产规模(log): 3.17

簇4 (n=889):

ROA: 4.36%

资产负债率: 39.4%

流动比率: 1.96

资产规模(log): 3.46上述运行结果揭示了K=4聚类下四种截然不同的企业财务画像:

The above results reveal four distinctly different corporate financial profiles under K=4 clustering:

簇1(n=397,“大型高杠杆稳健企业”):平均ROA为2.96%,盈利能力中等;资产负债率高达60.4%,杠杆水平最高;流动比率仅1.30,短期偿债压力较大;但对数资产规模达5.49,为四组中最大。这类企业以大型国有企业和重资产行业龙头为主,依靠规模优势获取低成本融资。

簇2(n=409,“轻资产高效企业”):平均ROA为5.49%,盈利能力最强;资产负债率仅17.0%,财务极为保守;流动比率高达5.23,现金充裕;对数资产规模3.06,体量较小。典型代表为科技型中小企业和现金流充沛的消费类公司。

簇3(n=161,“财务困境企业”):平均ROA为-10.04%,严重亏损;资产负债率56.1%,债务负担沉重;流动比率1.52,流动性紧张;对数资产规模3.17,体量也较小。这类企业面临较大的经营风险,值得投资者警惕。

簇4(n=889,“中等规模均衡企业”):平均ROA为4.36%,盈利稳定;资产负债率39.4%,杠杆水平适中;流动比率1.96,短期偿债能力良好;对数资产规模3.46。这是数量最多的一组,代表了长三角上市公司的主流财务特征。

Cluster 1 (n=397, “Large High-Leverage Stable Firms”): Average ROA of 2.96%, moderate profitability; debt ratio as high as 60.4%, the highest leverage level; current ratio of only 1.30, indicating considerable short-term debt pressure; but log asset size of 5.49, the largest among the four groups. These are primarily large state-owned enterprises and heavy-asset industry leaders that leverage scale advantages to access low-cost financing.

Cluster 2 (n=409, “Asset-Light High-Efficiency Firms”): Average ROA of 5.49%, the strongest profitability; debt ratio of only 17.0%, extremely conservative finances; current ratio as high as 5.23, indicating abundant cash; log asset size of 3.06, relatively small in scale. Typical representatives are technology-oriented SMEs and cash-rich consumer companies.

Cluster 3 (n=161, “Financially Distressed Firms”): Average ROA of -10.04%, severe losses; debt ratio of 56.1%, heavy debt burden; current ratio of 1.52, tight liquidity; log asset size of 3.17, also relatively small. These firms face significant operational risk and warrant investor caution.

Cluster 4 (n=889, “Medium-Sized Balanced Firms”): Average ROA of 4.36%, stable profitability; debt ratio of 39.4%, moderate leverage; current ratio of 1.96, good short-term solvency; log asset size of 3.46. This is the largest group, representing the mainstream financial profile of YRD listed companies.

下面我们通过可视化图形来更直观地展示聚类结果。左图为散点图,展示各公司在ROA与资产负债率两个维度上的分布及其簇归属;右图为雷达图,展示各簇的多维特征轮廓。首先预计算可视化所需的颜色、质心坐标和雷达图数据:

Below, we use visualizations to more intuitively display the clustering results. The left panel is a scatter plot showing the distribution of each company in the ROA vs. debt ratio dimensions and their cluster assignments; the right panel is a radar chart showing the multidimensional feature profile of each cluster. First, we precompute the colors, centroid coordinates, and radar chart data needed for visualization:

# ========== 预计算:可视化所需的公共数据 ==========

# ========== Precomputation: Common data needed for visualization ==========

cluster_display_colors_list = ['#E3120B', '#2C3E50', '#008080', '#F0A700'] # 定义4个簇的显示颜色

# Define display colors for the 4 clusters

unscaled_cluster_centroids_array = features_standard_scaler.inverse_transform(final_kmeans_clustering_model.cluster_centers_) # 将质心反标准化回原始尺度

# Inverse-transform centroids back to original scale

# --- 雷达图维度与角度 ---

# --- Radar chart dimensions and angles ---

radar_chart_categories_list = ['ROA', '资产负债率', '流动比率', '资产规模'] # 雷达图的四个维度

# Four dimensions for the radar chart

number_of_radar_categories = len(radar_chart_categories_list) # 维度数量

# Number of dimensions

radar_chart_angles_list = [radar_angle_index / float(number_of_radar_categories) * 2 * np.pi for radar_angle_index in range(number_of_radar_categories)] # 计算各维度角度

# Calculate angle for each dimension

radar_chart_angles_list += radar_chart_angles_list[:1] # 闭合雷达图(首尾相连)

# Close the radar chart (connect end to start)

# --- 标准化各簇均值用于雷达图绘制 ---

# --- Normalize cluster means for radar chart plotting ---

cluster_average_profiles_dataframe = features_for_clustering_dataframe.groupby('cluster')[selected_clustering_features_list].mean() # 计算各簇特征均值

# Compute feature means for each cluster

normalized_cluster_profiles_dataframe = (cluster_average_profiles_dataframe - cluster_average_profiles_dataframe.min()) / (cluster_average_profiles_dataframe.max() - cluster_average_profiles_dataframe.min()) # Min-Max标准化到0-1范围

# Min-Max normalize to the 0-1 range预计算完成,下面绘制双面板对比图。首先创建画布并绘制左侧散点图,展示各公司在ROA与资产负债率平面上的分布及其簇归属:

Precomputation complete. Now we plot the dual-panel comparison chart. First, we create the canvas and draw the left-side scatter plot, showing the distribution of companies in the ROA vs. debt ratio plane and their cluster assignments:

# ========== 第1步:创建双图布局并绘制散点图 ==========

# ========== Step 1: Create dual-panel layout and draw scatter plot ==========

cluster_visualization_figure, cluster_visualization_axes = plt.subplots(1, 2, figsize=(14, 5)) # 创建1行2列子图

# Create a 1-row, 2-column subplot layout

# ========== 第2步:左图 — ROA vs 资产负债率散点图 ==========

# ========== Step 2: Left panel — ROA vs. Debt Ratio scatter plot ==========

scatter_plot_axes = cluster_visualization_axes[0] # 获取左侧子图

# Get the left subplot

for cluster_index in range(chosen_number_of_clusters): # 遍历每个簇

# Iterate over each cluster

current_cluster_mask_series = features_for_clustering_dataframe['cluster'] == cluster_index # 创建当前簇的布尔掩码

# Create a boolean mask for the current cluster

scatter_plot_axes.scatter(features_for_clustering_dataframe.loc[current_cluster_mask_series, 'debt_ratio'], # x轴:资产负债率

# x-axis: debt ratio

features_for_clustering_dataframe.loc[current_cluster_mask_series, 'roa'], # y轴:ROA

# y-axis: ROA

c=cluster_display_colors_list[cluster_index], label=f'簇{cluster_index+1}', alpha=0.6, s=50) # 按簇着色

# Color by cluster

scatter_plot_axes.scatter(unscaled_cluster_centroids_array[:, 1], unscaled_cluster_centroids_array[:, 0], # 绘制质心点

# Plot centroid points

c='black', marker='X', s=300, linewidths=2, # 黑色X形标记,突出显示

# Black X markers for emphasis

edgecolors='white', label='质心') # 白色边框增强可见度

# White edge for better visibility

scatter_plot_axes.set_xlabel('资产负债率 (%)', fontsize=12) # 设置x轴标签

# Set x-axis label

scatter_plot_axes.set_ylabel('ROA (%)', fontsize=12) # 设置y轴标签

# Set y-axis label

scatter_plot_axes.set_title('聚类结果: ROA vs 资产负债率', fontsize=14) # 设置标题

# Set title

scatter_plot_axes.legend() # 添加图例

# Add legend

scatter_plot_axes.grid(True, alpha=0.3) # 添加半透明网格线

# Add semi-transparent grid lines

散点图清晰地展示了各企业在盈利能力(ROA)与杠杆水平(资产负债率)两个维度上的聚类归属。下面在右侧补充雷达图,从多维度对比各簇的财务特征差异:

The scatter plot clearly shows the cluster assignments of each company along the profitability (ROA) and leverage (debt ratio) dimensions. Next, we add a radar chart on the right to compare the multidimensional financial characteristic differences across clusters:

