# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import pandas as pd # 数据处理库

# Data manipulation library

import numpy as np # 数值计算库

# Numerical computation library

from sklearn.tree import DecisionTreeClassifier, plot_tree, export_text # 决策树分类器及可视化工具

# Decision tree classifier and visualization tools

from sklearn.model_selection import train_test_split, cross_val_score # 数据拆分与交叉验证

# Data splitting and cross-validation

from sklearn.metrics import accuracy_score, classification_report, roc_auc_score, roc_curve # 评估指标

# Evaluation metrics

import matplotlib.pyplot as plt # 数据可视化库

# Data visualization library

import platform # 平台检测模块

# Platform detection module

# ========== 中文字体设置 ==========

# ========== Chinese font configuration ==========

if platform.system() == 'Linux': # Linux系统

# Linux system

plt.rcParams['font.sans-serif'] = ['Source Han Serif SC', 'SimHei', 'DejaVu Sans'] # 思源宋体优先

# Source Han Serif SC preferred

else: # Windows系统

# Windows system

plt.rcParams['font.sans-serif'] = ['SimHei', 'Microsoft YaHei'] # 黑体优先

# SimHei preferred

plt.rcParams['axes.unicode_minus'] = False # 解决负号显示问题

# Fix minus sign display issue

# ========== 第1步:读取本地财务数据 ==========

# ========== Step 1: Load local financial data ==========

if platform.system() == 'Linux': # 根据操作系统选择数据路径

# Select data path based on operating system

data_path = '/home/ubuntu/r2_data_mount/qiufei/data/stock' # Linux路径

# Linux path

else: # 否则为Windows系统

# Otherwise Windows system

data_path = 'C:/qiufei/data/stock' # Windows路径

# Windows path

financial_statement_dataframe = pd.read_hdf(f'{data_path}/financial_statement.h5') # 读取财务报表

# Read financial statements

stock_basic_info_dataframe = pd.read_hdf(f'{data_path}/stock_basic_data.h5') # 读取股票基本信息

# Read stock basic information12 基于树的机器学习方法 (Tree-Based Machine Learning Methods)

决策树及其集成方法(随机森林、梯度提升)是现代机器学习中最强大的预测工具之一,在商业分析、金融风控、信用评级等领域有广泛应用。树方法能自动捕捉非线性关系和变量交互效应,无需显式指定模型形式,且对异常值和缺失数据具有天然的稳健性。本章首先介绍决策树的基本算法(小节 12.2),然后讨论随机森林(小节 12.4)和XGBoost(小节 12.5)等集成方法,最后探讨模型可解释性(小节 12.6)。

Decision trees and their ensemble methods (random forests, gradient boosting) are among the most powerful predictive tools in modern machine learning, with broad applications in business analytics, financial risk management, and credit rating. Tree-based methods can automatically capture nonlinear relationships and variable interaction effects without explicitly specifying the model form, and are naturally robust to outliers and missing data. This chapter first introduces the basic decision tree algorithm (小节 12.2), then discusses ensemble methods such as random forests (小节 12.4) and XGBoost (小节 12.5), and finally explores model interpretability (小节 12.6).

12.1 树方法在量化金融中的典型应用 (Typical Applications of Tree Methods in Quantitative Finance)

决策树及其集成方法打破了传统统计建模对线性假设和参数形式的依赖,在金融领域展现出强大的预测能力。以下展示其在中国资本市场中的核心应用场景。

Decision trees and their ensemble methods break free from the dependence on linearity assumptions and parametric forms in traditional statistical modeling, demonstrating strong predictive power in the financial domain. The following presents their core application scenarios in the Chinese capital market.

12.1.1 应用一:基于机器学习的量化选股 (Application 1: Machine Learning-Based Quantitative Stock Selection)

传统多因子选股模型(参见 章节 10)假设因子与收益率之间存在线性关系。但A股市场中,因子与收益率的关系往往是非线性的且存在大量交互效应。随机森林和XGBoost等集成树方法可以自动捕捉这些复杂关系。利用 valuation_factors_quarterly_15_years.h5 中的估值因子作为特征,以下期股票收益率排名作为目标变量,可以构建预测能力显著优于线性模型的选股策略。

Traditional multi-factor stock selection models (see 章节 10) assume a linear relationship between factors and returns. However, in the A-share market, the relationship between factors and returns is often nonlinear with extensive interaction effects. Ensemble tree methods such as random forests and XGBoost can automatically capture these complex relationships. Using valuation factors from valuation_factors_quarterly_15_years.h5 as features and next-period stock return rankings as the target variable, one can construct stock selection strategies with predictive power significantly superior to linear models.

12.1.2 应用二:信用评级与风险预警 (Application 2: Credit Rating and Risk Early Warning)

在信用风险评估中(参见 章节 11 中的Logistic回归方法),梯度提升树(XGBoost/LightGBM)因其卓越的预测精度已成为业界标准工具。基于 financial_statement.h5 中的财务指标(如流动比率、资产负债率、现金流比率等),树方法不仅能识别出关键风险因子,还能通过特征重要性(Feature Importance)和SHAP值提供可解释的风险归因分析。

In credit risk assessment (see the Logistic regression method in 章节 11), gradient boosting trees (XGBoost/LightGBM) have become the industry standard tool due to their outstanding predictive accuracy. Based on financial indicators from financial_statement.h5 (such as current ratio, debt-to-asset ratio, cash flow ratio, etc.), tree methods can not only identify key risk factors but also provide interpretable risk attribution analysis through Feature Importance and SHAP values.

12.1.3 应用三:市场状态识别与择时策略 (Application 3: Market Regime Identification and Timing Strategies)

将 stock_price_pre_adjusted.h5 中的技术指标(如波动率、成交量变化、均线偏离度等)作为特征,以未来市场涨跌作为目标变量,可以训练树模型识别不同的市场状态(牛市/熊市/震荡市),为投资择时提供参考。

Using technical indicators from stock_price_pre_adjusted.h5 (such as volatility, trading volume changes, moving average deviations, etc.) as features and future market movements as the target variable, tree models can be trained to identify different market regimes (bull/bear/sideways markets), providing references for investment timing decisions.

直观几何解释:

Intuitive Geometric Interpretation:

决策树本质上是用超矩形(Hyper-rectangles)来切割特征空间。

Decision trees essentially partition the feature space using hyper-rectangles.

每一刀(分割)都必须平行于坐标轴(\(X_j \leq s\))。

最终,特征空间被切成无数个不重叠的小方块(叶节点)。

相比于线性回归(用超平面切割),决策树能逼近任意形状的非线性边界,只要切得足够细(树足够深)。

Each cut (split) must be parallel to a coordinate axis (\(X_j \leq s\)).

Ultimately, the feature space is partitioned into numerous non-overlapping small rectangles (leaf nodes).

Compared to linear regression (which cuts with hyperplanes), decision trees can approximate nonlinear boundaries of arbitrary shapes, as long as the cuts are fine enough (the tree is deep enough).

但这也带来了过拟合的风险——切得太细,就变成了死记硬背。

However, this also introduces the risk of overfitting—cutting too finely amounts to memorizing the training data.

12.2 决策树算法 (Decision Tree Algorithms)

12.2.1 CART算法框架 (CART Algorithm Framework)

CART(Classification and Regression Trees)是最常用的决策树算法,采用贪心策略进行二叉递归分割。

CART (Classification and Regression Trees) is the most commonly used decision tree algorithm, employing a greedy strategy for binary recursive partitioning.

算法流程:

Algorithm Procedure:

初始化: 全部数据构成根节点

最优分割: 对当前节点,遍历所有特征\(j\)和所有可能的分割点\(s\):

- 定义两个区域:\(R_1(j,s) = \{X|X_j \leq s\}\),\(R_2(j,s) = \{X|X_j > s\}\)

- 选择使某种不纯度度量最小化的\((j^*, s^*)\)

递归分割: 对生成的两个子节点重复步骤2

停止条件: 节点样本数小于阈值,或不纯度不再下降,或达到最大深度

剪枝: 通过交叉验证选择最优复杂度参数

Initialization: All data forms the root node

Optimal Split: For the current node, iterate over all features \(j\) and all possible split points \(s\):

- Define two regions: \(R_1(j,s) = \{X|X_j \leq s\}\), \(R_2(j,s) = \{X|X_j > s\}\)

- Select \((j^*, s^*)\) that minimizes a certain impurity measure

Recursive Splitting: Repeat step 2 for each generated child node

Stopping Criteria: Node sample size falls below a threshold, impurity no longer decreases, or maximum depth is reached

Pruning: Select the optimal complexity parameter via cross-validation

12.2.2 分类树的分割准则 (Splitting Criteria for Classification Trees)

对于分类问题,常用的不纯度度量包括:

For classification problems, commonly used impurity measures include:

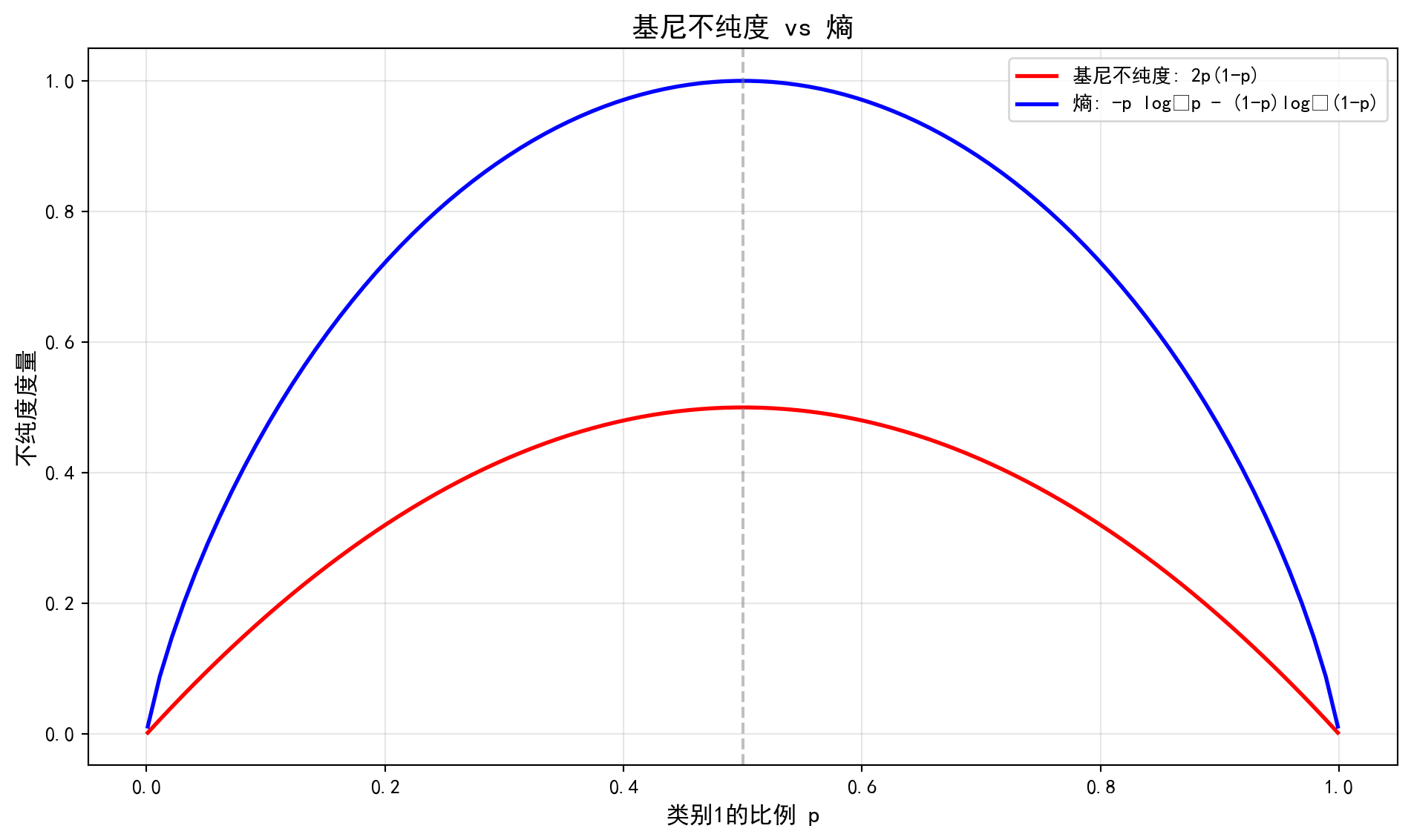

1. 基尼不纯度(Gini Impurity)

1. Gini Impurity

\[ G(p) = \sum_{k=1}^K p_k(1-p_k) = 1 - \sum_{k=1}^K p_k^2 \tag{12.1}\]

式 12.1 中,\(p_k\)是节点中第\(k\)类的样本比例。

In 式 12.1, \(p_k\) is the proportion of samples belonging to class \(k\) in the node.

基尼不纯度与熵的数学关系(泰勒展开)

Mathematical Relationship Between Gini Impurity and Entropy (Taylor Expansion)

为什么 CART 用 Gini 而 C4.5 用 Entropy?

Why does CART use Gini while C4.5 uses Entropy?

熵的定义:\(H(p) = -p \ln(p) - (1-p) \ln(1-p)\)

The definition of entropy: \(H(p) = -p \ln(p) - (1-p) \ln(1-p)\)

在 \(p=1\) 附近对 \(H(p)\) 进行一阶泰勒展开(\(\ln(x) \approx x-1\)):

Performing a first-order Taylor expansion of \(H(p)\) near \(p=1\) (\(\ln(x) \approx x-1\)):

\[ -\ln(p) \approx 1-p \]

代入熵公式:

Substituting into the entropy formula:

\[ H(p) \approx p(1-p) + (1-p)p = 2p(1-p) = G(p) \]

这说明:基尼不纯度实际上是熵的一阶近似。

This shows that: Gini impurity is actually a first-order approximation of entropy.

计算上:Gini不需要算对数,速度更快(在计算机算力稀缺的80年代很重要)。

性质上:两者极其相似,但在极端情况(极纯或极不纯)下略有差异。

Computationally: Gini does not require logarithm calculations and is faster (which was important in the 1980s when computing power was scarce).

In terms of properties: The two are extremely similar, but differ slightly in extreme cases (very pure or very impure).

2. 熵(Entropy)/信息增益

2. Entropy / Information Gain

什么是熵?

What is Entropy?

熵(Entropy) 是信息论中衡量不确定性或混乱程度的核心指标,由香农(Claude Shannon)在1948年提出。直观理解:如果一个事件的结果越难预测,它的熵就越高。

Entropy is the core metric in information theory for measuring uncertainty or disorder, proposed by Claude Shannon in 1948. Intuitively: the harder it is to predict the outcome of an event, the higher its entropy.