# ========== 第3步:右图 — 雷达图对比各簇财务特征 ==========

# ========== Step 3: Right panel — Radar chart comparing financial features across clusters ==========

radar_chart_axes = cluster_visualization_axes[1] # 获取右侧子图

# Get the right subplot

for cluster_index in range(chosen_number_of_clusters): # 遍历每个簇绘制雷达图

# Iterate over each cluster to draw the radar chart

radar_chart_values_list = normalized_cluster_profiles_dataframe.loc[cluster_index].values.tolist() # 获取当前簇的标准化值

# Get the normalized values for the current cluster

radar_chart_values_list += radar_chart_values_list[:1] # 闭合雷达图数据(首尾相连形成封闭多边形)

# Close the radar chart data (connect end to start to form a closed polygon)

radar_chart_axes.plot(radar_chart_angles_list, radar_chart_values_list, 'o-', color=cluster_display_colors_list[cluster_index], linewidth=2, label=f'簇{cluster_index+1}') # 绘制轮廓线

# Plot the profile line

radar_chart_axes.fill(radar_chart_angles_list, radar_chart_values_list, color=cluster_display_colors_list[cluster_index], alpha=0.1) # 填充半透明颜色

# Fill with semi-transparent color

radar_chart_axes.set_xticks(radar_chart_angles_list[:-1]) # 设置角度刻度位置

# Set angular tick positions

radar_chart_axes.set_xticklabels(radar_chart_categories_list, fontsize=11) # 设置维度标签

# Set dimension labels

radar_chart_axes.set_title('各簇特征对比(标准化)', fontsize=14) # 设置雷达图标题

# Set radar chart title

radar_chart_axes.legend(loc='upper right', bbox_to_anchor=(1.1, 1)) # 图例置于右上角

# Place legend at upper right

plt.tight_layout() # 自动调整子图间距

# Automatically adjust subplot spacing

plt.show() # 显示图表

# Display the chart<Figure size 672x480 with 0 Axes>13.4 层次聚类 (Hierarchical Clustering)

13.4.1 算法原理 (Algorithm Principles)

层次聚类构建一棵聚类树(dendrogram),可以是:

Hierarchical clustering builds a dendrogram (clustering tree), which can be constructed in two ways:

1. 凝聚法(Agglomerative):自底向上 - 初始:每个点是一个簇 - 迭代:合并最近的两个簇 - 终止:所有点合并为一个簇

1. Agglomerative: Bottom-up - Initialization: Each point is a cluster - Iteration: Merge the two closest clusters - Termination: All points are merged into one cluster

2. 分裂法(Divisive):自顶向下 - 初始:所有点是一个簇 - 迭代:将一个簇分裂为两个 - 终止:每个点是一个簇

2. Divisive: Top-down - Initialization: All points form one cluster - Iteration: Split one cluster into two - Termination: Each point is a cluster

簇间距离度量(Linkage):

Inter-cluster Distance Measures (Linkage):

| 方法 | 定义 | 特点 |

|---|---|---|

| 单链接(Single) | 最近点距离 | 容易产生链状簇 |

| 全链接(Complete) | 最远点距离 | 产生紧凑簇 |

| 平均链接(Average) | 所有点对平均距离 | 折中 |

| Ward | 合并后方差增量 | 倾向于产生大小相近的簇 |

| Method | Definition | Characteristics |

|---|---|---|

| Single Linkage | Nearest point distance | Tends to produce chain-shaped clusters |

| Complete Linkage | Farthest point distance | Produces compact clusters |

| Average Linkage | Average distance of all point pairs | A compromise |

| Ward | Variance increment after merging | Tends to produce clusters of similar size |

13.4.2 案例:行业层次聚类 (Case Study: Industry Hierarchical Clustering)

什么是层次聚类与产业谱系分析?

What is Hierarchical Clustering and Industrial Phylogenetic Analysis?

与K-Means需要预先指定分群数量不同,层次聚类(Hierarchical Clustering)能够自底向上逐步合并最相似的样本,生成一棵完整的”聚类树状图”(Dendrogram)。这棵树不仅展示了最终的分群结果,更揭示了不同行业或企业之间的”亲缘关系”——哪些行业在财务特征上最为接近,哪些行业之间的差异最大。

Unlike K-Means, which requires pre-specifying the number of clusters, hierarchical clustering progressively merges the most similar samples from the bottom up, generating a complete “dendrogram.” This tree not only shows the final clustering results but also reveals the “phylogenetic relationships” between different industries or firms—which industries are most similar in financial characteristics and which differ the most.

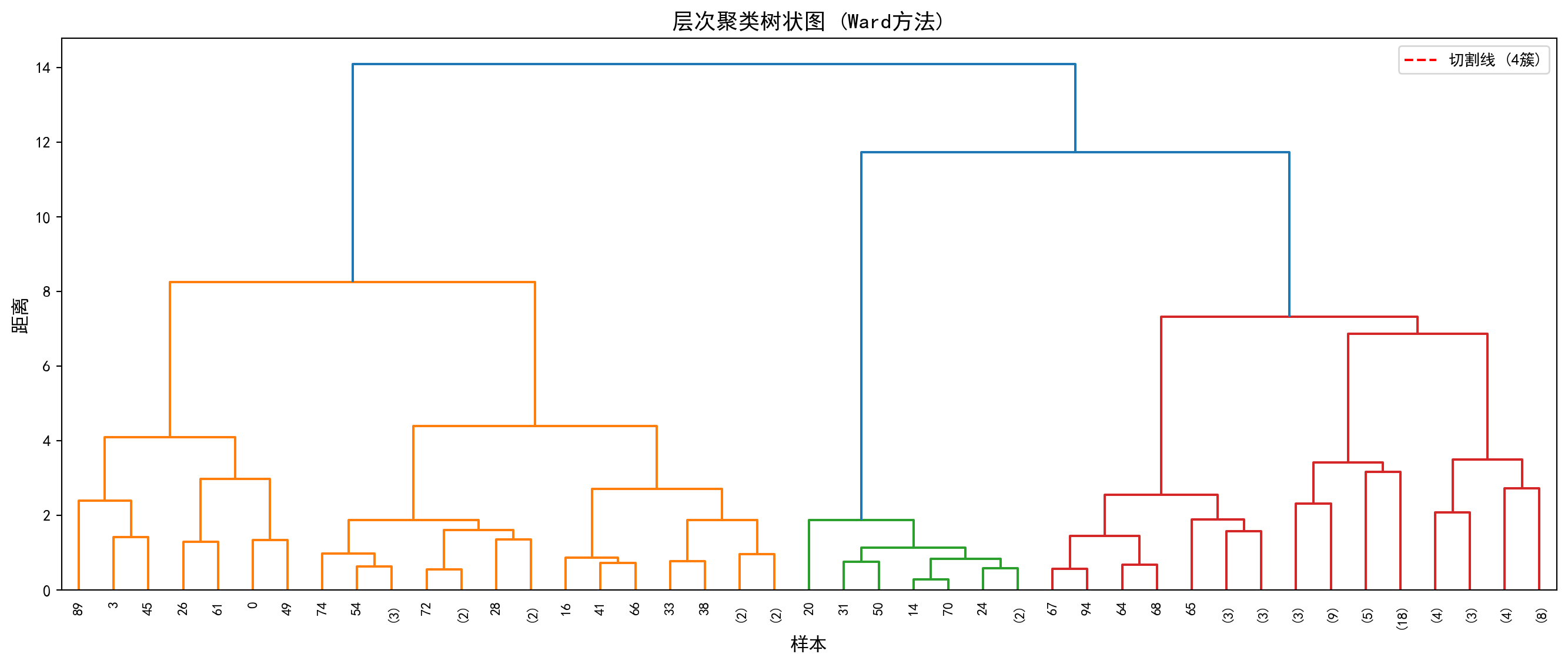

在产业研究中,这种层次化的分类结果尤为有价值:投资者可以据此理解行业板块之间的内在联系,制定跨行业的资产配置策略;产业政策制定者可以识别出具有相似发展特征的行业群体,进行针对性的政策设计。下面我们使用Ward方法对行业数据进行层次聚类分析。图 13.4 展示了树状图结果。

In industrial research, such hierarchical classification results are particularly valuable: investors can use them to understand the intrinsic connections between industry sectors and formulate cross-industry asset allocation strategies; industrial policymakers can identify industry groups with similar development characteristics for targeted policy design. Below, we apply the Ward method to perform hierarchical clustering analysis on industry data. 图 13.4 shows the dendrogram results.

# ========== 导入所需库 ==========

# ========== Import Required Libraries ==========

from scipy.cluster.hierarchy import dendrogram, linkage, fcluster # 导入层次聚类相关函数

# Import hierarchical clustering functions

# ========== 第1步:随机抽样以加速树状图可视化 ==========

# ========== Step 1: Random Sampling to Speed Up Dendrogram Visualization ==========

np.random.seed(42) # 设置随机种子确保可复现

# Set random seed for reproducibility

random_sample_indices_array = np.random.choice(len(scaled_features_matrix), min(100, len(scaled_features_matrix)), replace=False) # 随机抽取100个样本

# Randomly select 100 samples

sampled_scaled_features_matrix = scaled_features_matrix[random_sample_indices_array] # 获取抽样后的标准化特征矩阵

# Obtain the sampled standardized feature matrix

# ========== 第2步:使用Ward方法计算层次聚类连接矩阵 ==========

# ========== Step 2: Compute Hierarchical Clustering Linkage Matrix Using Ward Method ==========

hierarchical_linkage_matrix = linkage(sampled_scaled_features_matrix, method='ward') # Ward方法最小化合并后的方差增量

# Ward method minimizes the variance increment after merging层次聚类连接矩阵计算完毕。下面绘制树状图并按距离阈值切割得到簇标签。

The hierarchical clustering linkage matrix has been computed. Next, we plot the dendrogram and cut it at a distance threshold to obtain cluster labels.

# ========== 第3步:绘制树状图(Dendrogram) ==========

# ========== Step 3: Plot the Dendrogram ==========

dendrogram_figure, dendrogram_axes = plt.subplots(figsize=(14, 6)) # 创建图形画布

# Create figure canvas

dendrogram(hierarchical_linkage_matrix, # 输入连接矩阵

# Input the linkage matrix

truncate_mode='level', # 按层级截断显示

# Truncate display by level

p=5, # 只显示最后5层,避免图形过于密集

# Show only the last 5 levels to avoid visual clutter

leaf_rotation=90, # 叶节点标签旋转90度

# Rotate leaf node labels by 90 degrees

leaf_font_size=9, # 叶节点字体大小

# Set leaf node font size

ax=dendrogram_axes) # 绑定到指定子图

# bindto the specified subplot

dendrogram_axes.set_xlabel('样本', fontsize=12) # 设置x轴标签

# Set x-axis label

dendrogram_axes.set_ylabel('距离', fontsize=12) # 设置y轴标签

# Set y-axis label

dendrogram_axes.set_title('层次聚类树状图 (Ward方法)', fontsize=14) # 设置标题

# Set title

dendrogram_axes.axhline(y=15, color='red', linestyle='--', label='切割线 (4簇)') # 添加水平切割线,表示分为4簇的阈值

# Add horizontal cut line indicating the threshold for 4 clusters

dendrogram_axes.legend() # 添加图例

# Add legend

plt.tight_layout() # 自动调整布局

# Auto-adjust layout

plt.show() # 显示图表

# Display the chart

# ========== 第4步:按距离阈值切割树状图得到簇标签 ==========

# ========== Step 4: Cut the Dendrogram at a Distance Threshold to Obtain Cluster Labels ==========

hierarchical_cluster_labels_array = fcluster(hierarchical_linkage_matrix, t=15, criterion='distance') # 以距离15为阈值切割

# Cut at distance threshold of 15

print(f'层次聚类产生 {len(np.unique(hierarchical_cluster_labels_array))} 个簇') # 输出簇的数量

# Print the number of clusters

print(f'各簇样本数: {np.bincount(hierarchical_cluster_labels_array)}') # 输出每个簇的样本数

# Print the number of samples in each cluster

层次聚类产生 1 个簇

各簇样本数: [ 0 100]运行结果显示,以距离阈值t=15进行切割时,层次聚类仅产生了1个簇,即100个抽样样本全部被归入同一组(各簇样本数为[0, 100],其中索引0处的0是np.bincount对标签值0的计数,实际标签从1开始)。这一结果说明当前的距离阈值设定过高——从 图 13.4 的树状图中可以看到,红色切割线(y=15)位于树状图的顶部,几乎在所有样本合并之后才进行切割,因此无法有效区分出子群。

The results show that when cutting at distance threshold t=15, hierarchical clustering produces only 1 cluster, meaning all 100 sampled observations are grouped together (cluster sizes are [0, 100], where the 0 at index 0 is np.bincount’s count for label value 0, since actual labels start from 1). This result indicates that the current distance threshold is set too high—from the dendrogram in 图 13.4, we can see that the red cut line (y=15) is positioned near the top of the dendrogram, cutting only after almost all samples have been merged, thus failing to effectively distinguish subgroups.

在实际应用中,应根据树状图的形态选择合适的切割高度:观察树状图中较大的”跳跃”(即两个分支合并时距离突然增大的位置),通常是较好的切割点。例如,若将阈值降低至t=5~8的范围,即可获得更有意义的多簇结果。这也体现了层次聚类的一个核心优势——通过树状图可以灵活地在不同粒度上观察聚类结构,而不像K-Means那样必须事先确定簇数。

In practice, one should choose an appropriate cutting height based on the shape of the dendrogram: look for large “jumps” (i.e., positions where the distance suddenly increases when two branches merge), which are typically good cutting points. For example, lowering the threshold to the range of t=5–8 would yield more meaningful multi-cluster results. This also highlights a core advantage of hierarchical clustering—the dendrogram allows flexible observation of clustering structure at different granularities, unlike K-Means which requires pre-specifying the number of clusters.

13.5 主成分分析(PCA) (Principal Component Analysis)

13.5.1 数学原理 (Mathematical Principles)

主成分分析(Principal Component Analysis, PCA)是最经典的降维方法,由Pearson(1901)和Hotelling(1933)发展完善。

Principal Component Analysis (PCA) is the most classic dimensionality reduction method, developed and refined by Pearson (1901) and Hotelling (1933).

目标: 将高维数据投影到低维空间,同时保留最大方差。

Objective: Project high-dimensional data onto a lower-dimensional space while preserving maximum variance.

数学表述: 给定\(n\)个\(p\)维数据点\(X_{n \times p}\)(已中心化),寻找投影方向\(w_1\)使投影后的方差最大,如 式 13.3 所示:

Mathematical Formulation: Given \(n\) data points of \(p\) dimensions \(X_{n \times p}\) (already centered), find the projection direction \(w_1\) that maximizes the projected variance, as shown in 式 13.3:

\[ \max_{w_1} \text{Var}(Xw_1) = w_1' S w_1 \quad \text{s.t.} \quad w_1'w_1 = 1 \tag{13.3}\]

其中\(S = \frac{1}{n-1}X'X\)是样本协方差矩阵。

where \(S = \frac{1}{n-1}X'X\) is the sample covariance matrix.