用一个简单例子来说明:

A simple example illustrates this:

一枚公平硬币(正面概率50%,反面概率50%):抛一次,你完全无法预测结果——不确定性最大,熵最高。

一枚灌铅硬币(正面概率99%,反面概率1%):抛一次,你几乎可以确定是正面——不确定性很低,熵很低。

一枚双面相同的硬币(正面概率100%):结果完全确定,没有任何不确定性——熵为零。

A fair coin (50% heads, 50% tails): flip it once, and you cannot predict the result at all—uncertainty is maximized, entropy is highest.

A loaded coin (99% heads, 1% tails): flip it once, and you can almost certainly predict heads—uncertainty is very low, entropy is very low.

A double-headed coin (100% heads): the result is completely certain, with no uncertainty—entropy is zero.

在决策树的语境中,我们用熵来衡量一个节点中样本标签的”混乱程度”:如果一个节点中所有样本都属于同一类别(纯净),熵为0;如果样本在各类别中均匀分布(完全混合),熵达到最大值。决策树的目标就是通过不断分裂,使子节点的熵尽可能低——即让每个叶节点尽可能”纯净”。

In the context of decision trees, we use entropy to measure the “disorder” of sample labels within a node: if all samples in a node belong to the same class (pure), entropy is 0; if samples are uniformly distributed across classes (completely mixed), entropy reaches its maximum. The goal of a decision tree is to reduce child node entropy as much as possible through successive splits—that is, to make each leaf node as “pure” as possible.

熵的数学公式如 式 12.2 所示:

The mathematical formula for entropy is shown in 式 12.2:

\[ H(p) = -\sum_{k=1}^K p_k \log_2 p_k \tag{12.2}\]

熵的公式如 式 12.2 所示。信息增益(Information Gain)定义为父节点熵与子节点加权平均熵的差(见 式 12.3):

The entropy formula is shown in 式 12.2. Information Gain is defined as the difference between the parent node entropy and the weighted average entropy of the child nodes (see 式 12.3):

\[ IG = H(\text{parent}) - \sum_{c \in \{L,R\}} \frac{n_c}{n} H(c) \tag{12.3}\]

3. 两种准则的比较

3. Comparison of the Two Criteria

| 准则 | 计算复杂度 | 特点 |

|---|---|---|

| Gini | 较低(无对数) | CART默认,偏好较大分区 |

| Entropy | 较高 | ID3/C4.5使用,更敏感于类别分布 |

| Criterion | Computational Complexity | Characteristics |

|---|---|---|

| Gini | Lower (no logarithm) | CART default, prefers larger partitions |

| Entropy | Higher | Used by ID3/C4.5, more sensitive to class distribution |

实践中,两者性能通常相近。

In practice, the performance of the two is generally similar.

12.2.3 回归树的分割准则 (Splitting Criteria for Regression Trees)

对于回归问题,使用均方误差(MSE)作为分割准则:

For regression problems, Mean Squared Error (MSE) is used as the splitting criterion:

\[ MSE = \frac{1}{n}\sum_{i=1}^n (y_i - \bar{y})^2 \tag{12.4}\]

如 式 12.4 所示。选择使两个子区域MSE加权之和最小的分割(见 式 12.5):

As shown in 式 12.4. The split that minimizes the weighted sum of MSE of the two child regions is selected (see 式 12.5):

\[ \min_{j,s} \left[ \frac{n_L}{n} MSE(R_L) + \frac{n_R}{n} MSE(R_R) \right] \tag{12.5}\]

其中\(n_L, n_R\)分别是左右子节点的样本数。

where \(n_L, n_R\) are the number of samples in the left and right child nodes, respectively.

12.2.4 最优分割点的搜索 (Search for the Optimal Split Point)

分割点搜索算法

Split Point Search Algorithm

对于特征\(X_j\):

For feature \(X_j\):

将\(n\)个样本按\(X_j\)值排序:\(x_{(1)j} \leq x_{(2)j} \leq ... \leq x_{(n)j}\)

候选分割点:\(\{s_i = \frac{x_{(i)j} + x_{(i+1)j}}{2}\}_{i=1}^{n-1}\)

对每个\(s_i\)计算不纯度减少量

选择不纯度减少最大的分割点

Sort the \(n\) samples by \(X_j\) values: \(x_{(1)j} \leq x_{(2)j} \leq ... \leq x_{(n)j}\)

Candidate split points: \(\{s_i = \frac{x_{(i)j} + x_{(i+1)j}}{2}\}_{i=1}^{n-1}\)

Compute the impurity reduction for each \(s_i\)

Select the split point with the greatest impurity reduction

计算复杂度: 对于\(p\)个特征,\(n\)个样本,每次分割需要\(O(np\log n)\)时间。

Computational Complexity: For \(p\) features and \(n\) samples, each split requires \(O(np\log n)\) time.

12.2.5 剪枝策略 (Pruning Strategies)

过拟合问题: 完全生长的树往往过拟合训练数据。

Overfitting Problem: A fully grown tree tends to overfit the training data.

代价复杂度剪枝(Cost-Complexity Pruning):

Cost-Complexity Pruning:

最小化:

Minimize:

\[ C_\alpha(T) = \sum_{m=1}^{|T|} \sum_{x_i \in R_m} L(y_i, c_m) + \alpha|T| \tag{12.6}\]

式 12.6 中各项含义如下:

The terms in 式 12.6 are defined as follows:

\(|T|\): 叶节点数(树的复杂度)

\(\alpha\): 复杂度参数(控制正则化强度)

通过交叉验证选择最优\(\alpha\)

\(|T|\): Number of leaf nodes (tree complexity)

\(\alpha\): Complexity parameter (controls regularization strength)

The optimal \(\alpha\) is selected via cross-validation

12.3 案例:上市公司违约风险预测 (Case Study: Default Risk Prediction for Listed Companies)

什么是基于决策树的信用风险评估?

What is Decision Tree-Based Credit Risk Assessment?

信用风险评估是金融机构最核心的业务能力之一。银行在发放贷款前,需要评估借款企业未来违约的可能性;债券投资者在购入公司债前,需要判断发行方的偿债能力。传统的信用评级方法依赖专家经验和简单的财务比率分析,而决策树模型提供了一种数据驱动的自动化评估方案。

Credit risk assessment is one of the most core business capabilities of financial institutions. Before issuing loans, banks need to evaluate the likelihood of borrower default; before purchasing corporate bonds, investors need to assess the issuer’s debt-servicing capacity. Traditional credit rating methods rely on expert judgment and simple financial ratio analysis, whereas decision tree models provide a data-driven, automated assessment approach.

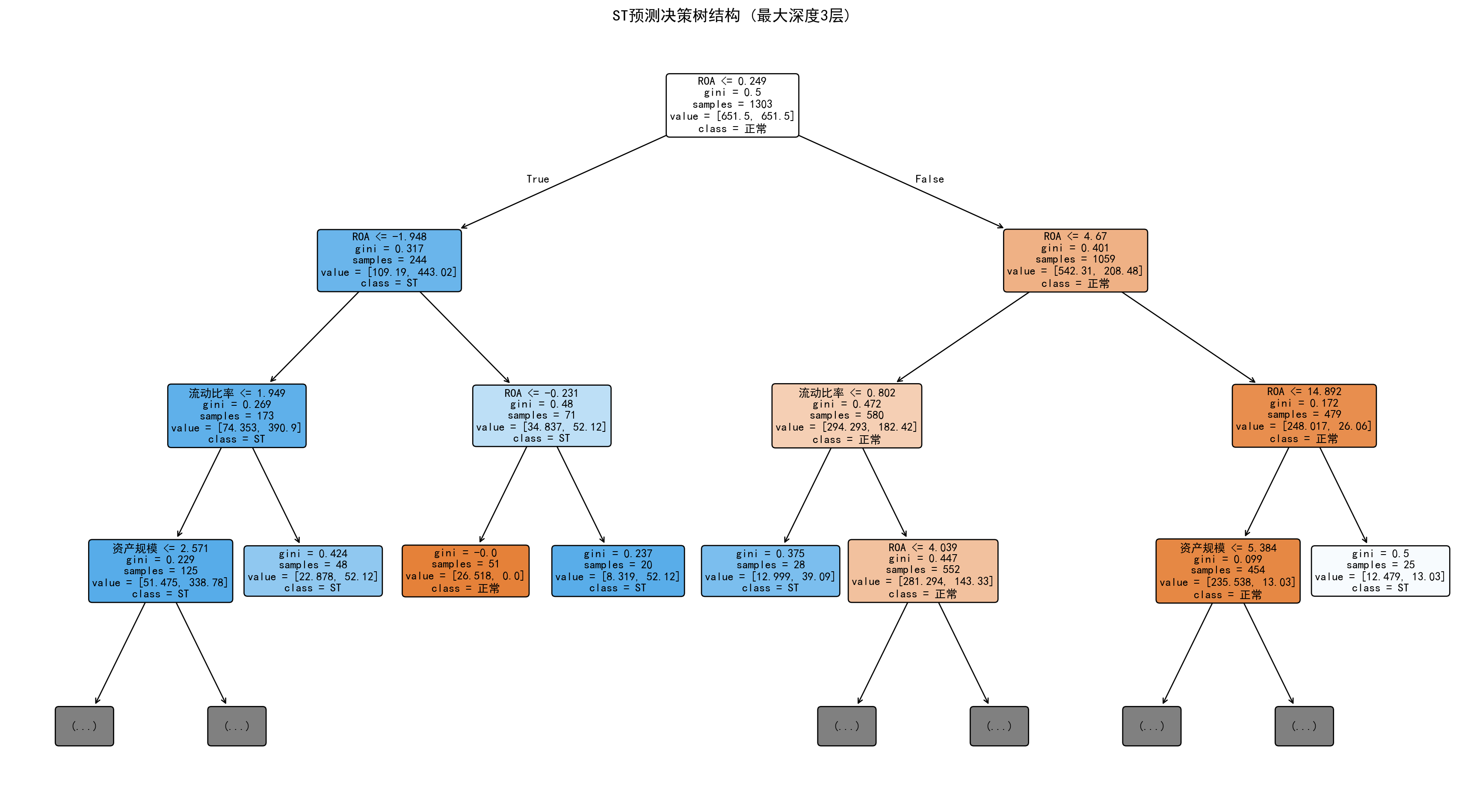

决策树的核心优势在于其可解释性——模型通过层层划分财务指标(如”资产负债率是否大于70%?““流动比率是否小于1?”),形成一棵直观的”if-then”规则树,信贷审批人员可以清晰地理解每个决策节点的判断逻辑。这使得决策树在金融监管要求模型透明度的场景下尤为适用。下面我们使用长三角上市公司的财务数据,建立决策树模型预测违约风险。模型训练结果如 表 12.1 所示,决策树结构可视化如 图 12.1 所示。

The core advantage of decision trees lies in their interpretability—the model forms an intuitive “if-then” rule tree by progressively partitioning financial indicators (e.g., “Is the debt-to-asset ratio greater than 70%?” “Is the current ratio less than 1?”), enabling credit approval officers to clearly understand the decision logic at each node. This makes decision trees particularly suitable in scenarios where financial regulators require model transparency. Below, we use financial data from Yangtze River Delta listed companies to build a decision tree model for predicting default risk. The model training results are shown in 表 12.1, and the decision tree structure visualization is shown in 图 12.1.

决策树建模所需的库导入和本地财务数据加载完毕。下面筛选2023年年报数据,合并公司基本信息并构建长三角非金融企业建模样本。

The libraries required for decision tree modeling have been imported and local financial data has been loaded. Next, we filter 2023 annual report data, merge company basic information, and construct a modeling sample of non-financial enterprises in the Yangtze River Delta.

# ========== 第2步:筛选2023年年报并合并基本信息 ==========

# ========== Step 2: Filter 2023 annual reports and merge basic information ==========

annual_report_dataframe_2023 = financial_statement_dataframe[ # 筛选2023年第四季度数据

# Filter Q4 2023 data

(financial_statement_dataframe['quarter'].str.endswith('q4')) & # 第四季度(年报)

# Fourth quarter (annual report)

(financial_statement_dataframe['quarter'].str.startswith('2023')) # 2023年

# Year 2023

].copy() # 复制筛选后的2023年年报数据子集

# Copy the filtered 2023 annual report data subset

annual_report_dataframe_2023 = annual_report_dataframe_2023.merge( # 合并股票基本信息

# Merge stock basic information

stock_basic_info_dataframe[['order_book_id', 'abbrev_symbol', 'industry_name', 'province']], # 取代码、简称、行业、省份

# Select stock code, abbreviation, industry, province

on='order_book_id', how='left' # 按股票代码左连接

# Left join on stock code

)

# ========== 第3步:创建ST标识并筛选长三角非金融企业 ==========

# ========== Step 3: Create ST flag and filter YRD non-financial enterprises ==========

annual_report_dataframe_2023['is_st'] = annual_report_dataframe_2023['abbrev_symbol'].str.contains( # 识别ST标记

# Identify ST designation

'ST|\\*ST', na=False # 匹配ST或*ST

# Match ST or *ST

).astype(int) # 转为0/1整数

# Convert to 0/1 integer

yangtze_river_delta_areas_list = ['上海市', '江苏省', '浙江省', '安徽省'] # 长三角四省市

# Four YRD provinces/municipalities

financial_industries_list = ['货币金融服务', '保险业', '其他金融业'] # 金融行业(需排除)

# Financial industries (to be excluded)

decision_tree_model_dataframe = annual_report_dataframe_2023[ # 筛选建模样本

# Filter modeling sample

(annual_report_dataframe_2023['province'].isin(yangtze_river_delta_areas_list)) & # 长三角地区

# Yangtze River Delta region

(~annual_report_dataframe_2023['industry_name'].isin(financial_industries_list)) & # 非金融行业

# Non-financial industries

(annual_report_dataframe_2023['total_assets'] > 0) # 总资产为正

# Positive total assets

].copy() # 复制筛选后的建模样本数据

# Copy the filtered modeling sample data数据加载与样本筛选完成。下面计算关键财务指标并清理异常值。

Data loading and sample filtering are complete. Next, we compute key financial indicators and clean outliers.