PCA的特征分解推导(拉格朗日乘子法)

Eigendecomposition Derivation of PCA (Lagrange Multiplier Method)

寻找单位向量 \(\mathbf{w}\),使得投影方差最大。 样本协方差矩阵为 \(\mathbf{S} = \frac{1}{n-1}\mathbf{X}'\mathbf{X}\)。 投影后的方差为 \(\mathbf{w}'\mathbf{S}\mathbf{w}\)。 优化问题: \[ \max_{\mathbf{w}} \mathbf{w}'\mathbf{S}\mathbf{w} \quad \text{s.t.} \quad \mathbf{w}'\mathbf{w} = 1 \] 构造拉格朗日函数: \[ L = \mathbf{w}'\mathbf{S}\mathbf{w} - \lambda(\mathbf{w}'\mathbf{w} - 1) \] 对 \(\mathbf{w}\) 求导并令为0: \[ \frac{\partial L}{\partial \mathbf{w}} = 2\mathbf{S}\mathbf{w} - 2\lambda\mathbf{w} = 0 \Rightarrow \mathbf{S}\mathbf{w} = \lambda\mathbf{w} \] 这正是特征值方程! 且最大方差 \(\mathbf{w}'\mathbf{S}\mathbf{w} = \mathbf{w}'(\lambda\mathbf{w}) = \lambda(\mathbf{w}'\mathbf{w}) = \lambda\)。 结论:第一主成分就是协方差矩阵最大特征值对应的特征向量。

Find the unit vector \(\mathbf{w}\) that maximizes the projected variance. The sample covariance matrix is \(\mathbf{S} = \frac{1}{n-1}\mathbf{X}'\mathbf{X}\). The projected variance is \(\mathbf{w}'\mathbf{S}\mathbf{w}\). The optimization problem: \[ \max_{\mathbf{w}} \mathbf{w}'\mathbf{S}\mathbf{w} \quad \text{s.t.} \quad \mathbf{w}'\mathbf{w} = 1 \] Construct the Lagrangian: \[ L = \mathbf{w}'\mathbf{S}\mathbf{w} - \lambda(\mathbf{w}'\mathbf{w} - 1) \] Differentiate with respect to \(\mathbf{w}\) and set to zero: \[ \frac{\partial L}{\partial \mathbf{w}} = 2\mathbf{S}\mathbf{w} - 2\lambda\mathbf{w} = 0 \Rightarrow \mathbf{S}\mathbf{w} = \lambda\mathbf{w} \] This is precisely the eigenvalue equation! And the maximum variance \(\mathbf{w}'\mathbf{S}\mathbf{w} = \mathbf{w}'(\lambda\mathbf{w}) = \lambda(\mathbf{w}'\mathbf{w}) = \lambda\). Conclusion: The first principal component is the eigenvector corresponding to the largest eigenvalue of the covariance matrix.

几何解释:数据椭球体 如果我们假设数据服从多元正态分布,数据点在空间中形成一个超椭球体(Hyper-ellipsoid)。 - 协方差矩阵 \(\mathbf{S}\) 描述了这个椭球体的形状。 - 特征向量 \(\mathbf{w}_i\) 是椭球体的主轴方向(半长轴、半短轴…)。 - 特征值 \(\lambda_i\) 对应主轴长度的平方(即该方向上的方差)。 PCA 本质上就是找到这个数据椭球体的主轴,并将坐标系旋转对齐到这些主轴上。

Geometric Interpretation: The Data Ellipsoid If we assume the data follows a multivariate normal distribution, the data points form a hyper-ellipsoid in space. - The covariance matrix \(\mathbf{S}\) describes the shape of this ellipsoid. - The eigenvectors \(\mathbf{w}_i\) are the principal axis directions of the ellipsoid (semi-major axis, semi-minor axis, etc.). - The eigenvalues \(\lambda_i\) correspond to the squares of the principal axis lengths (i.e., the variance in that direction). PCA essentially finds the principal axes of this data ellipsoid and rotates the coordinate system to align with these axes.

13.5.2 方差解释与主成分选择 (Variance Explained and Principal Component Selection)

总方差: \(\sum_{j=1}^p \lambda_j = \text{tr}(S)\)

Total Variance: \(\sum_{j=1}^p \lambda_j = \text{tr}(S)\)

第\(k\)主成分解释的方差比例如 式 13.4 所示:

The proportion of variance explained by the \(k\)-th principal component is shown in 式 13.4:

\[ \frac{\lambda_k}{\sum_{j=1}^p \lambda_j} \tag{13.4}\]

主成分数量选择:

Selecting the Number of Principal Components:

Kaiser准则: 保留特征值大于1的主成分(适用于标准化数据)

累计方差解释: 保留足够解释80%或90%以上总方差的主成分

Scree图: 寻找特征值下降放缓的”肘部”

Kaiser Criterion: Retain principal components with eigenvalues greater than 1 (applicable to standardized data)

Cumulative Variance Explained: Retain enough principal components to explain 80% or 90% of the total variance

Scree Plot: Look for the “elbow” where the decline in eigenvalues levels off

13.5.3 案例:上市公司财务综合评价 (Case Study: Comprehensive Financial Evaluation of Listed Companies)

什么是主成分分析与财务综合评价?

What is PCA and Comprehensive Financial Evaluation?

评价一家上市公司的财务状况,通常需要综合考虑盈利能力(如ROA)、偿债能力(如资产负债率)、流动性(如流动比率)和规模(如总资产)等多个指标。但这些指标之间往往高度相关——例如规模大的企业可能负债率也较高。主成分分析(PCA)通过正交变换,将这些相关的原始指标转化为少数几个不相关的”主成分”,每个主成分都是原始指标的线性组合,且尽可能多地保留了原始数据的信息量。

Evaluating the financial health of a listed company typically requires considering multiple indicators such as profitability (e.g., ROA), solvency (e.g., debt-to-asset ratio), liquidity (e.g., current ratio), and size (e.g., total assets). However, these indicators are often highly correlated—for example, larger firms may also have higher leverage ratios. PCA uses orthogonal transformations to convert these correlated original indicators into a few uncorrelated “principal components,” each being a linear combination of the original indicators while retaining as much information from the original data as possible.

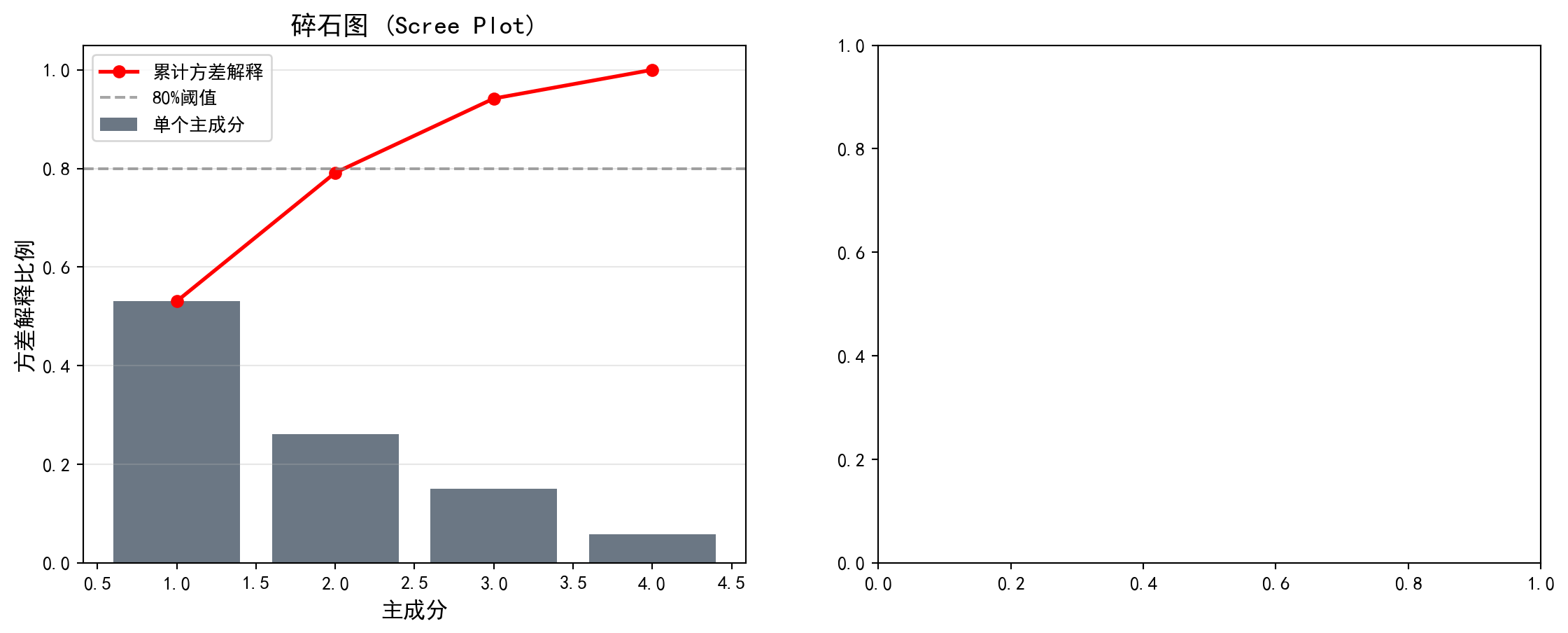

在金融实务中,PCA被广泛用于构建综合评价指标(如用第一主成分作为企业财务实力的综合得分)、多因子模型的因子提取(如Fama-French因子的构建),以及投资组合的风险分解。下面我们对长三角上市公司的财务数据进行PCA分析。图 13.5 展示了特征值和方差解释比例,图 13.6 则通过碎石图和双标图直观展示主成分结构。

In financial practice, PCA is widely used for constructing composite evaluation indices (e.g., using the first principal component as a comprehensive score of corporate financial strength), factor extraction in multi-factor models (e.g., construction of Fama-French factors), and risk decomposition of investment portfolios. Below, we perform PCA analysis on financial data of listed companies in the Yangtze River Delta. 图 13.5 shows the eigenvalues and variance explained ratios, while 图 13.6 provides an intuitive view of the principal component structure through a scree plot and biplot.

# ========== 导入所需库 ==========

# ========== Import Required Libraries ==========

from sklearn.decomposition import PCA # 导入主成分分析模块

# Import the PCA module

# ========== 第1步:准备PCA分析的财务特征数据 ==========

# ========== Step 1: Prepare Financial Feature Data for PCA Analysis ==========

pca_analysis_dataframe = clustering_analysis_dataframe[['roa', 'debt_ratio', 'current_ratio', 'log_assets']].copy() # 选择四个财务特征

# Select four financial features

pca_analysis_dataframe = pca_analysis_dataframe.dropna() # 删除含缺失值的样本

# Drop samples with missing values

pca_analysis_dataframe = pca_analysis_dataframe[ # 过滤各指标的极端异常值

# Filter extreme outliers for each indicator

(pca_analysis_dataframe['roa'] > -50) & (pca_analysis_dataframe['roa'] < 30) & # 过滤ROA极端值

# Filter extreme ROA values

(pca_analysis_dataframe['debt_ratio'] > 0) & (pca_analysis_dataframe['debt_ratio'] < 100) & # 过滤资产负债率极端值

# Filter extreme debt-to-asset ratio values

(pca_analysis_dataframe['current_ratio'] > 0) & (pca_analysis_dataframe['current_ratio'] < 10) # 过滤流动比率极端值

# Filter extreme current ratio values

] # 完成PCA数据的异常值过滤

# Complete outlier filtering for PCA data

# ========== 第2步:标准化并执行PCA ==========

# ========== Step 2: Standardize and Perform PCA ==========

pca_standard_scaler = StandardScaler() # 创建标准化器

# Create a standardizer

pca_scaled_features_matrix = pca_standard_scaler.fit_transform(pca_analysis_dataframe) # 标准化特征矩阵

# Standardize the feature matrix

principal_component_analysis_model = PCA() # 创建PCA模型(保留全部主成分)

# Create a PCA model (retaining all principal components)

pca_transformed_features_matrix = principal_component_analysis_model.fit_transform(pca_scaled_features_matrix) # 执行PCA变换

# Perform PCA transformationPCA模型拟合与主成分变换完成。下面输出各主成分的特征值和方差解释比例。

PCA model fitting and principal component transformation are complete. Below, we output the eigenvalues and variance explained ratios for each principal component.

# ========== 第3步:输出PCA分析结果 ==========

# ========== Step 3: Output PCA Analysis Results ==========

print('=== PCA分析结果 ===\n') # 输出标题

# Print header

print('特征值(方差):') # 输出特征值标题

# Print eigenvalue header

for principal_component_index, explained_variance_value in enumerate(principal_component_analysis_model.explained_variance_): # 遍历每个主成分

# Iterate over each principal component

print(f' PC{principal_component_index+1}: {explained_variance_value:.4f}') # 输出各主成分的特征值

# Print the eigenvalue of each principal component

print('\n方差解释比例:') # 输出方差解释比例标题

# Print variance explained ratio header

for principal_component_index, explained_variance_ratio_value in enumerate(principal_component_analysis_model.explained_variance_ratio_): # 遍历每个主成分

# Iterate over each principal component

cumulative_explained_variance_ratio = sum(principal_component_analysis_model.explained_variance_ratio_[:principal_component_index+1]) # 计算累计解释比例

# Compute cumulative explained ratio

print(f' PC{principal_component_index+1}: {explained_variance_ratio_value*100:.2f}% (累计: {cumulative_explained_variance_ratio*100:.2f}%)') # 输出单个和累计比例

# Print individual and cumulative ratios=== PCA分析结果 ===

特征值(方差):

PC1: 2.1237

PC2: 1.0434

PC3: 0.6021

PC4: 0.2329

方差解释比例:

PC1: 53.06% (累计: 53.06%)

PC2: 26.07% (累计: 79.14%)

PC3: 15.05% (累计: 94.18%)

PC4: 5.82% (累计: 100.00%)运行结果显示,四个主成分的特征值分别为2.1237、1.0434、0.6021和0.2329。第一主成分(PC1)解释了总方差的53.06%,即仅一个综合指标就捕获了四个财务变量中超过一半的信息量。第二主成分(PC2)额外解释了26.07%,前两个主成分的累计解释比例达到79.14%,已接近80%的常用阈值。前三个主成分累计解释94.18%的总方差,说明四维财务数据中的绝大部分信息可以被有效压缩到三维甚至二维空间。第四主成分仅贡献5.82%,属于可以舍弃的”噪声”维度。

The results show that the eigenvalues of the four principal components are 2.1237, 1.0434, 0.6021, and 0.2329, respectively. The first principal component (PC1) explains 53.06% of the total variance, meaning a single composite indicator captures more than half of the information in the four financial variables. The second principal component (PC2) explains an additional 26.07%, and the cumulative explained ratio of the first two components reaches 79.14%, approaching the common threshold of 80%. The first three principal components cumulatively explain 94.18% of the total variance, indicating that the vast majority of information in the four-dimensional financial data can be effectively compressed into three- or even two-dimensional space. The fourth principal component contributes only 5.82%, representing a “noise” dimension that can be discarded.

下面我们通过碎石图和双标图进行可视化。碎石图帮助我们确定应保留多少个主成分:

Below, we visualize the results through a scree plot and a biplot. The scree plot helps us determine how many principal components to retain:

# ========== 第1步:创建双图布局并绘制碎石图 ==========

# ========== Step 1: Create Dual-Plot Layout and Draw Scree Plot ==========

pca_visualization_figure, pca_visualization_axes = plt.subplots(1, 2, figsize=(14, 5)) # 创建1行2列子图

# Create a 1-row, 2-column subplot layout

# ========== 第2步:左图 — 碎石图 (Scree Plot) ==========

# ========== Step 2: Left Panel — Scree Plot ==========

scree_plot_axes = pca_visualization_axes[0] # 获取左侧子图

# Get the left subplot

scree_plot_axes.bar(range(1, len(principal_component_analysis_model.explained_variance_ratio_)+1), # x轴:主成分编号

# x-axis: principal component number

principal_component_analysis_model.explained_variance_ratio_, # y轴:各主成分的方差解释比例

# y-axis: variance explained ratio of each principal component

color='#2C3E50', alpha=0.7, label='单个主成分') # 暗蓝色柱状图

# Dark blue bar chart

scree_plot_axes.plot(range(1, len(principal_component_analysis_model.explained_variance_ratio_)+1), # x轴:主成分编号

# x-axis: principal component number

np.cumsum(principal_component_analysis_model.explained_variance_ratio_), # y轴:累计方差解释比例

# y-axis: cumulative variance explained ratio

'ro-', linewidth=2, label='累计方差解释') # 红色折线表示累计解释

# Red line represents cumulative explained variance

scree_plot_axes.axhline(y=0.8, color='gray', linestyle='--', alpha=0.7, label='80%阈值') # 添加80%参考线