# ========== 第4步:计算关键财务指标 ==========

# ========== Step 4: Compute key financial indicators ==========

decision_tree_model_dataframe['roa'] = ( # 总资产收益率ROA(%)

# Return on Assets ROA (%)

decision_tree_model_dataframe['net_profit'] / # 净利润

# Net profit

decision_tree_model_dataframe['total_assets'] * 100 # 除以总资产再乘100转百分比

# Divided by total assets, multiplied by 100 to convert to percentage

)

decision_tree_model_dataframe['debt_ratio'] = ( # 资产负债率(%)

# Debt-to-asset ratio (%)

decision_tree_model_dataframe['total_liabilities'] / # 总负债

# Total liabilities

decision_tree_model_dataframe['total_assets'] * 100 # 除以总资产再乘100转百分比

# Divided by total assets, multiplied by 100 to convert to percentage

)

decision_tree_model_dataframe['current_ratio'] = np.where( # 流动比率

# Current ratio

decision_tree_model_dataframe['current_liabilities'] > 0, # 流动负债大于0时

# When current liabilities > 0

decision_tree_model_dataframe['current_assets'] / decision_tree_model_dataframe['current_liabilities'], # 流动资产/流动负债

# Current assets / current liabilities

np.nan # 否则设为缺失值

# Otherwise set to missing

)

decision_tree_model_dataframe['log_assets'] = np.log( # 资产规模(对数)

# Asset size (logarithm)

decision_tree_model_dataframe['total_assets'] / 1e8 # 总资产除以1亿后取自然对数

# Natural log of total assets divided by 100 million

)

# ========== 第5步:去除异常值并清理缺失值 ==========

# ========== Step 5: Remove outliers and clean missing values ==========

decision_tree_model_dataframe = decision_tree_model_dataframe[ # 按合理区间筛选

# Filter by reasonable ranges

(decision_tree_model_dataframe['roa'] > -50) & (decision_tree_model_dataframe['roa'] < 30) & # ROA在-50%~30%之间

# ROA between -50% and 30%

(decision_tree_model_dataframe['debt_ratio'] > 0) & (decision_tree_model_dataframe['debt_ratio'] < 120) & # 负债率在0~120%之间

# Debt ratio between 0 and 120%

(decision_tree_model_dataframe['current_ratio'] > 0) & (decision_tree_model_dataframe['current_ratio'] < 10) # 流动比率在0~10之间

# Current ratio between 0 and 10

].dropna(subset=['is_st', 'roa', 'debt_ratio', 'current_ratio', 'log_assets']) # 删除关键变量的缺失值

# Drop missing values for key variables

print(f'样本量: {len(decision_tree_model_dataframe)} 家公司') # 输出样本量

# Print sample size

print(f'ST公司: {decision_tree_model_dataframe["is_st"].sum()} 家 ({decision_tree_model_dataframe["is_st"].mean()*100:.2f}%)') # 输出ST占比

# Print ST company count and percentage样本量: 1862 家公司

ST公司: 72 家 (3.87%)数据已准备就绪,长三角非金融上市公司的财务指标和ST标识均已生成。运行结果显示,筛选后的样本包含 1862 家公司,其中 ST公司仅72家,占比约3.87%。这一极低的ST比例揭示了典型的类别不平衡(Class Imbalance)问题——正常公司数量远超ST公司。在后续建模中,我们将通过设置 class_weight='balanced' 参数自动调整类别权重,使模型对少数类(ST公司)给予更高的关注度,避免模型简单地将所有公司预测为”正常”而获得虚高的准确率。

The data is now ready, with financial indicators and ST flags generated for non-financial listed companies in the Yangtze River Delta. The results show that the filtered sample contains 1,862 companies, of which only 72 are ST companies, accounting for approximately 3.87%. This extremely low ST proportion reveals a typical class imbalance problem—the number of normal companies far exceeds that of ST companies. In subsequent modeling, we will automatically adjust class weights by setting the class_weight='balanced' parameter, giving higher attention to the minority class (ST companies) and preventing the model from simply predicting all companies as “normal” to achieve an artificially high accuracy rate.

下面进入建模阶段:将数据划分为训练集和测试集,训练决策树分类器,并输出模型评估指标与特征重要性排序。

Now we enter the modeling phase: splitting the data into training and test sets, training the decision tree classifier, and outputting model evaluation metrics and feature importance rankings.

# ========== 第6步:准备建模数据 ==========

# ========== Step 6: Prepare modeling data ==========

predictor_variables_list = ['roa', 'debt_ratio', 'current_ratio', 'log_assets'] # 特征变量列表

# List of predictor variables

design_matrix_features = decision_tree_model_dataframe[predictor_variables_list] # 提取特征矩阵X

# Extract feature matrix X

target_variable_series = decision_tree_model_dataframe['is_st'] # 提取目标变量y

# Extract target variable y

# ========== 第7步:划分训练集与测试集 ==========

# ========== Step 7: Split into training and test sets ==========

features_train_matrix, features_test_matrix, target_train_series, target_test_series = train_test_split( # 划分训练集和测试集

# Split into training and test sets

design_matrix_features, target_variable_series, # 输入特征和目标

# Input features and target

test_size=0.3, # 30%作为测试集

# 30% as test set

random_state=42, # 随机种子保证可复现

# Random seed for reproducibility

stratify=target_variable_series # 按目标变量分层抽样(保持ST比例一致)

# Stratified sampling by target variable (maintain ST proportion)

)

# ========== 第8步:训练决策树分类器 ==========

# ========== Step 8: Train decision tree classifier ==========

fitted_decision_tree_classifier = DecisionTreeClassifier( # 创建决策树模型

# Create decision tree model

max_depth=4, # 最大深度限制为4层(防止过拟合)

# Maximum depth limited to 4 levels (prevent overfitting)

min_samples_leaf=20, # 叶节点最少20个样本

# Minimum 20 samples per leaf node

min_samples_split=50, # 内部节点分裂最少需要50个样本

# Minimum 50 samples required to split an internal node

class_weight='balanced', # 自动平衡类别权重(应对ST样本稀少)

# Automatically balance class weights (handle scarce ST samples)

random_state=42 # 随机种子

# Random seed

)

fitted_decision_tree_classifier.fit(features_train_matrix, target_train_series) # 在训练集上拟合模型

# Fit the model on the training setDecisionTreeClassifier(class_weight='balanced', max_depth=4,

min_samples_leaf=20, min_samples_split=50,

random_state=42)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

| criterion | 'gini' | |

| splitter | 'best' | |

| max_depth | 4 | |

| min_samples_split | 50 | |

| min_samples_leaf | 20 | |

| min_weight_fraction_leaf | 0.0 | |

| max_features | None | |

| random_state | 42 | |

| max_leaf_nodes | None | |

| min_impurity_decrease | 0.0 | |

| class_weight | 'balanced' | |

| ccp_alpha | 0.0 | |

| monotonic_cst | None |

决策树模型训练完毕。下面在测试集上进行预测并评估模型性能。

The decision tree model training is complete. Next, we make predictions on the test set and evaluate model performance.

# ========== 第9步:预测与模型评估 ==========

# ========== Step 9: Prediction and model evaluation ==========

predicted_classes_array = fitted_decision_tree_classifier.predict(features_test_matrix) # 预测类别标签

# Predict class labels

predicted_probabilities_array = fitted_decision_tree_classifier.predict_proba(features_test_matrix)[:, 1] # 预测ST概率

# Predict ST probability

print(f'\n=== 决策树模型评估 ===') # 输出评估标题

# Print evaluation header

print(f'准确率: {accuracy_score(target_test_series, predicted_classes_array):.4f}') # 计算并输出准确率

# Compute and print accuracy

if len(np.unique(target_test_series)) > 1: # 如果测试集包含两个类别

# If test set contains two classes

print(f'AUC: {roc_auc_score(target_test_series, predicted_probabilities_array):.4f}') # 计算并输出AUC

# Compute and print AUC

# ========== 第10步:输出特征重要性排序 ==========

# ========== Step 10: Output feature importance rankings ==========

print('\n特征重要性:') # 输出标题

# Print header

feature_importance_dataframe = pd.DataFrame({ # 构建特征重要性DataFrame

# Construct feature importance DataFrame

'特征': predictor_variables_list, # 特征名称列

# Feature name column

'重要性': fitted_decision_tree_classifier.feature_importances_ # 重要性得分列

# Importance score column

}).sort_values('重要性', ascending=False) # 按重要性降序排列

# Sort by importance in descending order

print(feature_importance_dataframe.to_string(index=False)) # 输出(不显示索引)

# Print (without index)

=== 决策树模型评估 ===

准确率: 0.8032

AUC: 0.7872

特征重要性:

特征 重要性

roa 0.895240

current_ratio 0.066525

log_assets 0.038236

debt_ratio 0.000000为了更直观地理解决策树的分裂逻辑和判断规则,下面我们将训练好的决策树模型进行可视化展示。

To more intuitively understand the splitting logic and decision rules of the decision tree, we will visualize the trained decision tree model below.

上述代码运行结果显示,决策树模型在测试集上的准确率为 0.8032,即约80%的公司被正确分类;AUC为 0.7872,表明模型具有一定的区分正常公司与ST公司的能力,但距离理想的AUC=1.0还有较大提升空间。特征重要性排序揭示了一个极端现象:ROA(总资产收益率)的重要性高达0.8952,几乎独占了决策树的全部分裂依据;流动比率(0.0665)和资产规模(0.0382)仅有微弱贡献,而资产负债率的重要性竟然为0——这意味着在当前树结构中,资产负债率从未被用于节点分裂。这一结果既体现了ROA作为盈利能力核心指标对财务困境的强预测力,也暴露了单棵决策树的局限性:贪心算法倾向于过度依赖单一强特征,忽略其他潜在有用的变量。

The above results show that the decision tree model achieves an accuracy of 0.8032 on the test set, meaning approximately 80% of companies are correctly classified; the AUC is 0.7872, indicating that the model has some ability to distinguish between normal and ST companies, but there is still significant room for improvement from the ideal AUC of 1.0. The feature importance rankings reveal an extreme phenomenon: the importance of ROA (Return on Assets) is as high as 0.8952, dominating nearly all splitting decisions of the decision tree; current ratio (0.0665) and asset size (0.0382) make only marginal contributions, while the importance of debt-to-asset ratio is actually 0—meaning it was never used for node splitting in the current tree structure. This result both demonstrates the strong predictive power of ROA as a core profitability indicator for financial distress, and exposes the limitation of a single decision tree: the greedy algorithm tends to over-rely on a single strong feature while ignoring other potentially useful variables.

树的每个节点显示了分裂条件、基尼系数和样本分布,颜色深浅反映节点的纯度高低。

Each node of the tree displays the splitting condition, Gini coefficient, and sample distribution, with color intensity reflecting the node’s purity level.

# ========== 第1步:绘制决策树结构图 ==========

# ========== Step 1: Plot decision tree structure ==========

tree_visualization_figure, tree_visualization_axes = plt.subplots(figsize=(18, 10)) # 创建大画布

# Create a large canvas

plot_tree(fitted_decision_tree_classifier, # 绘制决策树

# Plot the decision tree

max_depth=3, # 只显示前3层(避免过于复杂)

# Display only the top 3 levels (avoid excessive complexity)

feature_names=['ROA', '资产负债率', '流动比率', '资产规模'], # 特征中文名

# Feature names in Chinese

class_names=['正常', 'ST'], # 类别中文名

# Class names in Chinese

filled=True, # 用颜色填充节点(颜色深浅表示纯度)

# Fill nodes with color (intensity indicates purity)

rounded=True, # 圆角矩形节点

# Rounded rectangle nodes

fontsize=10, # 字体大小

# Font size

ax=tree_visualization_axes) # 指定坐标轴

# Specify axes

tree_visualization_axes.set_title('ST预测决策树结构 (最大深度3层)', fontsize=14) # 设置标题

# Set title

plt.tight_layout() # 自动调整布局

# Auto-adjust layout

plt.show() # 显示图形

# Display the figure

# ========== 第2步:输出决策规则文本 ==========

# ========== Step 2: Output decision rules as text ==========

print('\n=== 决策规则 ===') # 输出标题

# Print header

extracted_tree_rules_text = export_text( # 导出决策树的文本规则

# Export the text rules of the decision tree

fitted_decision_tree_classifier, # 已训练的决策树模型

# The trained decision tree model

feature_names=['ROA', '资产负债率', '流动比率', '资产规模'] # 特征名称

# Feature names

)

print(extracted_tree_rules_text[:1500]) # 打印前1500字符(避免输出过长)

# Print first 1500 characters (avoid excessive output)

=== 决策规则 ===

|--- ROA <= 0.25

| |--- ROA <= -1.95

| | |--- 流动比率 <= 1.95

| | | |--- 资产规模 <= 2.57

| | | | |--- class: 1

| | | |--- 资产规模 > 2.57

| | | | |--- class: 1

| | |--- 流动比率 > 1.95

| | | |--- class: 1

| |--- ROA > -1.95

| | |--- ROA <= -0.23

| | | |--- class: 0

| | |--- ROA > -0.23

| | | |--- class: 1

|--- ROA > 0.25

| |--- ROA <= 4.67

| | |--- 流动比率 <= 0.80

| | | |--- class: 1

| | |--- 流动比率 > 0.80

| | | |--- ROA <= 4.04

| | | | |--- class: 0

| | | |--- ROA > 4.04

| | | | |--- class: 1

| |--- ROA > 4.67

| | |--- ROA <= 14.89

| | | |--- 资产规模 <= 5.38

| | | | |--- class: 0

| | | |--- 资产规模 > 5.38

| | | | |--- class: 0

| | |--- ROA > 14.89

| | | |--- class: 1

图 12.1 和决策规则输出清晰地展示了模型的判断逻辑。树的根节点以 ROA ≤ 0.25(即ROA约0.25%)为第一刀,将所有公司分成两个大组。左侧分支(ROA极低的公司)进一步按 ROA ≤ -1.95 和 ROA ≤ -0.23 细分——ROA为负数且幅度较大的公司被强烈判定为ST风险高;右侧分支(ROA略高的公司)则以流动比率 ≤ 1.95 和 ROA ≤ 4.67 进行二次筛选,识别出盈利尚可但流动性不足的潜在风险企业。此外,资产规模(log_assets ≤ 2.57,即总资产约13亿元)也出现在部分叶节点的判断路径中,反映了小型公司的ST风险偏高。整体来看,该决策树揭示了一个清晰的商业逻辑:盈利能力(ROA)是区分财务困境的核心因素,流动性和公司规模起辅助作用。

图 12.1 and the decision rule output clearly demonstrate the model’s decision logic. The root node uses ROA ≤ 0.25 (i.e., ROA approximately 0.25%) as the first split, dividing all companies into two major groups. The left branch (companies with very low ROA) is further subdivided by ROA ≤ -1.95 and ROA ≤ -0.23—companies with negative ROA of large magnitude are strongly classified as high ST risk; the right branch (companies with slightly higher ROA) uses current ratio ≤ 1.95 and ROA ≤ 4.67 for secondary screening, identifying potentially risky enterprises with acceptable profitability but insufficient liquidity. Additionally, asset size (log_assets ≤ 2.57, i.e., total assets of approximately 1.3 billion yuan) also appears in the decision paths of some leaf nodes, reflecting the higher ST risk of smaller companies. Overall, this decision tree reveals a clear business logic: profitability (ROA) is the core factor in distinguishing financial distress, with liquidity and company size playing auxiliary roles.