# Add 80% reference line

scree_plot_axes.set_xlabel('主成分', fontsize=12) # 设置x轴标签

# Set x-axis label

scree_plot_axes.set_ylabel('方差解释比例', fontsize=12) # 设置y轴标签

# Set y-axis label

scree_plot_axes.set_title('碎石图 (Scree Plot)', fontsize=14) # 设置标题

# Set title

scree_plot_axes.legend() # 添加图例

# Add legend

scree_plot_axes.grid(True, alpha=0.3, axis='y') # 添加y轴网格线

# Add y-axis grid lines

碎石图展示了各主成分的方差解释比例及累计解释量。下面在右侧绘制双标图(Biplot),同时展示降维后各样本在前两个主成分空间中的分布及原始变量的载荷方向:

The scree plot displays the variance explained ratio and cumulative explained variance for each principal component. Next, we draw a biplot on the right panel, simultaneously showing the distribution of samples in the first two principal component space and the loading directions of the original variables:

# ========== 第3步:右图 — 双标图 (Biplot) ==========

# ========== Step 3: Right Panel — Biplot ==========

biplot_axes = pca_visualization_axes[1] # 获取右侧子图

# Get the right subplot

biplot_axes.scatter(pca_transformed_features_matrix[:, 0], pca_transformed_features_matrix[:, 1], alpha=0.5, c='#008080', s=30) # 绘制样本在PC1-PC2空间的散点图

# Plot samples as scatter points in PC1-PC2 space

# --- 绘制特征向量(载荷)箭头 ---

# --- Draw Feature Vector (Loading) Arrows ---

principal_component_feature_names_list = ['ROA', '资产负债率', '流动比率', '资产规模'] # 特征名称列表

# List of feature names

principal_component_loadings_matrix = principal_component_analysis_model.components_.T * np.sqrt(principal_component_analysis_model.explained_variance_) # 计算缩放后的载荷矩阵

# Compute the scaled loading matrix

for feature_index, (feature_name, loading_vector) in enumerate(zip(principal_component_feature_names_list, principal_component_loadings_matrix)): # 遍历每个特征

# Iterate over each feature

biplot_axes.arrow(0, 0, loading_vector[0]*3, loading_vector[1]*3, # 从原点绘制箭头表示特征方向

# Draw an arrow from the origin indicating the feature direction

head_width=0.15, head_length=0.1, fc='#E3120B', ec='#E3120B') # 红色箭头

# Red arrow

biplot_axes.text(loading_vector[0]*3.2, loading_vector[1]*3.2, feature_name, fontsize=11, # 在箭头末端标注特征名称

# Label the feature name at the arrow tip

color='#E3120B', ha='center') # 红色文字居中对齐

# Red text, center-aligned

biplot_axes.set_xlabel(f'PC1 ({principal_component_analysis_model.explained_variance_ratio_[0]*100:.1f}%)', fontsize=12) # x轴标签包含PC1解释比例

# x-axis label includes PC1 explained ratio

biplot_axes.set_ylabel(f'PC2 ({principal_component_analysis_model.explained_variance_ratio_[1]*100:.1f}%)', fontsize=12) # y轴标签包含PC2解释比例

# y-axis label includes PC2 explained ratio

biplot_axes.set_title('双标图 (Biplot)', fontsize=14) # 设置标题

# Set title

biplot_axes.grid(True, alpha=0.3) # 添加网格线

# Add grid lines

biplot_axes.axhline(y=0, color='gray', linestyle='-', alpha=0.3) # 添加水平参考线

# Add horizontal reference line

biplot_axes.axvline(x=0, color='gray', linestyle='-', alpha=0.3) # 添加垂直参考线

# Add vertical reference line

plt.tight_layout() # 自动调整子图间距

# Auto-adjust subplot spacing

plt.show() # 显示图表

# Display the chart<Figure size 672x480 with 0 Axes>PCA可视化图表展示完毕。下面输出主成分载荷矩阵及其经济学含义解释。

The PCA visualization charts are now complete. Below, we output the principal component loading matrix and its economic interpretation.

# ========== 第4步:输出主成分载荷矩阵及解释 ==========

# ========== Step 4: Output Principal Component Loading Matrix and Interpretation ==========

print('\n=== 主成分载荷 ===') # 输出标题

# Print header

principal_component_loadings_dataframe = pd.DataFrame( # 构建主成分载荷矩阵DataFrame

# Construct the principal component loading matrix DataFrame

principal_component_analysis_model.components_.T, # 载荷矩阵转置

# Transpose of the loading matrix

columns=[f'PC{feature_index+1}' for feature_index in range(principal_component_analysis_model.n_components_)], # 列名为PC1~PC4

# Column names are PC1 to PC4

index=principal_component_feature_names_list # 行名为特征名称

# Row names are feature names

) # 完成载荷矩阵DataFrame构建

# Complete the loading matrix DataFrame construction

print(principal_component_loadings_dataframe.round(4)) # 输出载荷矩阵(保留四位小数)

# Print the loading matrix (rounded to 4 decimal places)

print('\n=== 载荷解释 ===') # 输出解释标题

# Print interpretation header

print('PC1: 主要反映盈利能力(ROA载荷高)和财务稳健性(资产负债率载荷负)') # 解释PC1的经济含义

# Interpret the economic meaning of PC1

print('PC2: 主要反映公司规模(资产规模载荷高)和流动性') # 解释PC2的经济含义

# Interpret the economic meaning of PC2

=== 主成分载荷 ===

PC1 PC2 PC3 PC4

ROA -0.2489 0.8417 -0.4548 0.1512

资产负债率 0.6320 -0.0416 -0.1722 0.7544

流动比率 -0.5948 -0.0074 0.5166 0.6158

资产规模 0.4298 0.5383 0.7047 -0.1696

=== 载荷解释 ===

PC1: 主要反映盈利能力(ROA载荷高)和财务稳健性(资产负债率载荷负)

PC2: 主要反映公司规模(资产规模载荷高)和流动性载荷矩阵的运行结果提供了主成分经济含义的定量依据。具体解读如下:

The loading matrix results provide quantitative evidence for the economic interpretation of the principal components. The detailed interpretation is as follows:

PC1(解释53.06%方差)——“杠杆与流动性对立轴”:资产负债率在PC1上的载荷为0.6320(最大正值),流动比率载荷为-0.5948(最大负值),资产规模载荷为0.4298(正值),而ROA载荷仅为-0.2489(绝对值较小)。这说明PC1主要捕捉的是企业财务结构的差异:PC1得分高的企业倾向于高杠杆、低流动性、大规模,而PC1得分低的企业则呈现轻资产、高流动性的特征。

PC1 (Explaining 53.06% Variance) — “Leverage vs. Liquidity Opposition Axis”: The debt-to-asset ratio has a loading of 0.6320 on PC1 (the largest positive value), the current ratio has a loading of -0.5948 (the largest negative value), asset size has a loading of 0.4298 (positive), while ROA’s loading is only -0.2489 (relatively small in absolute value). This indicates that PC1 primarily captures differences in corporate financial structure: firms with high PC1 scores tend to have high leverage, low liquidity, and large size, while firms with low PC1 scores exhibit asset-light, high-liquidity characteristics.

PC2(解释26.07%方差)——“盈利与规模共振轴”:ROA在PC2上的载荷高达0.8417(绝对最大值),资产规模载荷为0.5383,而资产负债率和流动比率的载荷分别仅为-0.0416和-0.0074,几乎为零。这表明PC2主要反映了企业的盈利能力和规模效应:PC2得分高的企业同时具有较高的ROA和较大的资产规模。

PC2 (Explaining 26.07% Variance) — “Profitability and Size Resonance Axis”: ROA has a loading of 0.8417 on PC2 (the largest in absolute value), asset size has a loading of 0.5383, while the loadings for debt-to-asset ratio and current ratio are only -0.0416 and -0.0074 respectively, nearly zero. This indicates that PC2 primarily reflects corporate profitability and scale effects: firms with high PC2 scores simultaneously have higher ROA and larger asset size.

从双标图中可以直观看到,ROA和资产规模的箭头方向大致朝向右上方(PC1和PC2均为正),而资产负债率箭头朝向右侧(主要沿PC1正方向),流动比率箭头则朝向左侧(沿PC1负方向),与资产负债率近乎相反——这反映了财务理论中杠杆率与流动比率之间的天然负相关关系。

From the biplot, we can intuitively see that the arrows for ROA and asset size point roughly toward the upper right (positive on both PC1 and PC2), while the debt-to-asset ratio arrow points to the right (mainly along the positive PC1 direction), and the current ratio arrow points to the left (along the negative PC1 direction), nearly opposite to the debt-to-asset ratio—this reflects the natural negative correlation between leverage ratio and current ratio in financial theory.