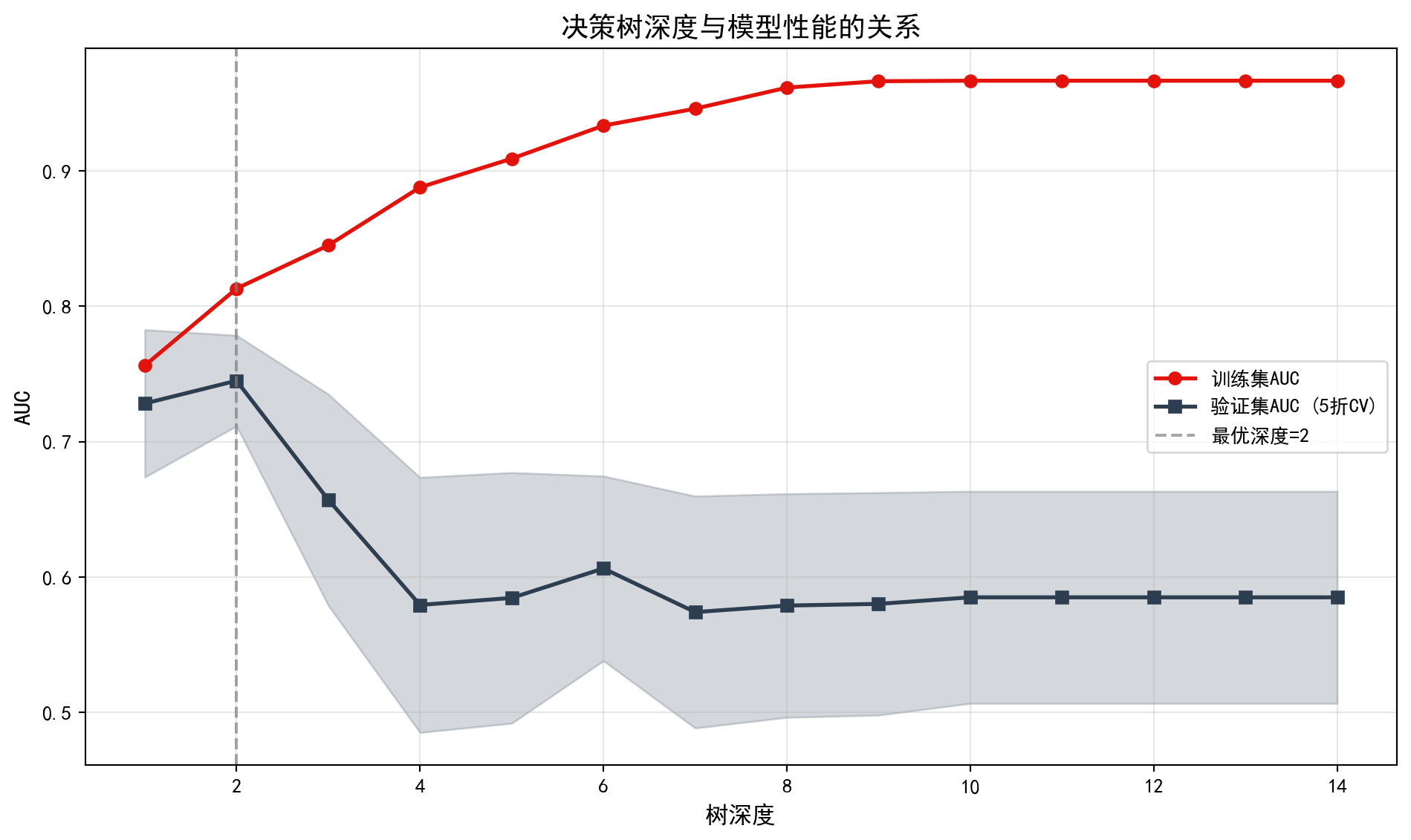

12.3.1 超参数调优:树深度选择 (Hyperparameter Tuning: Tree Depth Selection)

通过交叉验证选择最优树深度,如 图 12.2 所示。

The optimal tree depth is selected via cross-validation, as shown in 图 12.2.

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

from sklearn.model_selection import cross_val_score # 交叉验证评分函数

# Cross-validation scoring function

# ========== 第1步:设定候选深度范围 ==========

# ========== Step 1: Set candidate depth range ==========

candidate_tree_depths_list = range(1, 15) # 候选深度从1到14

# Candidate depths from 1 to 14

cross_validation_scores_mean_list = [] # 存储交叉验证AUC均值

# Store cross-validation AUC means

cross_validation_scores_std_list = [] # 存储交叉验证AUC标准差

# Store cross-validation AUC standard deviations

training_scores_list = [] # 存储训练集AUC

# Store training set AUC候选深度与评分列表初始化完毕。下面遍历各候选深度进行交叉验证。

Candidate depths and scoring lists are initialized. Next, we iterate over each candidate depth for cross-validation.

# ========== 第2步:遍历每个深度进行交叉验证 ==========

# ========== Step 2: Iterate over each depth for cross-validation ==========

for depth in candidate_tree_depths_list: # 逐个测试每个深度

# Test each depth one by one

cross_validation_decision_tree_classifier = DecisionTreeClassifier( # 创建指定深度的决策树

# Create a decision tree with specified depth

max_depth=depth, # 当前测试的深度

# Current depth being tested

min_samples_leaf=10, # 叶节点最少10个样本

# Minimum 10 samples per leaf node

class_weight='balanced', # 类别权重平衡

# Balanced class weights

random_state=42 # 随机种子

# Random seed

)

# --- 5折交叉验证计算验证集AUC ---

# --- 5-fold cross-validation to compute validation AUC ---

calculated_cross_validation_scores = cross_val_score( # 执行交叉验证

# Perform cross-validation

cross_validation_decision_tree_classifier, # 待评估模型

# Model to evaluate

features_train_matrix, target_train_series, # 训练数据

# Training data

cv=5, scoring='roc_auc' # 5折,以AUC为指标

# 5 folds, using AUC as metric

)

cross_validation_scores_mean_list.append(calculated_cross_validation_scores.mean()) # 记录AUC均值

# Record AUC mean

cross_validation_scores_std_list.append(calculated_cross_validation_scores.std()) # 记录AUC标准差

# Record AUC standard deviation

# --- 计算训练集AUC ---

# --- Compute training set AUC ---

cross_validation_decision_tree_classifier.fit(features_train_matrix, target_train_series) # 在全部训练集上拟合

# Fit on the full training set

training_predicted_probabilities_array = cross_validation_decision_tree_classifier.predict_proba( # 预测训练集概率

# Predict training set probabilities

features_train_matrix)[:, 1] # 取ST类别的概率

# Take the probability of the ST class

if len(np.unique(target_train_series)) > 1: # 如果训练集包含两个类别

# If training set contains two classes

training_scores_list.append(roc_auc_score(target_train_series, training_predicted_probabilities_array)) # 计算训练AUC

# Compute training AUC

else: # 训练集只有单一类别时

# When training set has only one class

training_scores_list.append(0) # 否则记为0

# Otherwise record as 0交叉验证评估完成。下面可视化树深度与模型性能的关系。

Cross-validation evaluation is complete. Next, we visualize the relationship between tree depth and model performance.

# ========== 第3步:可视化深度与AUC的关系 ==========

# ========== Step 3: Visualize the relationship between depth and AUC ==========

depth_evaluation_figure, depth_evaluation_axes = plt.subplots(figsize=(10, 6)) # 创建画布

# Create canvas

depth_evaluation_axes.plot(candidate_tree_depths_list, training_scores_list, # 绘制训练集AUC曲线

# Plot training set AUC curve

'o-', color='#E3120B', label='训练集AUC', linewidth=2)

depth_evaluation_axes.plot(candidate_tree_depths_list, cross_validation_scores_mean_list, # 绘制验证集AUC曲线

# Plot validation set AUC curve

's-', color='#2C3E50', label='验证集AUC (5折CV)', linewidth=2)

depth_evaluation_axes.fill_between(candidate_tree_depths_list, # 绘制验证AUC的置信区间

# Plot confidence interval for validation AUC

np.array(cross_validation_scores_mean_list) - np.array(cross_validation_scores_std_list), # 下界

# Lower bound

np.array(cross_validation_scores_mean_list) + np.array(cross_validation_scores_std_list), # 上界

# Upper bound

alpha=0.2, color='#2C3E50') # 半透明填充

# Semi-transparent fill

# ========== 第4步:标记最优深度并美化图表 ==========

# ========== Step 4: Mark optimal depth and beautify the chart ==========

optimal_tree_depth_value = candidate_tree_depths_list[np.argmax(cross_validation_scores_mean_list)] # 找到验证AUC最大的深度

# Find the depth with maximum validation AUC

depth_evaluation_axes.axvline(x=optimal_tree_depth_value, color='gray', linestyle='--', alpha=0.7, # 画最优深度竖线

# Draw vertical line at optimal depth

label=f'最优深度={optimal_tree_depth_value}') # 图例标注最优深度值

# Legend annotation for optimal depth value

depth_evaluation_axes.set_xlabel('树深度', fontsize=12) # X轴标签

# X-axis label

depth_evaluation_axes.set_ylabel('AUC', fontsize=12) # Y轴标签

# Y-axis label

depth_evaluation_axes.set_title('决策树深度与模型性能的关系', fontsize=14) # 图标题

# Chart title

depth_evaluation_axes.legend() # 显示图例

# Show legend

depth_evaluation_axes.grid(True, alpha=0.3) # 添加网格线

# Add gridlines

plt.tight_layout() # 自动调整布局

# Auto-adjust layout

plt.show() # 显示图形

# Display the figure

交叉验证深度选择可视化完成。从 图 12.2 可以观察到典型的偏差-方差权衡模式:训练集AUC(红线)随深度增加而单调上升,在深度14时接近完美的1.0;而验证集AUC(蓝线)在深度2处达到峰值后即开始下降并趋于平稳,且置信区间(阴影区域)随深度增大而逐渐加宽。这说明较深的树虽然能更好地拟合训练数据,但泛化能力反而下降——这正是过拟合的经典表现。下面输出最优树深度及其对应的验证集AUC。

The cross-validation depth selection visualization is complete. From 图 12.2, a typical bias-variance tradeoff pattern can be observed: the training set AUC (red line) increases monotonically with depth, approaching a perfect 1.0 at depth 14; while the validation set AUC (blue line) reaches its peak at depth 2 and then begins to decline and level off, with the confidence interval (shaded area) gradually widening as depth increases. This indicates that although deeper trees can better fit the training data, their generalization ability actually decreases—this is the classic manifestation of overfitting. Below, we output the optimal tree depth and its corresponding validation set AUC.

# ========== 第5步:输出最优深度结论 ==========

# ========== Step 5: Output optimal depth conclusions ==========

print(f'最优深度: {optimal_tree_depth_value}') # 输出最优深度

# Print optimal depth

print(f'对应验证AUC: {max(cross_validation_scores_mean_list):.4f}') # 输出最优验证AUC

# Print optimal validation AUC

print('\n观察: 随着深度增加,训练AUC持续上升,但验证AUC先升后降(过拟合)') # 输出过拟合观察结论

# Print overfitting observation conclusion最优深度: 2

对应验证AUC: 0.7450

观察: 随着深度增加,训练AUC持续上升,但验证AUC先升后降(过拟合)交叉验证结果表明,最优树深度为2,对应的验证集AUC为 0.7450。这意味着仅需两层分裂(即两个判断条件的组合),决策树即可达到最佳的泛化性能。再增加深度只会让模型过度学习训练数据中的噪声,验证AUC反而下降。值得注意的是,0.7450的AUC虽然高于随机猜测(0.5),但在实际金融风控中仍属于”中等偏弱”的水平,提示我们单棵决策树的预测能力有限,有必要探索更强大的集成学习方法。

The cross-validation results indicate that the optimal tree depth is 2, with a corresponding validation set AUC of 0.7450. This means that only two levels of splits (i.e., a combination of two decision conditions) are needed for the decision tree to achieve the best generalization performance. Increasing the depth further only causes the model to overlearn noise in the training data, causing the validation AUC to decrease instead. It is worth noting that while an AUC of 0.7450 is above random guessing (0.5), it is still at a “moderate-to-weak” level in practical financial risk management, suggesting that the predictive capability of a single decision tree is limited and it is necessary to explore more powerful ensemble learning methods. ## 从理论到实践:苦活累活 (From Theory to Practice: The “Dirty Work”) {#sec-dirty-work-ch12}

尽管决策树直观易懂,但它们在实际应用中有一个致命弱点:“即使最强壮的树,也经不起风吹草动”。

Despite how intuitive decision trees are, they have a fatal weakness in practical applications: “Even the strongest tree cannot withstand the slightest breeze.”

12.3.2 结构的不稳定性 (Instability)

决策树是高方差 (High Variance) 模型。

Decision trees are high variance models.

现象:如果你稍微改变训练数据(哪怕只是随机删除 5% 的行,或者改变一个离群值),生成的整棵树结构可能会面目全非(根节点的分割变量都变了)。

原因:贪心算法(Greedy Search)的每一步决策都依赖于上一步。根节点的微小变化会像”蝴蝶效应”一样层层放大,导致后续所有分割点都完全不同。

后果:这也是为什么我们永远不应该基于单棵树做商业决策。必须集成 (Ensemble)。

Phenomenon: If you slightly change the training data (even just randomly removing 5% of the rows, or changing one outlier), the entire tree structure can change beyond recognition (even the splitting variable at the root node may change).

Cause: Each decision in the greedy search algorithm depends on the previous step. A small change at the root node amplifies like a “butterfly effect” through successive layers, causing all subsequent split points to differ completely.

Consequence: This is why we should never make business decisions based on a single tree. Ensembling is essential.

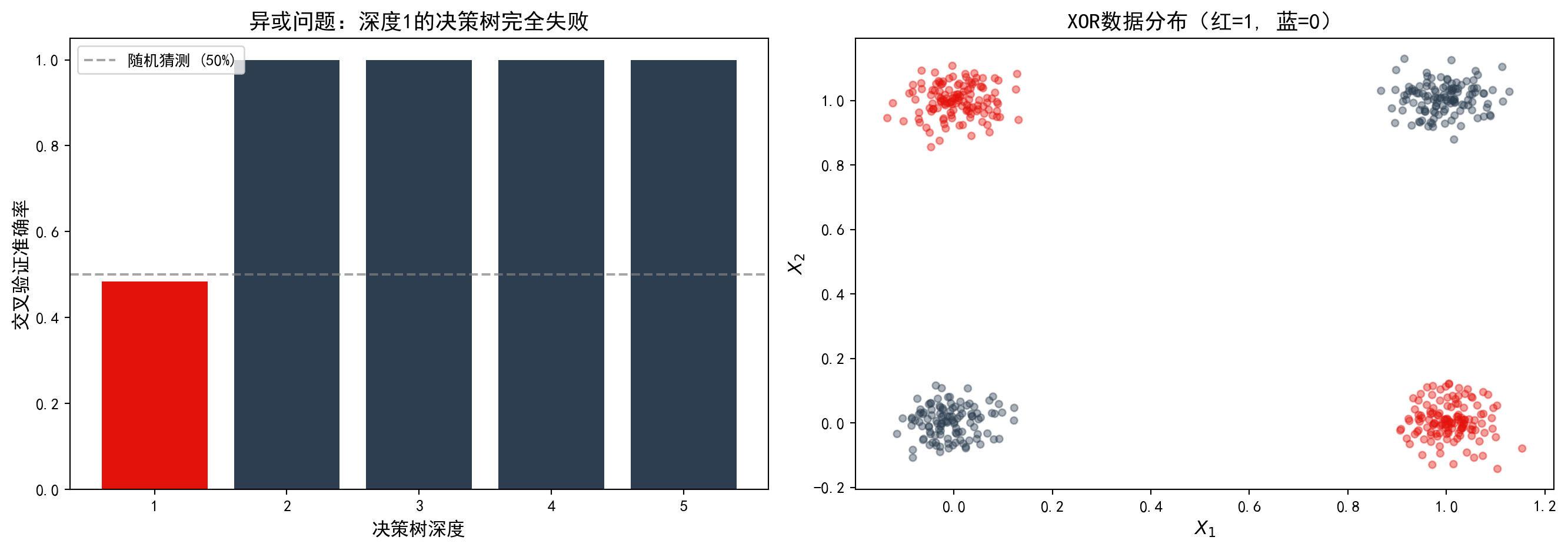

12.3.3 异或问题 (The XOR Problem)

CART 算法每次只切一个变量(轴平行分割)。它很难捕捉变量间的交互作用 (Interaction),特别是 XOR 类型。

The CART algorithm splits on only one variable at a time (axis-parallel splits). It struggles to capture interactions between variables, especially those of the XOR type.

例子:假设 \(Y = X_1 \oplus X_2\)(当且仅当 \(X_1, X_2\) 符号不同时 \(Y=1\))。

困境:单看 \(X_1\),\(Y\) 的分布是均匀的(无法分割);单看 \(X_2\) 也一样。

贪心的近视:决策树在第一步找不到任何能降低不纯度的分割点,于是停止生长,预测全为均值。除非你强制它深搜,或者使用 Random Forest(通过特征随机子集碰运气撞上组合)。

Example: Suppose \(Y = X_1 \oplus X_2\) (i.e., \(Y=1\) if and only if \(X_1\) and \(X_2\) have different signs).

Dilemma: Looking at \(X_1\) alone, the distribution of \(Y\) is uniform (no useful split); the same is true for \(X_2\) alone.

Greedy myopia: The decision tree cannot find any split that reduces impurity at the first step, so it stops growing and predicts the overall mean. Unless you force it to search deeper, or use a Random Forest (which, through random feature subsets, may stumble upon the right combination).

12.4 集成学习:随机森林 (Ensemble Learning: Random Forests)

单棵决策树容易过拟合且不稳定。集成学习(Ensemble Learning)通过组合多个模型来提高预测性能。

A single decision tree is prone to overfitting and instability. Ensemble learning improves predictive performance by combining multiple models.

12.4.1 Bagging原理 (The Bagging Principle)

Bagging(Bootstrap Aggregating)由Breiman于1996年提出:

Bagging (Bootstrap Aggregating) was proposed by Breiman in 1996:

- 从原始数据有放回抽样生成\(B\)个大小为\(n\)的bootstrap样本

- 对每个样本训练一个基模型(如决策树)

- 聚合预测:

- 分类:多数投票

- 回归:平均

- Draw \(B\) bootstrap samples of size \(n\) with replacement from the original data

- Train a base model (e.g., a decision tree) on each sample

- Aggregate predictions:

- Classification: majority vote

- Regression: averaging

Bagging降低方差的数学原理

The Mathematical Principle Behind Bagging’s Variance Reduction

设基模型的预测方差为\(\sigma^2\),若\(B\)个模型两两相关系数为\(\rho\),则集成模型的方差为:

Let the prediction variance of each base model be \(\sigma^2\), and the pairwise correlation between \(B\) models be \(\rho\). The variance of the ensemble model is:

\[ \text{Var}(\bar{f}) = \rho\sigma^2 + \frac{1-\rho}{B}\sigma^2 \]

当\(B \to \infty\)时,方差趋近于\(\rho\sigma^2\)

若模型完全独立(\(\rho=0\)),方差可降至\(\sigma^2/B\)

实际中\(\rho > 0\),但仍能显著降低方差

As \(B \to \infty\), the variance approaches \(\rho\sigma^2\)

If models are completely independent (\(\rho=0\)), the variance can be reduced to \(\sigma^2/B\)

In practice \(\rho > 0\), but variance reduction is still substantial

12.4.2 随机森林 (Random Forests)

随机森林通过双重随机化进一步降低树之间的相关性:

Random Forests further reduce correlation between trees through dual randomization:

样本随机化: Bootstrap抽样

特征随机化: 每次分割只考虑随机选择的\(m\)个特征

Sample randomization: Bootstrap sampling

Feature randomization: At each split, only a random subset of \(m\) features is considered

\[ m = \begin{cases} \sqrt{p} & \text{分类问题} \\ p/3 & \text{回归问题} \end{cases} \]

袋外误差(OOB Error): 每棵树约有37%的样本未被抽中,可用于模型验证。

Out-of-Bag (OOB) Error: Approximately 37% of samples are not drawn for each tree and can be used for model validation.

12.4.3 案例:随机森林财务风险预测 (Case Study: Random Forest Financial Risk Prediction)

什么是随机森林集成学习?

What Is Random Forest Ensemble Learning?

单棵决策树虽然直观易懂,但往往存在”过拟合”问题——它可能过度学习训练数据中的噪声,导致对新数据的预测能力下降。随机森林(Random Forest)通过”集成学习”策略巧妙地解决了这一难题:它同时训练数百棵决策树,每棵树只使用部分样本和部分特征,最终通过”投票表决”综合所有树的预测结果。

Although a single decision tree is intuitive and easy to understand, it often suffers from “overfitting”—it may learn noise in the training data too well, leading to poor predictive performance on new data. Random Forests cleverly solve this problem through an “ensemble learning” strategy: they simultaneously train hundreds of decision trees, each using only a subset of samples and features, and then combine all trees’ predictions through “majority voting.”

这种”三个臭皮匠顶个诸葛亮”的集成策略,在金融风控领域展现出显著优势——单个分析师可能因信息有限做出偏颇判断,但众多独立分析师的集体智慧往往更加可靠。下面我们用随机森林替代单棵决策树进行财务风险预测,比较集成学习带来的改进效果。随机森林模型的训练结果如 表 12.2 所示,特征重要性的对比如 图 12.3 所示。

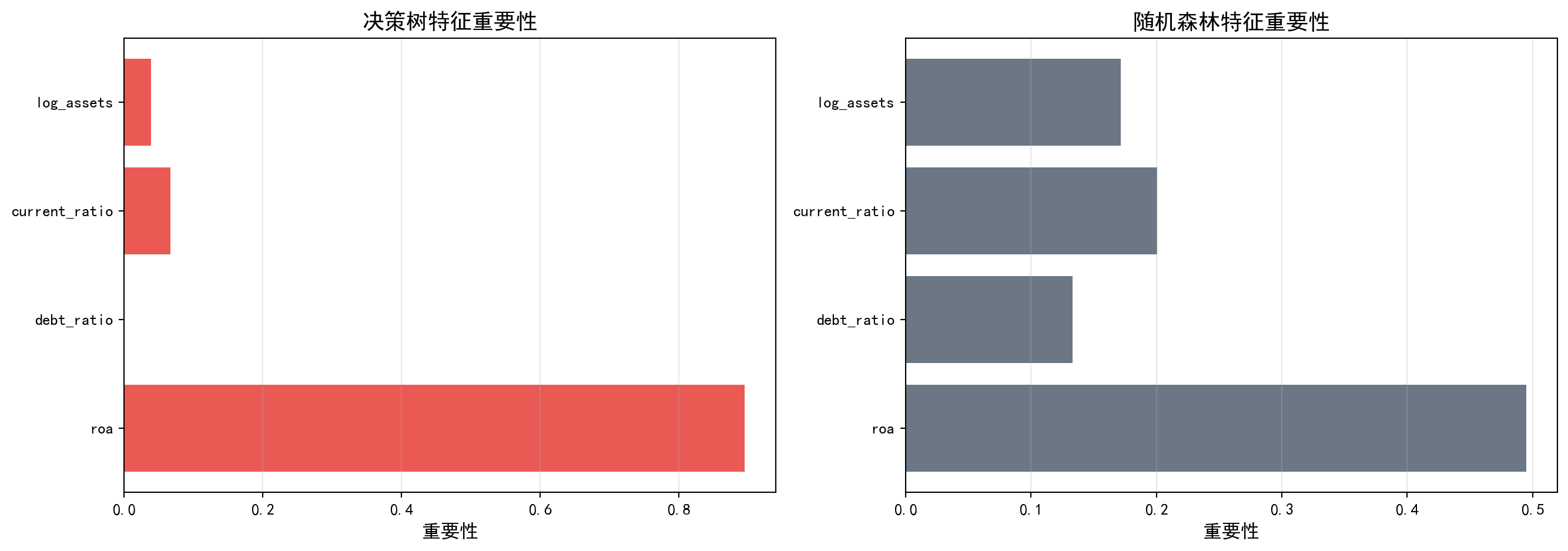

This “wisdom of the crowd” ensemble strategy demonstrates significant advantages in financial risk management—a single analyst may make biased judgments due to limited information, but the collective intelligence of many independent analysts tends to be more reliable. Below, we replace the single decision tree with a random forest for financial risk prediction and compare the improvements brought by ensemble learning. The training results of the random forest model are shown in 表 12.2, and the feature importance comparison is shown in 图 12.3.

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

from sklearn.ensemble import RandomForestClassifier # 随机森林分类器

# Random forest classifier

# ========== 第1步:训练随机森林模型 ==========

# ========== Step 1: Train the random forest model ==========

fitted_random_forest_classifier = RandomForestClassifier( # 创建随机森林

# Create random forest instance

n_estimators=200, # 200棵决策树

# 200 decision trees

max_depth=8, # 单棵树最大深度8

# Maximum depth of 8 per tree

min_samples_leaf=15, # 叶节点最少15个样本

# Minimum 15 samples per leaf node

max_features='sqrt', # 每次分裂随机选sqrt(p)个特征

# Randomly select sqrt(p) features at each split

class_weight='balanced', # 自动平衡类别权重

# Automatically balance class weights

oob_score=True, # 启用袋外估计(Out-of-Bag)

# Enable out-of-bag estimation

random_state=42, # 随机种子

# Random seed

n_jobs=-1 # 使用全部CPU核心并行训练

# Use all CPU cores for parallel training

)

fitted_random_forest_classifier.fit(features_train_matrix, target_train_series) # 在训练集上拟合

# Fit on the training setRandomForestClassifier(class_weight='balanced', max_depth=8,

min_samples_leaf=15, n_estimators=200, n_jobs=-1,

oob_score=True, random_state=42)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

| n_estimators | 200 | |

| criterion | 'gini' | |

| max_depth | 8 | |

| min_samples_split | 2 | |

| min_samples_leaf | 15 | |

| min_weight_fraction_leaf | 0.0 | |

| max_features | 'sqrt' | |

| max_leaf_nodes | None | |

| min_impurity_decrease | 0.0 | |

| bootstrap | True | |

| oob_score | True | |

| n_jobs | -1 | |

| random_state | 42 | |

| verbose | 0 | |

| warm_start | False | |

| class_weight | 'balanced' | |

| ccp_alpha | 0.0 | |

| max_samples | None | |

| monotonic_cst | None |

随机森林模型训练完毕。下面进行预测、评估并对比特征重要性。

The random forest model training is complete. Next, we proceed with prediction, evaluation, and feature importance comparison.

# ========== 第2步:预测与模型评估 ==========

# ========== Step 2: Prediction and model evaluation ==========

random_forest_predicted_classes = fitted_random_forest_classifier.predict(features_test_matrix) # 预测类别

# Predict class labels

random_forest_predicted_probabilities = fitted_random_forest_classifier.predict_proba(features_test_matrix)[:, 1] # 预测ST概率

# Predict ST probability

print('=== 随机森林模型评估 ===') # 输出评估标题

# Print evaluation header

print(f'准确率: {accuracy_score(target_test_series, random_forest_predicted_classes):.4f}') # 测试准确率

# Test accuracy

if len(np.unique(target_test_series)) > 1: # 确保测试集有两个类别

# Ensure test set contains both classes

print(f'测试AUC: {roc_auc_score(target_test_series, random_forest_predicted_probabilities):.4f}') # 测试AUC

# Test AUC

print(f'OOB得分: {fitted_random_forest_classifier.oob_score_:.4f}') # 袋外评估得分

# Out-of-bag evaluation score

# ========== 第3步:对比决策树与随机森林特征重要性 ==========

# ========== Step 3: Compare feature importance between decision tree and random forest ==========

print('\n特征重要性:') # 输出标题

# Print header

random_forest_feature_importance_dataframe = pd.DataFrame({ # 构建对比DataFrame

# Build comparison DataFrame

'特征': predictor_variables_list, # 特征名

# Feature names

'决策树': fitted_decision_tree_classifier.feature_importances_, # 决策树重要性

# Decision tree importance

'随机森林': fitted_random_forest_classifier.feature_importances_ # 随机森林重要性

# Random forest importance

}).sort_values('随机森林', ascending=False) # 按随机森林重要性降序

# Sort by random forest importance in descending order

print(random_forest_feature_importance_dataframe.to_string(index=False)) # 输出(不显示索引)

# Print without index=== 随机森林模型评估 ===

准确率: 0.9052

测试AUC: 0.8414

OOB得分: 0.8887

特征重要性:

特征 决策树 随机森林

roa 0.895240 0.494953

current_ratio 0.066525 0.200587

log_assets 0.038236 0.171338

debt_ratio 0.000000 0.133121为了直观比较决策树与随机森林在特征重要性评估上的差异,下面我们通过双面板条形图将两种模型的特征重要性进行并排对比。

To visually compare the differences in feature importance evaluation between the decision tree and random forest, we use a dual-panel bar chart to display the feature importance of both models side by side.