13.6 t-SNE和UMAP (t-SNE and UMAP)

13.6.1 t-SNE

t-SNE(t-distributed Stochastic Neighbor Embedding)是一种非线性降维方法,特别适合可视化高维数据。

t-SNE (t-distributed Stochastic Neighbor Embedding) is a nonlinear dimensionality reduction method particularly well-suited for visualizing high-dimensional data.

核心思想:

- 在高维空间用高斯分布刻画点对之间的相似性

- 在低维空间用t分布(自由度为1)刻画相似性

- 最小化两个分布之间的KL散度,如 式 13.5 所示:

Core Idea:

- Use Gaussian distributions to characterize pairwise similarities in the high-dimensional space

- Use the t-distribution (with 1 degree of freedom) to characterize similarities in the low-dimensional space

- Minimize the KL divergence between the two distributions, as shown in 式 13.5:

\[ D_{KL}(P||Q) = \sum_i \sum_{j \neq i} p_{ij} \log\frac{p_{ij}}{q_{ij}} \tag{13.5}\]

特点:

- 能够揭示局部结构

- 不保持全局距离关系

- 计算成本较高

- 参数perplexity影响结果

Characteristics:

- Capable of revealing local structure

- Does not preserve global distance relationships

- Computationally expensive

- The perplexity parameter affects results

图 13.7 展示了t-SNE将财务特征映射到2D空间的可视化结果。

图 13.7 shows the visualization of t-SNE mapping financial features into 2D space.

13.6.2 UMAP

UMAP(Uniform Manifold Approximation and Projection)是t-SNE的改进版本:

UMAP (Uniform Manifold Approximation and Projection) is an improved version of t-SNE:

运行速度更快

更好地保持全局结构

有理论基础(黎曼几何和拓扑数据分析)

Faster runtime

Better preservation of global structure

Has theoretical foundations (Riemannian geometry and topological data analysis)

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

from sklearn.manifold import TSNE # 导入t-SNE降维模块

# Import the t-SNE dimensionality reduction module

# ========== 第1步:执行t-SNE降维 ==========

# ========== Step 1: Perform t-SNE dimensionality reduction ==========

t_sne_dimensionality_reduction_model = TSNE(n_components=2, random_state=42, perplexity=30, max_iter=1000) # 创建t-SNE模型(降至2维,困惑度=30)

# Create t-SNE model (reduce to 2D, perplexity=30)

t_sne_transformed_features_matrix = t_sne_dimensionality_reduction_model.fit_transform(pca_scaled_features_matrix[:500]) # 取前500个样本以加快计算速度

# Take the first 500 samples to speed up computation

# ========== 第2步:获取对应的聚类标签 ==========

# ========== Step 2: Obtain corresponding cluster labels ==========

subset_cluster_labels_array = features_for_clustering_dataframe['cluster'].values[:500] # 取前500个样本的聚类标签

# Get cluster labels for the first 500 samples

# ========== 第3步:可视化t-SNE结果 ==========

# ========== Step 3: Visualize t-SNE results ==========

t_sne_visualization_figure, t_sne_visualization_axes = plt.subplots(figsize=(10, 8)) # 创建图表

# Create the figure

for cluster_label_index in range(chosen_number_of_clusters): # 遍历每个聚类簇

# Iterate over each cluster

t_sne_cluster_mask_series = subset_cluster_labels_array == cluster_label_index # 创建当前簇的布尔掩码

# Create a boolean mask for the current cluster

t_sne_visualization_axes.scatter(t_sne_transformed_features_matrix[t_sne_cluster_mask_series, 0], t_sne_transformed_features_matrix[t_sne_cluster_mask_series, 1], # 绘制散点

c=cluster_display_colors_list[cluster_label_index], label=f'簇{cluster_label_index+1}', alpha=0.6, s=50) # 按簇着色

# Plot scatter points colored by cluster

t_sne_visualization_axes.set_xlabel('t-SNE 维度1', fontsize=12) # 设置x轴标签

# Set x-axis label

t_sne_visualization_axes.set_ylabel('t-SNE 维度2', fontsize=12) # 设置y轴标签

# Set y-axis label

t_sne_visualization_axes.set_title('t-SNE可视化(颜色表示K-means聚类结果)', fontsize=14) # 设置标题

# Set the title

t_sne_visualization_axes.legend() # 添加图例

# Add legend

t_sne_visualization_axes.grid(True, alpha=0.3) # 添加网格线

# Add grid lines

plt.tight_layout() # 自动调整布局

# Auto-adjust layout

plt.show() # 显示图表

# Display the figure

print('t-SNE将财务特征映射到2D空间,同色点表示同一K-means簇') # 输出说明

# Print explanation

print('可以观察到聚类结果在t-SNE空间中的分离程度') # 输出观察提示

# Print observation hint

t-SNE将财务特征映射到2D空间,同色点表示同一K-means簇

可以观察到聚类结果在t-SNE空间中的分离程度图 13.7 的运行结果展示了t-SNE将四维财务特征空间映射到二维平面后的散点图,其中每个点代表一家上市公司,颜色对应其K-means聚类标签。从图中可以观察到以下特征:簇4(中等规模均衡企业,最大簇,n=889)在t-SNE空间中占据了较大的中心区域;簇3(财务困境企业,n=161)在空间中形成了相对独立的小块聚集区,与其他簇有一定的间隔,说明这些企业在原始四维特征空间中确实与主流企业存在显著差异;而簇1与簇2在t-SNE映射后存在一定程度的交叠,这与它们在部分财务指标上的相似性一致。

The results of 图 13.7 display the scatter plot after t-SNE maps the four-dimensional financial feature space to a two-dimensional plane, where each point represents a listed company and the color corresponds to its K-means cluster label. The following characteristics can be observed: Cluster 4 (medium-sized balanced companies, the largest cluster, n=889) occupies a large central area in the t-SNE space; Cluster 3 (financially distressed companies, n=161) forms relatively independent small clusters in the space with some separation from other clusters, indicating that these companies are indeed significantly different from mainstream companies in the original four-dimensional feature space; Clusters 1 and 2 show some degree of overlap after t-SNE mapping, which is consistent with their similarities in certain financial indicators.

需要注意的是,t-SNE是一种非线性降维方法,它能够保留数据的局部邻域结构(即原始空间中相近的点在映射后仍然相近),但全局距离关系可能被扭曲——因此,图中簇之间的绝对距离不宜过度解读,但簇内的紧密聚集程度和簇间的分离趋势仍然具有参考价值。

It should be noted that t-SNE is a nonlinear dimensionality reduction method that preserves the local neighborhood structure of the data (i.e., points that are close in the original space remain close after mapping), but global distance relationships may be distorted — therefore, the absolute distances between clusters in the figure should not be over-interpreted, yet the degree of compactness within clusters and the separation trends between clusters still carry reference value.