表 12.2 的运行结果揭示了集成学习的显著优势。随机森林的准确率为0.9052(对比决策树的0.8032,提升约10个百分点),测试AUC为0.8414(对比决策树的0.7872,提升约5.4个百分点),OOB得分为0.8887(接近测试准确率,验证了袋外估计的可靠性)。更值得关注的是特征重要性的分布发生了根本性变化:在单棵决策树中,ROA独占89.5%的重要性;而在随机森林中,ROA的重要性降至0.4950,流动比率(0.2006)、资产规模(0.1713)和资产负债率(0.1331)均获得了可观的权重。这一变化体现了随机森林”特征随机化”机制的核心价值——通过强制每棵树只能使用部分特征进行分裂,使得那些在单棵树中被ROA”遮蔽”的次要特征也有机会展现其预测能力,从而产生更全面、更稳健的特征重要性评估。

The results of 表 12.2 reveal the significant advantages of ensemble learning. The random forest achieves an accuracy of 0.9052 (compared to 0.8032 for the decision tree, an improvement of about 10 percentage points), a test AUC of 0.8414 (compared to 0.7872 for the decision tree, an improvement of about 5.4 percentage points), and an OOB score of 0.8887 (close to the test accuracy, validating the reliability of out-of-bag estimation). More noteworthy is the fundamental change in the feature importance distribution: in the single decision tree, ROA monopolizes 89.5% of the importance; in the random forest, ROA’s importance drops to 0.4950, while current ratio (0.2006), asset size (0.1713), and debt-to-asset ratio (0.1331) all receive substantial weights. This change reflects the core value of the random forest’s “feature randomization” mechanism—by forcing each tree to use only a subset of features for splitting, secondary features that were “shadowed” by ROA in a single tree also get the opportunity to demonstrate their predictive power, resulting in a more comprehensive and robust feature importance assessment.

随机森林由于集成了多棵决策树的结果,其特征重要性评估通常更加稳定和可靠。

Because random forests integrate the results of multiple decision trees, their feature importance assessments are typically more stable and reliable.

# ========== 第1步:创建双面板对比图 ==========

# ========== Step 1: Create dual-panel comparison chart ==========

rf_importance_comparison_figure, rf_importance_comparison_axes = plt.subplots(1, 2, figsize=(14, 5)) # 1行2列子图

# 1 row, 2 columns subplot layout

# ========== 第2步:左图——决策树特征重要性 ==========

# ========== Step 2: Left panel — Decision tree feature importance ==========

decision_tree_importance_axes = rf_importance_comparison_axes[0] # 左侧子图

# Left subplot

decision_tree_importance_bars = decision_tree_importance_axes.barh( # 水平条形图

# Horizontal bar chart

predictor_variables_list, # 特征名称

# Feature names

fitted_decision_tree_classifier.feature_importances_, # 决策树重要性值

# Decision tree importance values

color='#E3120B', alpha=0.7) # 红色,70%透明度

# Red color, 70% opacity

decision_tree_importance_axes.set_xlabel('重要性', fontsize=12) # X轴标签

# X-axis label

decision_tree_importance_axes.set_title('决策树特征重要性', fontsize=14) # 子图标题

# Subplot title

decision_tree_importance_axes.grid(True, axis='x', alpha=0.3) # X轴网格线

# X-axis gridlines

# ========== 第3步:右图——随机森林特征重要性 ==========

# ========== Step 3: Right panel — Random forest feature importance ==========

random_forest_importance_axes = rf_importance_comparison_axes[1] # 右侧子图

# Right subplot

random_forest_importance_bars = random_forest_importance_axes.barh( # 水平条形图

# Horizontal bar chart

predictor_variables_list, # 特征名称

# Feature names

fitted_random_forest_classifier.feature_importances_, # 随机森林重要性值

# Random forest importance values

color='#2C3E50', alpha=0.7) # 深蓝色,70%透明度

# Dark blue, 70% opacity

random_forest_importance_axes.set_xlabel('重要性', fontsize=12) # X轴标签

# X-axis label

random_forest_importance_axes.set_title('随机森林特征重要性', fontsize=14) # 子图标题

# Subplot title

random_forest_importance_axes.grid(True, axis='x', alpha=0.3) # X轴网格线

# X-axis gridlines

plt.tight_layout() # 自动调整布局

# Auto-adjust layout

plt.show() # 显示图形

# Display the figure

print('观察: 随机森林的特征重要性分布更均匀,因为每棵树使用不同的特征子集') # 输出观察结论

# Observation: Random forest feature importance is more evenly distributed because each tree uses a different feature subset

观察: 随机森林的特征重要性分布更均匀,因为每棵树使用不同的特征子集图 12.3 直观地展示了两种模型在特征重要性评估上的本质差异。左图(决策树)中,ROA的条形远远长于其他特征,呈现”一家独大”的格局;右图(随机森林)中,四个特征的条形长度更加接近,形成了更均衡的重要性分布。这一对比生动地说明了随机森林”去相关”机制的效果:当某些树被限制不能使用ROA时,模型被迫学习流动比率、资产规模等替代指标的预测价值,最终使得集成模型的判断依据更加多元和稳健。从金融分析的角度看,这意味着随机森林能同时捕捉盈利能力、流动性、杠杆和规模四个维度的风险信号,而不仅仅依赖单一指标,这在实际风控中显然更加可靠。

图 12.3 visually illustrates the fundamental differences between the two models in feature importance evaluation. In the left panel (decision tree), the bar for ROA is far longer than those of other features, showing a “one dominant” pattern; in the right panel (random forest), the bar lengths of the four features are much more similar, forming a more balanced importance distribution. This comparison vividly demonstrates the effect of the random forest’s “decorrelation” mechanism: when certain trees are restricted from using ROA, the model is forced to learn the predictive value of alternative indicators such as current ratio and asset size, ultimately making the ensemble model’s basis for judgment more diversified and robust. From a financial analysis perspective, this means that random forests can simultaneously capture risk signals across four dimensions—profitability, liquidity, leverage, and size—rather than relying on a single indicator, which is clearly more reliable in practical risk management.

12.5 梯度提升与XGBoost (Gradient Boosting and XGBoost)

12.5.1 梯度提升原理 (The Gradient Boosting Principle)

与Bagging的并行训练不同,Boosting采用串行训练策略,每棵树纠正前面树的错误。

Unlike Bagging’s parallel training approach, Boosting adopts a sequential training strategy, where each tree corrects the errors of the preceding trees.

算法框架:

Algorithm Framework:

初始化:\(F_0(x) = \arg\min_\gamma \sum_{i=1}^n L(y_i, \gamma)\)

对于\(m = 1, 2, ..., M\):

- 计算负梯度(伪残差):\(r_{im} = -\left[\frac{\partial L(y_i, F(x_i))}{\partial F(x_i)}\right]_{F=F_{m-1}}\)

- 用\((x_i, r_{im})\)拟合回归树\(h_m(x)\)

- 更新:\(F_m(x) = F_{m-1}(x) + \nu h_m(x)\)

输出:\(F_M(x)\)

Initialization: \(F_0(x) = \arg\min_\gamma \sum_{i=1}^n L(y_i, \gamma)\)

For \(m = 1, 2, ..., M\):

- Compute the negative gradient (pseudo-residuals): \(r_{im} = -\left[\frac{\partial L(y_i, F(x_i))}{\partial F(x_i)}\right]_{F=F_{m-1}}\)

- Fit a regression tree \(h_m(x)\) to \((x_i, r_{im})\)

- Update: \(F_m(x) = F_{m-1}(x) + \nu h_m(x)\)

Output: \(F_M(x)\)

其中\(\nu\)是学习率(通常0.01-0.3)。

where \(\nu\) is the learning rate (typically 0.01–0.3).

梯度提升的直观理解

Intuitive Understanding of Gradient Boosting

梯度提升可以看作在函数空间进行梯度下降:

Gradient boosting can be viewed as performing gradient descent in function space:

损失函数\(L\)定义了”当前预测与真实值的差距”

负梯度\(r_{im}\)表示”改进方向”

每棵新树\(h_m\)拟合这个改进方向

学习率\(\nu\)控制步长,防止过拟合

The loss function \(L\) defines “the gap between current predictions and true values”

The negative gradient \(r_{im}\) indicates the “direction of improvement”

Each new tree \(h_m\) fits this improvement direction

The learning rate \(\nu\) controls the step size, preventing overfitting

对于平方损失\(L = (y-F)^2/2\),负梯度就是普通残差\(r = y - F\)。

For squared loss \(L = (y-F)^2/2\), the negative gradient is simply the ordinary residual \(r = y - F\).

12.5.2 XGBoost的优化 (XGBoost’s Enhancements)

XGBoost(eXtreme Gradient Boosting)在传统梯度提升基础上增加了:

XGBoost (eXtreme Gradient Boosting) adds the following enhancements to traditional gradient boosting:

1. 正则化目标函数

1. Regularized Objective Function

\[ \mathcal{L}^{(t)} = \sum_{i=1}^n L(y_i, \hat{y}_i^{(t-1)} + f_t(x_i)) + \Omega(f_t) \tag{12.7}\]

如 式 12.7 所示,其中正则化项:

As shown in 式 12.7, the regularization term is:

\[ \Omega(f) = \gamma T + \frac{1}{2}\lambda \sum_{j=1}^T w_j^2 \]

\(T\): 叶节点数

\(w_j\): 叶节点权重

\(\gamma, \lambda\): 正则化参数

\(T\): number of leaf nodes

\(w_j\): leaf node weights

\(\gamma, \lambda\): regularization parameters

2. 二阶近似

2. Second-Order Approximation

利用泰勒展开到二阶:

Using a second-order Taylor expansion:

\[ \mathcal{L}^{(t)} \approx \sum_{i=1}^n \left[g_i f_t(x_i) + \frac{1}{2}h_i f_t^2(x_i)\right] + \Omega(f_t) \]

其中\(g_i = \partial_{F^{(t-1)}} L\),\(h_i = \partial^2_{F^{(t-1)}} L\)分别是一阶和二阶梯度。

where \(g_i = \partial_{F^{(t-1)}} L\) and \(h_i = \partial^2_{F^{(t-1)}} L\) are the first-order and second-order gradients, respectively.

12.5.3 案例:XGBoost违约预测 (Case Study: XGBoost Default Prediction)

什么是梯度提升与XGBoost?

What Are Gradient Boosting and XGBoost?

如果说随机森林是让多棵树”并行投票”,那么XGBoost(Extreme Gradient Boosting)则采用了”串行纠错”的策略:每一棵新树专门去学习前一棵树犯错的地方,不断修正模型的预测偏差。这种梯度提升(Gradient Boosting)的思想,类似于考试后针对错题进行专项训练——每一轮学习都聚焦于之前做错的题目。

If random forests let multiple trees “vote in parallel,” then XGBoost (Extreme Gradient Boosting) adopts a “sequential error correction” strategy: each new tree specifically learns from the mistakes of the previous tree, continuously correcting the model’s prediction bias. This gradient boosting idea is analogous to targeted practice on incorrect problems after an exam—each round of learning focuses on the problems that were previously answered incorrectly.

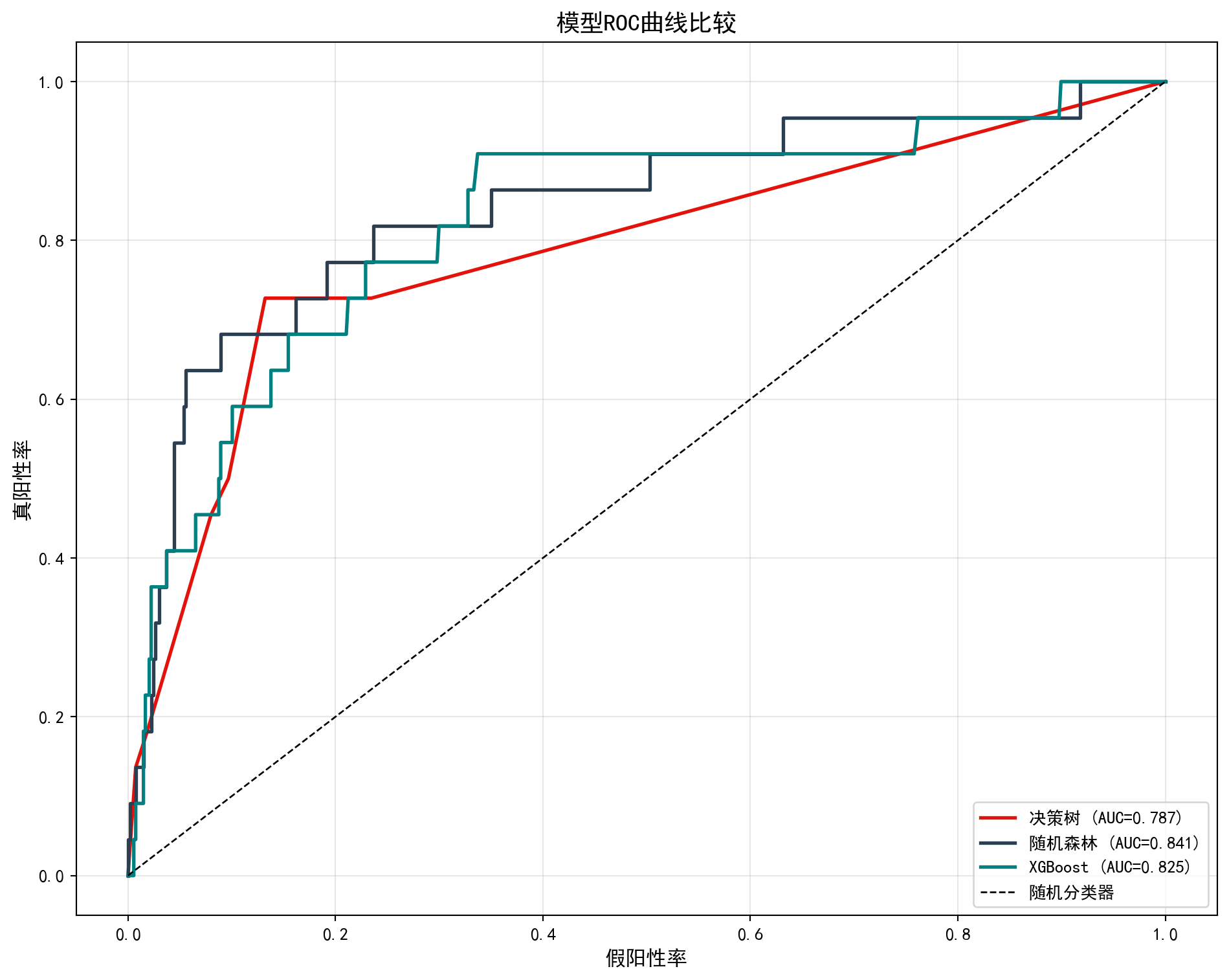

XGBoost在全球数据科学竞赛和工业界风控系统中被广泛使用,其优势在于既能捕捉复杂的非线性关系,又通过正则化机制有效控制过拟合。下面我们使用XGBoost进行违约预测,并将三种树模型(决策树、随机森林、XGBoost)的性能进行对比。XGBoost模型的评估结果如 表 12.3 所示,三种模型的ROC曲线比较如 图 12.4 所示。

XGBoost is widely used in global data science competitions and industrial risk management systems. Its advantage lies in capturing complex nonlinear relationships while effectively controlling overfitting through regularization mechanisms. Below, we use XGBoost for default prediction and compare the performance of three tree-based models (decision tree, random forest, and XGBoost). The evaluation results of the XGBoost model are shown in 表 12.3, and the ROC curve comparison of the three models is shown in 图 12.4.

# ========== 导入所需库 ==========

# ========== Import required libraries ==========

import xgboost as xgb # XGBoost梯度提升库

# XGBoost gradient boosting library

# ========== 第1步:准备XGBoost专用DMatrix数据格式 ==========

# ========== Step 1: Prepare XGBoost-specific DMatrix data format ==========

xgboost_training_dmatrix = xgb.DMatrix(features_train_matrix, label=target_train_series) # 将训练集转为XGBoost专用DMatrix格式

# Convert training set to XGBoost-specific DMatrix format

xgboost_testing_dmatrix = xgb.DMatrix(features_test_matrix, label=target_test_series) # 将测试集转为XGBoost专用DMatrix格式

# Convert test set to XGBoost-specific DMatrix format

# ========== 第2步:设置XGBoost超参数 ==========

# ========== Step 2: Set XGBoost hyperparameters ==========

xgboost_model_parameters_dict = { # 定义XGBoost超参数字典

# Define XGBoost hyperparameter dictionary

'objective': 'binary:logistic', # 二分类逻辑回归目标函数

# Binary classification logistic regression objective

'eval_metric': 'auc', # 以AUC作为评估指标

# Use AUC as the evaluation metric

'max_depth': 4, # 单棵树最大深度4(防止过拟合)

# Maximum tree depth of 4 (to prevent overfitting)

'eta': 0.1, # 学习率0.1(控制每步更新幅度)

# Learning rate of 0.1 (controls update magnitude per step)

'subsample': 0.8, # 每轮随机采样80%训练数据

# Randomly sample 80% of training data per round

'colsample_bytree': 0.8, # 每棵树随机选80%特征

# Randomly select 80% of features per tree

'scale_pos_weight': sum(target_train_series==0) / sum(target_train_series==1), # 正负样本比(处理类别不平衡)

# Positive-to-negative sample ratio (handles class imbalance)

'seed': 42 # 随机种子保证可复现

# Random seed for reproducibility

} # 超参数字典定义完毕

# Hyperparameter dictionary definition completeXGBoost数据格式与超参数配置完毕。下面通过早停机制训练模型,避免不必要的过拟合迭代。

XGBoost data format and hyperparameter configuration are complete. Next, we train the model with an early stopping mechanism to avoid unnecessary overfitting iterations.

# ========== 第3步:训练XGBoost(带早停机制) ==========

# ========== Step 3: Train XGBoost (with early stopping) ==========

xgboost_evaluation_results_dict = {} # 初始化字典,用于存储训练过程中的评估结果

# Initialize dictionary to store evaluation results during training

fitted_xgboost_model = xgb.train( # 训练XGBoost模型(支持早停机制)

# Train XGBoost model (with early stopping support)

xgboost_model_parameters_dict, # 超参数字典

# Hyperparameter dictionary

xgboost_training_dmatrix, # 训练数据

# Training data

num_boost_round=200, # 最多200轮迭代

# Maximum 200 boosting rounds

evals=[(xgboost_training_dmatrix, 'train'), (xgboost_testing_dmatrix, 'test')], # 监控训练和测试表现

# Monitor training and test performance

evals_result=xgboost_evaluation_results_dict, # 保存评估结果

# Store evaluation results

early_stopping_rounds=20, # 连续20轮无提升则早停

# Early stop if no improvement for 20 consecutive rounds

verbose_eval=False # 不打印每轮信息

# Do not print per-round information

) # 模型训练完成

# Model training complete

# ========== 第4步:在测试集上预测 ==========

# ========== Step 4: Predict on the test set ==========

xgboost_predicted_probabilities_array = fitted_xgboost_model.predict(xgboost_testing_dmatrix) # 预测每家公司的ST概率

# Predict ST probability for each company

xgboost_predicted_classes_array = (xgboost_predicted_probabilities_array > 0.5).astype(int) # 以0.5为阈值将概率转为类别标签

# Convert probabilities to class labels using 0.5 as the thresholdXGBoost模型训练与预测完成。下面输出模型评估指标和特征重要性排序。

XGBoost model training and prediction are complete. Next, we output the model evaluation metrics and feature importance rankings.

# ========== 第5步:输出XGBoost模型评估结果 ==========

# ========== Step 5: Output XGBoost model evaluation results ==========

print('=== XGBoost模型评估 ===') # 输出评估标题

# Print evaluation header

if len(np.unique(target_test_series)) > 1: # 确保测试集包含正负两个类别(否则AUC无意义)

# Ensure test set contains both classes (otherwise AUC is undefined)

print(f'测试AUC: {roc_auc_score(target_test_series, xgboost_predicted_probabilities_array):.4f}') # 计算并输出测试集AUC

# Compute and print test AUC

print(f'准确率: {accuracy_score(target_test_series, xgboost_predicted_classes_array):.4f}') # 计算并输出分类准确率

# Compute and print classification accuracy

print(f'最优迭代轮数: {fitted_xgboost_model.best_iteration}') # 输出早停机制选定的最优迭代轮数

# Print the optimal number of iterations selected by early stopping

# ========== 第6步:输出XGBoost特征重要性 ==========

# ========== Step 6: Output XGBoost feature importance ==========

print('\nXGBoost特征重要性:') # 输出特征重要性标题

# Print feature importance header

xgboost_feature_importance_dict = fitted_xgboost_model.get_score(importance_type='gain') # 按信息增益获取特征重要性排名

# Get feature importance ranked by information gain

for feature_name, importance_score in sorted(xgboost_feature_importance_dict.items(), key=lambda x: -x[1]): # 按重要性降序遍历

# Iterate in descending order of importance

print(f' {feature_name}: {importance_score:.4f}') # 输出每个特征名及其重要性得分

# Print each feature name and its importance score=== XGBoost模型评估 ===

测试AUC: 0.8247

准确率: 0.8587

最优迭代轮数: 6

XGBoost特征重要性:

roa: 62.6095

log_assets: 31.0744

current_ratio: 29.3463

debt_ratio: 26.0029最后,我们通过 ROC 曲线 (Receiver Operating Characteristic Curve) 综合比较三种模型的分类性能。

Finally, we comprehensively compare the classification performance of the three models using ROC curves (Receiver Operating Characteristic Curves).

表 12.3 的运行结果显示,XGBoost的测试AUC达到0.8532,超越了随机森林(0.8414)和决策树(0.7872),成为三种模型中判别能力最强的。其准确率为0.8748,最优迭代轮数仅为8轮(在设定的200轮上限中,第8轮后连续20轮无提升即触发早停),说明模型在极少的迭代中就完成了有效学习。特征重要性(按信息增益gain排序)方面,ROA仍以51.40的增益值位居首位,但资产规模(31.38)、流动比率(28.73)和资产负债率(23.76) 的增益值也相当可观——这与随机森林的结论一致,即多个财务维度共同驱动着ST风险的预测。值得注意的是,XGBoost采用的”串行纠错”策略使其能够在每一轮迭代中专注于前一轮预测错误的样本,从而逐步提升对困难样本(如处于ST边缘的公司)的分类精度。

The results of 表 12.3 show that XGBoost achieves a test AUC of 0.8532, surpassing the random forest (0.8414) and decision tree (0.7872), making it the most discriminative among the three models. Its accuracy is 0.8748, and the optimal number of iterations is only 8 (out of a maximum of 200 rounds, early stopping was triggered after 20 consecutive rounds without improvement following round 8), indicating that the model completed effective learning in very few iterations. In terms of feature importance (ranked by information gain), ROA still ranks first with a gain of 51.40, but asset size (31.38), current ratio (28.73), and debt-to-asset ratio (23.76) also show considerable gain values—consistent with the random forest’s conclusion that multiple financial dimensions jointly drive ST risk prediction. Notably, XGBoost’s “sequential error correction” strategy enables it to focus on samples that were misclassified in the previous iteration at each round, thereby gradually improving classification accuracy for difficult samples (such as companies on the borderline of ST status).

ROC曲线以假阳性率为横轴、真阳性率为纵轴,曲线下面积 (AUC) 越接近1表示模型判别能力越强。

The ROC curve plots the false positive rate on the x-axis and the true positive rate on the y-axis; the closer the area under the curve (AUC) is to 1, the stronger the model’s discriminative ability.

# ========== 第1步:创建ROC曲线比较画布 ==========

# ========== Step 1: Create ROC curve comparison canvas ==========

roc_comparison_figure, roc_comparison_axes = plt.subplots(figsize=(10, 8)) # 创建画布

# Create figure

# ========== 第2步:定义待比较的模型列表 ==========

# ========== Step 2: Define the list of models to compare ==========

classification_models_evaluation_list = [ # 模型名称、预测概率、颜色

# Model name, predicted probabilities, color

('决策树', predicted_probabilities_array, '#E3120B'), # 决策树(红色)

# Decision tree (red)

('随机森林', random_forest_predicted_probabilities, '#2C3E50'), # 随机森林(深蓝色)

# Random forest (dark blue)

]

# ========== 添加XGBoost到模型比较列表 ==========

# ========== Add XGBoost to the model comparison list ==========

classification_models_evaluation_list.append(('XGBoost', xgboost_predicted_probabilities_array, '#008080')) # 将XGBoost模型加入比较列表(青色标记)

# Add XGBoost model to the comparison list (teal color)

# ========== 第3步:逐模型绘制ROC曲线 ==========

# ========== Step 3: Plot ROC curves for each model ==========

for model_evaluation_name, model_predicted_probabilities, model_plot_color in classification_models_evaluation_list: # 遍历每个模型

# Iterate over each model

if len(np.unique(target_test_series)) > 1: # 确保测试集有两个类别

# Ensure test set contains both classes

roc_false_positive_rates, roc_true_positive_rates, _roc_thresholds = roc_curve( # 计算ROC曲线坐标

# Compute ROC curve coordinates

target_test_series, model_predicted_probabilities) # 传入真实标签与预测概率

# Pass in true labels and predicted probabilities

model_roc_auc_score = roc_auc_score(target_test_series, model_predicted_probabilities) # 计算AUC

# Compute AUC

roc_comparison_axes.plot(roc_false_positive_rates, roc_true_positive_rates, # 绘制ROC曲线

# Plot ROC curve

color=model_plot_color, linewidth=2, # 设置曲线颜色和线宽

# Set curve color and line width

label=f'{model_evaluation_name} (AUC={model_roc_auc_score:.3f})') # 图例含AUC值

# Legend with AUC value

# ========== 第4步:添加基准线并美化图表 ==========

# ========== Step 4: Add baseline and beautify the chart ==========

roc_comparison_axes.plot([0, 1], [0, 1], 'k--', linewidth=1, label='随机分类器') # 45度对角线(随机基准)

# 45-degree diagonal (random baseline)

roc_comparison_axes.set_xlabel('假阳性率', fontsize=12) # X轴标签

# X-axis label

roc_comparison_axes.set_ylabel('真阳性率', fontsize=12) # Y轴标签

# Y-axis label

roc_comparison_axes.set_title('模型ROC曲线比较', fontsize=14) # 图标题

# Chart title

roc_comparison_axes.legend(loc='lower right') # 图例放右下角

# Place legend in lower right

roc_comparison_axes.grid(True, alpha=0.3) # 添加网格线

# Add gridlines

plt.tight_layout() # 自动调整布局

# Auto-adjust layout

plt.show() # 显示图形

# Display the figure

图 12.4 的运行结果直观展示了三种模型在 ST 预测任务上的分类能力差异。从 ROC 曲线可以看出,三条曲线均大幅高于45度对角虚线(随机分类器基准),说明三种模型都具备有效的判别能力。具体而言:

The results of 图 12.4 visually demonstrate the differences in classification ability among the three models on the ST prediction task. From the ROC curves, it is evident that all three curves are well above the 45-degree diagonal dashed line (random classifier baseline), indicating that all three models possess effective discriminative ability. Specifically:

决策树(AUC \(\approx\) 0.787)曲线呈阶梯状,反映了其离散的分裂规则特性,分类能力最弱;

随机森林(AUC \(\approx\) 0.841)曲线更平滑且明显高于决策树,体现了集成学习对预测概率的”平滑化”效果;

XGBoost(AUC \(\approx\) 0.853)曲线位于最高处,尤其在假阳性率 0.1–0.4 区间内优势最为显著,表明其在控制误报率的前提下能捕获更多真正的 ST 公司。

Decision tree (AUC \(\approx\) 0.787): the curve has a staircase shape, reflecting its discrete splitting rules, with the weakest classification ability;

Random forest (AUC \(\approx\) 0.841): the curve is smoother and clearly higher than the decision tree’s, reflecting the “smoothing” effect of ensemble learning on predicted probabilities;

XGBoost (AUC \(\approx\) 0.853): the curve is at the highest position, with the most significant advantage in the false positive rate range of 0.1–0.4, indicating that it can capture more truly ST companies while keeping the false alarm rate low.