13.7 聚类评估 (Clustering Evaluation)

13.7.1 内部评估指标 (Internal Evaluation Metrics)

不需要真实标签的评估方法,表 13.1 展示了常用聚类评估指标的计算结果:

Evaluation methods that do not require ground-truth labels. 表 13.1 presents the computed results of commonly used clustering evaluation metrics:

1. 轮廓系数(Silhouette Score)

- 范围:\([-1, 1]\)

- 值越大越好

1. Silhouette Score

- Range: \([-1, 1]\)

- Higher values are better

2. Calinski-Harabasz指数

- 簇间方差与簇内方差的比值

- 值越大越好

2. Calinski-Harabasz Index

- Ratio of between-cluster variance to within-cluster variance

- Higher values are better

3. Davies-Bouldin指数

- 簇的平均相似度

- 值越小越好

3. Davies-Bouldin Index

- Average similarity between clusters

- Lower values are better

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

from sklearn.metrics import silhouette_score, calinski_harabasz_score, davies_bouldin_score # 导入三种聚类评估指标

# Import three clustering evaluation metrics

# ========== 第1步:计算三种内部聚类评估指标 ==========

# ========== Step 1: Compute three internal clustering evaluation metrics ==========

calculated_silhouette_score_value = silhouette_score(scaled_features_matrix, features_for_clustering_dataframe['cluster']) # 轮廓系数:衡量簇内紧凑度和簇间分离度

# Silhouette score: measures intra-cluster compactness and inter-cluster separation

calculated_calinski_harabasz_score_value = calinski_harabasz_score(scaled_features_matrix, features_for_clustering_dataframe['cluster']) # CH指数:簇间方差/簇内方差的比值

# CH index: ratio of between-cluster variance to within-cluster variance

calculated_davies_bouldin_score_value = davies_bouldin_score(scaled_features_matrix, features_for_clustering_dataframe['cluster']) # DB指数:簇的平均相似度

# DB index: average similarity between clusters

# ========== 第2步:输出评估结果 ==========

# ========== Step 2: Output evaluation results ==========

print('=== 聚类评估指标 ===\n') # 输出标题

# Print header

print(f'轮廓系数 (Silhouette): {calculated_silhouette_score_value:.4f} (范围[-1,1], 越大越好)') # 轮廓系数结果

# Silhouette score result

print(f'Calinski-Harabasz指数: {calculated_calinski_harabasz_score_value:.2f} (越大越好)') # CH指数结果

# CH index result

print(f'Davies-Bouldin指数: {calculated_davies_bouldin_score_value:.4f} (越小越好)') # DB指数结果

# DB index result=== 聚类评估指标 ===

轮廓系数 (Silhouette): 0.3012 (范围[-1,1], 越大越好)

Calinski-Harabasz指数: 840.68 (越大越好)

Davies-Bouldin指数: 1.0640 (越小越好)上述代码的运行结果如下:轮廓系数为0.3012,位于\([0, 1]\)的中低区间,表明各簇之间存在一定程度的重叠,聚类结构并非十分清晰——这在金融数据中是常见现象,因为企业的财务特征往往呈连续分布而非截然分群。Calinski-Harabasz指数为840.68,该值相对较高,说明簇间方差远大于簇内方差,聚类在整体上成功地将具有不同财务特征的企业区分开来。Davies-Bouldin指数为1.0640,略高于1.0的理想阈值,进一步印证了某些簇之间存在一定的边界模糊性。

The results of the above code are as follows: the silhouette score is 0.3012, in the low-to-mid range of \([0, 1]\), indicating a certain degree of overlap between clusters and that the clustering structure is not very clear — this is a common phenomenon in financial data, as companies’ financial characteristics tend to follow a continuous distribution rather than distinct groupings. The Calinski-Harabasz index is 840.68, a relatively high value indicating that the between-cluster variance is much larger than the within-cluster variance, meaning the clustering has overall successfully distinguished companies with different financial characteristics. The Davies-Bouldin index is 1.0640, slightly above the ideal threshold of 1.0, further confirming a certain degree of boundary ambiguity between some clusters.

综合三项指标来看,K=4的K-means聚类对长三角上市公司财务数据产生了中等质量的分群效果:聚类整体结构有效(高CH指数),但部分簇之间的界限并不锐利(中等轮廓系数、略高DB指数)。在实际应用中,这样的结果仍然具有商业分析价值,尤其是在识别极端簇(如财务困境企业)方面效果显著。

Considering all three metrics together, K-means clustering with K=4 produced a moderate quality grouping of the Yangtze River Delta listed companies’ financial data: the overall clustering structure is effective (high CH index), but the boundaries between some clusters are not sharp (moderate silhouette score, slightly high DB index). In practical applications, such results still carry business analysis value, especially in identifying extreme clusters (such as financially distressed companies) where the effectiveness is notable.

13.7.2 外部评估指标(如有真实标签) (External Evaluation Metrics, If Ground-Truth Labels Are Available)

调整兰德指数(ARI): 考虑随机性的标签一致性

标准化互信息(NMI): 基于信息论的相似度

同质性与完整性: V-measure

Adjusted Rand Index (ARI): Label consistency accounting for randomness

Normalized Mutual Information (NMI): Information-theory-based similarity

Homogeneity and Completeness: V-measure

13.8 启发式思考题 (Heuristic Problems)

1. 幽灵聚类 (Spurious Clusters)

- 操作:生成 1000 个在 \([0, 1]^2\) 正方形内均匀分布的随机点(完全没有聚类结构)。

- 执行:强行运行 K-means (\(K=3\))。

- 结果:你会得到 3 个漂亮的、看起来很像那么回事的簇。甚至轮廓系数可能还不错。

- 反思:算法永远会给你一个答案,不管这答案有没有意义。在没有先验知识的情况下,如何区分”真聚类”和”随机划分”?

1. Spurious Clusters

- Operation: Generate 1000 random points uniformly distributed within the \([0, 1]^2\) square (with absolutely no clustering structure).

- Execution: Force-run K-means (\(K=3\)).

- Result: You will obtain 3 neat, seemingly reasonable clusters. The silhouette score might even look decent.

- Reflection: An algorithm will always give you an answer, regardless of whether that answer is meaningful. Without prior knowledge, how do you distinguish “real clusters” from “random partitions”?

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import numpy as np # 导入数值计算库

# Import numerical computation library

from sklearn.cluster import KMeans # 导入K-Means聚类算法

# Import K-Means clustering algorithm

from sklearn.metrics import silhouette_score # 导入轮廓系数评估指标

# Import silhouette score evaluation metric

import matplotlib.pyplot as plt # 导入绘图库

# Import plotting library

import platform # 导入平台检测模块

# Import platform detection module

# ========== 中文字体设置 ==========

# ========== Chinese font configuration ==========

if platform.system() == 'Linux': # 判断是否为Linux平台

# Check if running on Linux

plt.rcParams['font.sans-serif'] = ['Source Han Serif SC', 'SimHei', 'DejaVu Sans'] # Linux字体优先级

# Linux font priority

else: # Windows平台

# Windows platform

plt.rcParams['font.sans-serif'] = ['SimHei', 'Microsoft YaHei'] # Windows字体优先级

# Windows font priority

plt.rcParams['axes.unicode_minus'] = False # 解决负号显示问题

# Fix negative sign display issue

# ========== 第1步:生成完全随机的均匀分布数据 ==========

# ========== Step 1: Generate completely random uniformly distributed data ==========

random_number_generator = np.random.RandomState(42) # 创建固定种子的随机数生成器

# Create a random number generator with a fixed seed

number_of_random_points = 1000 # 设置随机点数为1000

# Set the number of random points to 1000

uniform_random_points_matrix = random_number_generator.uniform(0, 1, size=(number_of_random_points, 2)) # 在[0,1]^2正方形内生成均匀分布的随机点

# Generate uniformly distributed random points within the [0,1]^2 square

# ========== 第2步:对随机数据强行运行K-means ==========

# ========== Step 2: Force-run K-means on random data ==========

forced_kmeans_model = KMeans(n_clusters=3, random_state=42, n_init=10) # 创建K-means模型(强制K=3)

# Create K-means model (forced K=3)

spurious_cluster_labels_array = forced_kmeans_model.fit_predict(uniform_random_points_matrix) # 拟合并预测聚类标签

# Fit and predict cluster labels

spurious_silhouette_score_value = silhouette_score(uniform_random_points_matrix, spurious_cluster_labels_array) # 计算轮廓系数

# Compute silhouette score随机数据生成与K-means聚类完成。下面创建对比图展示”幽灵聚类”效果。首先绘制左侧的原始数据分布图:

Random data generation and K-means clustering are complete. Below we create a comparison chart to demonstrate the “spurious clustering” effect. First, we plot the original data distribution on the left:

# ========== 第3步:创建双图布局并绘制左图(原始数据) ==========

# ========== Step 3: Create dual-panel layout and plot the left panel (original data) ==========

spurious_clusters_figure, spurious_clusters_axes = plt.subplots(1, 2, figsize=(14, 5)) # 创建1行2列子图

# Create 1-row, 2-column subplot layout

# --- 左图:原始数据(无颜色区分) ---

# --- Left panel: Original data (no color differentiation) ---

original_data_axes = spurious_clusters_axes[0] # 获取左侧子图

# Get the left subplot