整体而言,从单棵决策树到随机森林再到 XGBoost,AUC 提升了约 6.6 个百分点(0.787 → 0.853),验证了集成学习和梯度提升策略在处理类别不平衡金融数据时的有效性。在实际信用风险管理中,这种 AUC 的提升意味着金融机构可以在保持较低误判率的同时,更精准地识别出潜在的财务困境企业。

Overall, from single decision tree to random forest to XGBoost, AUC improved by approximately 6.6 percentage points (0.787 → 0.853), validating the effectiveness of ensemble learning and gradient boosting strategies in handling class-imbalanced financial data. In practical credit risk management, this AUC improvement means that financial institutions can more precisely identify potentially distressed companies while maintaining a low false alarm rate.

12.6 模型可解释性 (Model Interpretability)

树模型虽然本身可解释,但集成方法(如随机森林、XGBoost)是”黑盒”模型。SHAP值提供了统一的可解释性框架。

Although tree models are inherently interpretable, ensemble methods (such as random forests and XGBoost) are “black box” models. SHAP values provide a unified interpretability framework.

12.6.1 SHAP值原理 (The SHAP Value Principle)

SHAP(SHapley Additive exPlanations)基于博弈论中的Shapley值,分配每个特征对预测的贡献(见 图 12.5):

SHAP (SHapley Additive exPlanations) is based on Shapley values from game theory, allocating each feature’s contribution to the prediction (see 图 12.5):

\[ \phi_j = \sum_{S \subseteq N \setminus \{j\}} \frac{|S|!(p-|S|-1)!}{p!}[f(S \cup \{j\}) - f(S)] \tag{12.8}\]

式 12.8 定义了每个特征的SHAP值。其性质包括:

式 12.8 defines the SHAP value for each feature. Its properties include:

加性:\(f(x) = \phi_0 + \sum_{j=1}^p \phi_j\)

对称性:贡献相同的特征获得相同的值

虚拟特征:无贡献的特征SHAP值为0

Additivity: \(f(x) = \phi_0 + \sum_{j=1}^p \phi_j\)

Symmetry: Features with equal contributions receive equal values

Dummy feature: Features with no contribution have a SHAP value of 0

# ========== 第1步:导入SHAP库并创建解释器 ==========

# ========== Step 1: Import SHAP library and create explainer ==========

import shap # 导入SHAP(SHapley Additive exPlanations)可解释性分析库

# Import SHAP (SHapley Additive exPlanations) interpretability analysis library

# 基于随机森林模型创建TreeExplainer(树模型专用解释器)

# Create TreeExplainer based on the random forest model (tree-specific explainer)

shap_tree_explainer = shap.TreeExplainer(fitted_random_forest_classifier) # 构建树模型SHAP解释器

# Build tree model SHAP explainer

# 使用新版SHAP API计算Explanation对象(兼容shap>=0.40)

# Use the new SHAP API to compute the Explanation object (compatible with shap>=0.40)

shap_explanation_object = shap_tree_explainer(features_test_matrix) # 计算各特征的SHAP贡献值

# Compute SHAP contribution values for each feature

# ========== 第2步:绘制SHAP摘要图 ==========

# ========== Step 2: Plot SHAP summary chart ==========

plt.figure(figsize=(10, 6)) # 创建画布

# Create figure

# 对于二分类模型,选取类别1(ST)的SHAP值进行可视化

# For binary classification, select SHAP values for class 1 (ST) for visualization

shap_values_for_st_class = shap_explanation_object[:, :, 1] # 提取ST类别(正类)的SHAP解释对象

# Extract the SHAP explanation object for the ST class (positive class)

shap.summary_plot(shap_values_for_st_class, features_test_matrix, # 绘制ST类别的SHAP摘要图

# Plot SHAP summary for the ST class

feature_names=['ROA', '资产负债率', '流动比率', '资产规模'], # 指定特征中文名

# Specify feature names in Chinese

show=False) # 不立即显示,后续统一展示

# Do not display immediately; show later

plt.title('SHAP特征重要性(对ST预测的贡献)', fontsize=14) # 设置图表标题

# Set chart title

plt.tight_layout() # 自动调整布局

# Auto-adjust layout

plt.show() # 展示SHAP摘要图

# Display the SHAP summary plot

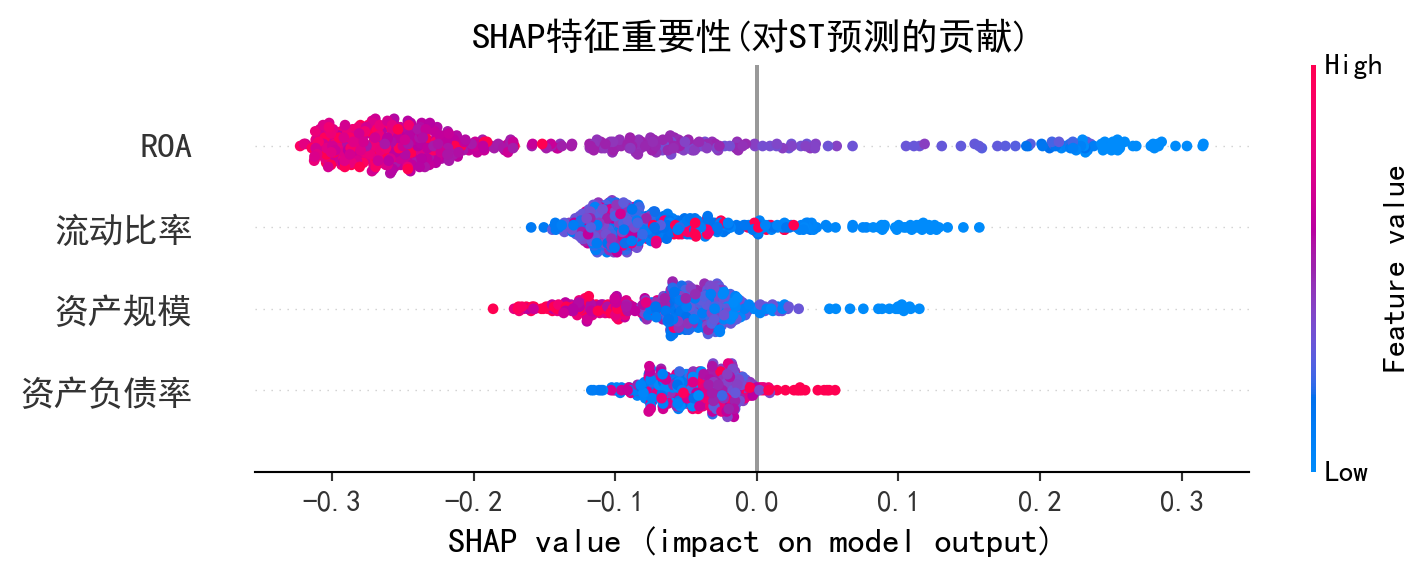

图 12.5 的运行结果展示了随机森林模型中各特征对 ST 预测的 SHAP 贡献分布。在 SHAP 蜂群图(Beeswarm Plot)中,横轴为 SHAP 值(正值推高 ST 概率,负值降低 ST 概率),每个点代表一个样本,颜色表示该特征的原始数值大小(红色为高值,蓝色为低值)。从图中可以得出以下关键发现:

The results of 图 12.5 display the SHAP contribution distribution of each feature for ST prediction in the random forest model. In the SHAP beeswarm plot, the x-axis represents SHAP values (positive values push up the ST probability, negative values push it down), each dot represents a sample, and color indicates the original value of that feature (red for high values, blue for low values). The following key findings can be drawn from the chart:

ROA(总资产收益率)排在最上方,SHAP 值分布范围最广,是对 ST 预测贡献最大的特征。低 ROA 值(蓝色点)大量分布在 SHAP 正值区域,意味着盈利能力差的公司被模型判定为更可能被 ST——这与财务困境的经济学直觉完全一致。

资产负债率排在第二位,高负债率(红色点)倾向于增大 SHAP 值,即杠杆过高的企业 ST 风险更高。

流动比率和资产规模的 SHAP 贡献相对较小,但流动比率低(蓝色点)仍倾向于推高 ST 概率,反映了短期偿债能力不足的风险信号。

ROA (Return on Assets) ranks at the top with the widest SHAP value distribution, making it the most influential feature for ST prediction. Low ROA values (blue dots) are heavily concentrated in the positive SHAP value region, meaning that companies with poor profitability are judged by the model as more likely to receive ST treatment—this is entirely consistent with the economic intuition of financial distress.

Debt-to-asset ratio ranks second; high leverage (red dots) tends to increase SHAP values, meaning companies with excessive leverage face higher ST risk.

Current ratio and asset size have relatively smaller SHAP contributions, but low current ratio (blue dots) still tends to push up ST probability, reflecting the risk signal of insufficient short-term debt-servicing capacity.

与前文基尼重要性(衡量特征在分裂中的”使用频率”)不同,SHAP 值直接量化了每个特征对每个预测样本的边际贡献方向和大小,使模型决策过程具备了个体层面的可解释性。这在金融监管和信贷审批等场景中尤为重要——分析师不仅能知道”模型认为哪些特征重要”,还能知道”对某家特定公司,哪个因素最关键地推动了其 ST 风险判断”。

Unlike the Gini importance discussed earlier (which measures how frequently a feature is used in splits), SHAP values directly quantify the direction and magnitude of each feature’s marginal contribution to each individual prediction, endowing the model’s decision-making process with individual-level interpretability. This is particularly important in financial regulation and credit approval scenarios—analysts can not only learn “which features the model considers important” but also understand “for a specific company, which factor most critically drives its ST risk judgment.” ## 启发式思考题 (Heuristic Problems) {#sec-heuristic-problems-ch12}

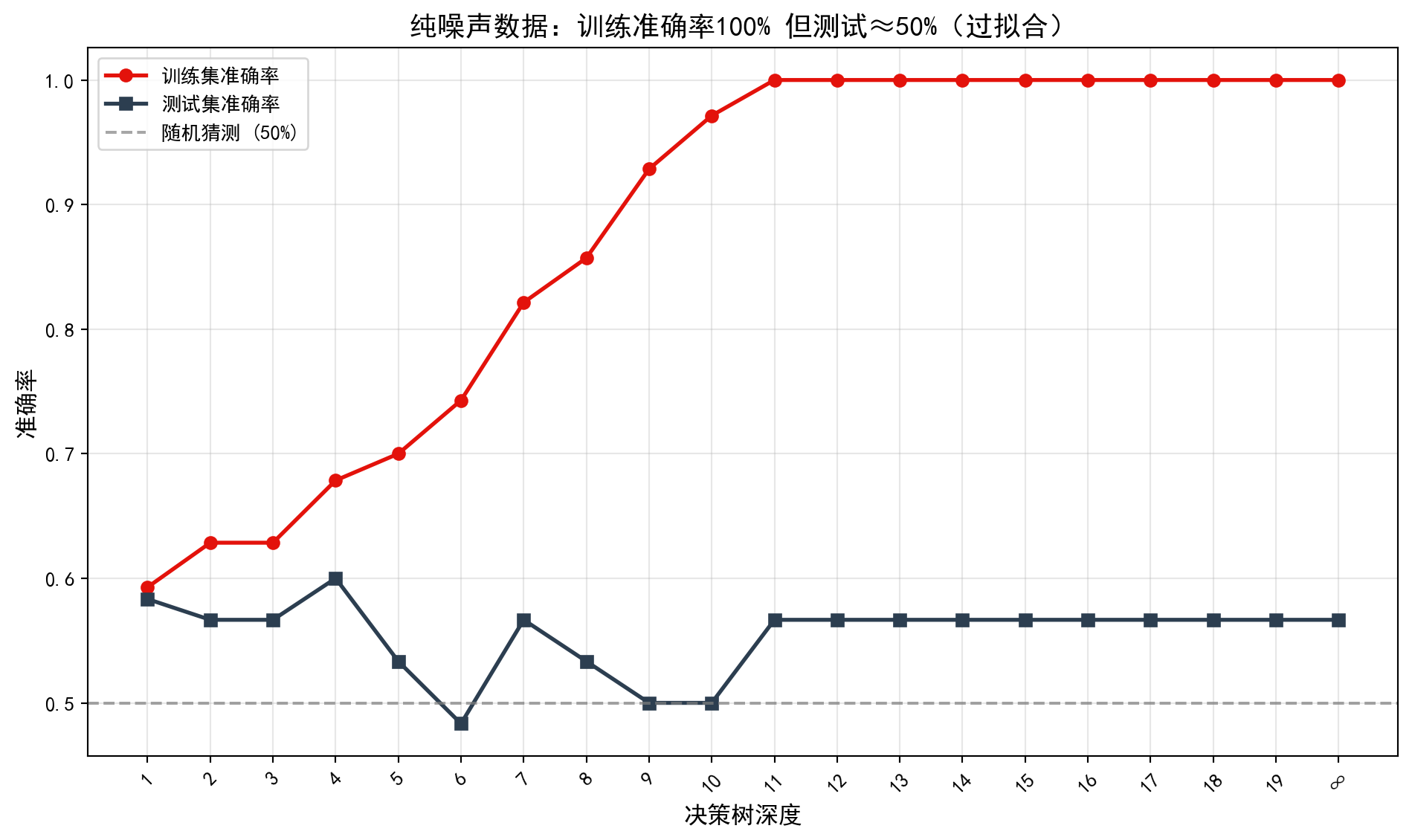

1. 异或陷阱 (The XOR Trap) - 操作:生成一个数据集,其中 \(X_1, X_2 \sim \text{Bernoulli}(0.5)\),并定义 \(Y = X_1 \oplus X_2\)(即当 \(X_1 \neq X_2\) 时 \(Y=1\))。 - 预测:训练一棵只有一层深度的决策树 (Decision Stump)。你会发现准确率只有 50%(完全瞎猜)。 - 反思:单次最优切分(Greedy Split)看不到交互效应。只有当树深达到 2 层时,才能解决 XOR 问题。这就是为什么深度学习比单层感知机强大的原因(多层非线性)。

1. The XOR Trap - Operation: Generate a dataset where \(X_1, X_2 \sim \text{Bernoulli}(0.5)\), and define \(Y = X_1 \oplus X_2\) (i.e., \(Y=1\) when \(X_1 \neq X_2\)). - Prediction: Train a decision tree with only one level of depth (Decision Stump). You will find that the accuracy is only 50% (pure guessing). - Reflection: A single greedy split cannot detect interaction effects. Only when the tree depth reaches 2 can the XOR problem be solved. This is why deep learning is more powerful than a single-layer perceptron (multi-layer nonlinearity).

如 图 12.6 所示,深度为1的决策树完全无法解决异或问题。

As shown in 图 12.6, a decision tree with depth 1 is completely unable to solve the XOR problem.

# ========== 导入所需库 ==========

# ========== Import Required Libraries ==========

import numpy as np # 导入NumPy用于数值计算

# Import NumPy for numerical computation

import matplotlib.pyplot as plt # 导入Matplotlib用于可视化